Successful investing in Emerging Markets is inextricably linked to a deep understanding of Environmental, Social and Governance (ESG) factors.

Developing countries are likely to face a disproportionate impact from some of the sustainability challenges facing the world today, in particular the risks associated with climate change. Yet, this is also where the most compelling investment opportunities associated with the attainment of the Paris Agreement targets and the United Nations Sustainability Development Goals (SDGs) will take place, which, over time, can be a valuable source of alpha.

However, investors beware. The successful integration of ESG considerations in Emerging Markets equity investing is complex and prone to challenges, which are not always advertised. This paper exposes some of the practical challenges needing to be overcome and outlines how they have been addressed by Ashmore.

The compelling investment opportunity

Let us first consider the investment opportunity. Emerging Markets dominate the supply chains of several industries at the forefront of sustainable economic development. This is particularly the case for renewable energy and electric vehicles (EV). Ashmore assesses the opportunity and risk of a transition to a low-carbon economy through the TCFD framework, as well as appraises the significant tailwinds in industries such as those that promote financial inclusion, education provision and healthcare, amongst others.

CASE STUDY

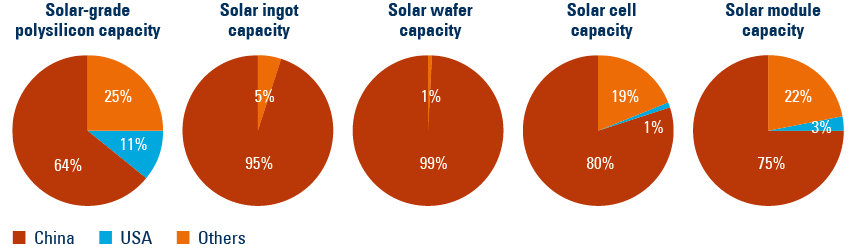

China’s dominance in solar manufacturing

China is the leading producer of the raw material used in solar cells, polysilicon. China dominates solar ingot manufacturing (the materials that can be cast into standardised shapes to be further processed), as well as wafer manufacturing. China also dominates the manufacturing of solar cells and the final solar module (the component seen on solar panels).

Figure 1: China’s dominance of the solar manufacturing value chain

Source: Mood Makenzie based on Wind turbine, Solar module & Battery storage 2022

The investment opportunity is significant. The OECD estimates that to meet net-zero emissions targets by 2050, annual clean energy investment must increase seven fold, from USD 150 billion in 2020 to over USD 1 trillion by 2030. The International Energy Agency believes a total transformation of the energy systems that underpin our economies is required to meet Net Zero Emissions by 2050.1 This is expected via investment in renewable energy, the digitalisation of grids and the electrification of end uses (such as transport, buildings and industry).

Consequently, investors need to consider Emerging Markets as an unavoidable, indeed disproportionately important, part of the sustainable economic development solution. However, successful investing in Emerging Markets equity requires navigating several challenges associated with ESG implementation, which Ashmore as a specialist Emerging Marketing investor is well positioned to do.

Challenges of ESG integration in Emerging Markets equities

CHALLENGE 1

What is a consistent methodology to apply when integrating ESG?

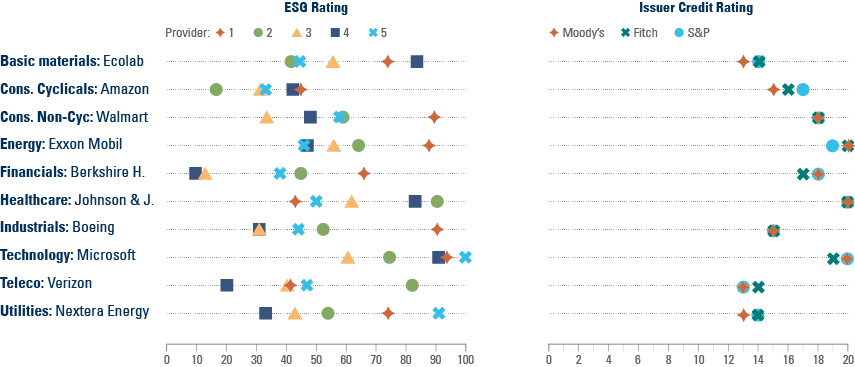

The ESG industry continues to evolve and formalise, which means reliance on third-party tools to implement an ESG approach risks inconsistency. This is reflected by the high divergence in ESG scores from different rating agencies given their differing methodologies. This is only more apparent when compared to the consistency of their credit scores. The contrast is highlighted in the following table for US stocks, and is only exacerbated in EM, the reasons for which have been well documented by the MIT2, amongst others.

Figure 2: US Stocks: ESG Rating vs. Credit Rating

Investors have a range of views on the importance of company financial fundamentals and the same is only truer for non-financial factors. ESG factors are notably hard to quantify given: the subjectivity of assessment and materiality; inconsistent levels of disclosure; and the lack of industry standardisation. Subsequently, there is significant opportunity for active management to add value.

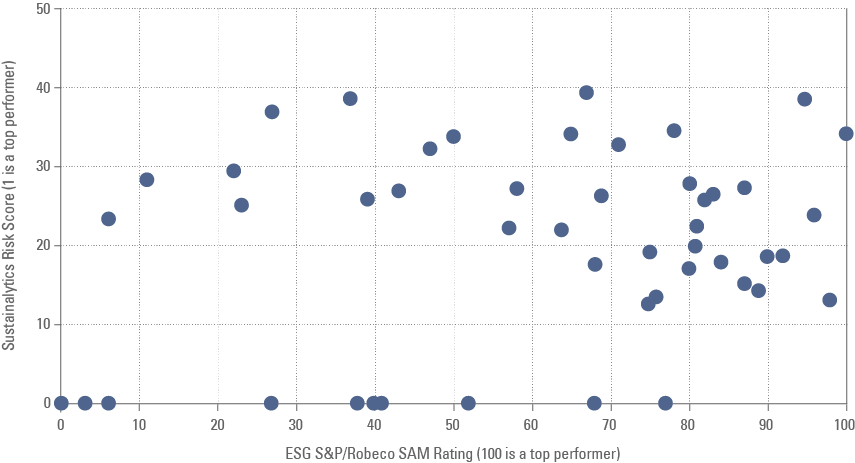

As we detail further below, Ashmore has established an ESG scoring framework. A comparison of our EM Equity portfolio scores to third-party rating providers exhibits a low correlation and highlights that primary research and proprietary assessment is a prerequisite to truly understand the business ESG risk and opportunity. It is also noteworthy that approximately 20% of the portfolio holdings are not covered by either rating provider.

Figure 3: Ashmore EM Equity ESG portfolio: Sustainalytics vs. Robeco SAM ratings

CHALLENGE 2

How to standardise a proprietary approach?

The assessment of a company’s ESG performance is fundamental to the stock research process. It is therefore best undertaken by the stock analyst who is assessing all the company’s fundamentals; not least for the investment team to benefit from the analyst’s accumulation of knowledge during the process.

How can this analysis be implemented on a consistent basis, similar to financial analysis?

Our solution is a standardised scoring framework which is underpinned by several principles. For instance, companies should be penalised for a poor track record of ESG performance yet be rewarded should they acknowledge areas of weakness and strive to improve. Scoring is on an absolute global basis, rather than in comparison to EM or industry peers, which promotes a ‘best-in-class’ assessment mind-set.

Guidelines set out the parameters for what should be considered best and worst practice. They also ensure consistent application across investments by analysts as the subjective nature of scoring may otherwise risk scores gravitating towards the mean, thus eroding their impact.

CHALLENGE 3

How to overcome poor data disclosure?

Data disclosure in Emerging Markets varies meaningfully. While some companies have world class disclosure, others are relatively new to the requirements demanded by institutional investors.

Figure 4: Data disclosure excerpt

Absent or poor disclosure can make it challenging to map a company’s ESG performance. Consequently, a deep understanding of the company is imperative to be able to ascertain their likely underlying exposures and also to build a view on their trajectory.

By simply excluding, or excessively penalising, stocks given poor disclosure risks penalising smaller companies (who may not have the capacity to generate large quantities of data) and it runs contrary to our belief in engaging to enact positive change. It may also fail to recognise a company’s wider contribution to sustainable development. A good example of this is Yunnan Energy.

CASE STUDY

Chinese battery wet separator manufacturer Yunnan Energy

The wet separator is a critical component used in the Electric Vehicle (EV) value chain and Yunnan Energy is a global leader in its industry. However, the company has poor ESG disclosure. By undertaking detailed analysis on the company’s operations, their carbon intensity can be estimated and a stock that directly benefits from policy to promote EV can avoid being potentially screened out based on poor disclosure. In parallel, educational engagement with the company can lead to improved disclosure in future.

The same principle applies when considering the carbon footprint of a software company with poor disclosure. The nature of their business is likely to have a limited carbon footprint and whose impact can likely be proxied by peers.

CHALLENGE 4

Why is materiality so important?

ESG factor analysis is multifaceted and the importance of different factors will vary by industry and company. For example, the factors that matter most for a polluting energy company will likely be very different compared to those for a labour-intensive industry. Consequently, an assessment of materiality is key.

What is the correct framework to appraise a company that scores poorly on certain ESG metrics, yet provides a key, non-replicable material / service in an industry at the epicentre of the drive for greater global sustainability? We provide a case study solution below.

CASE STUDY

Solar glass manufacturer

A common thread through this paper has been the solar Photovoltaics (PV) manufacturing process. Let us now consider solar glass production, which is used as the cover of polysilicon (the raw material used in solar cells) yet is highly energy intensive.

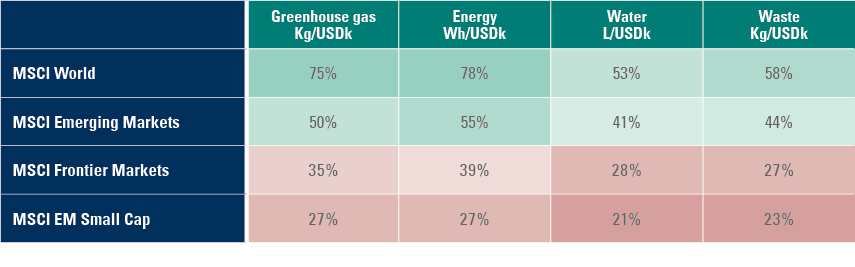

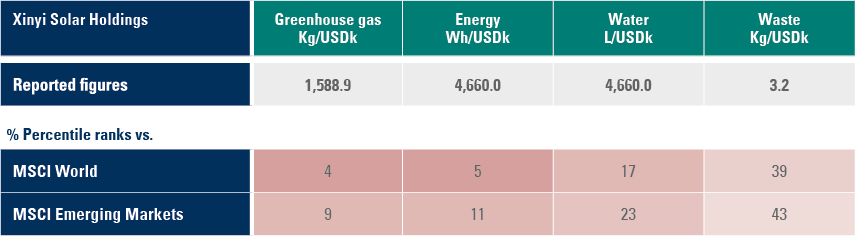

For example, Xinyi Solar, the largest producer globally, emits approximately 2m tons of greenhouse gas emissions (direct based on tonnes of CO2 equivalent or 1,600kg per $k revenue). This carbon intensity ranks in the bottom decile compared to global materials companies. The company also performs poorly across water usage and to some extent waste given the challenges associated with recycling the modules.

Figure 5: Global cross industry comparison

Source: Ashmore, Xinyi Solar, Bloomberg 2021

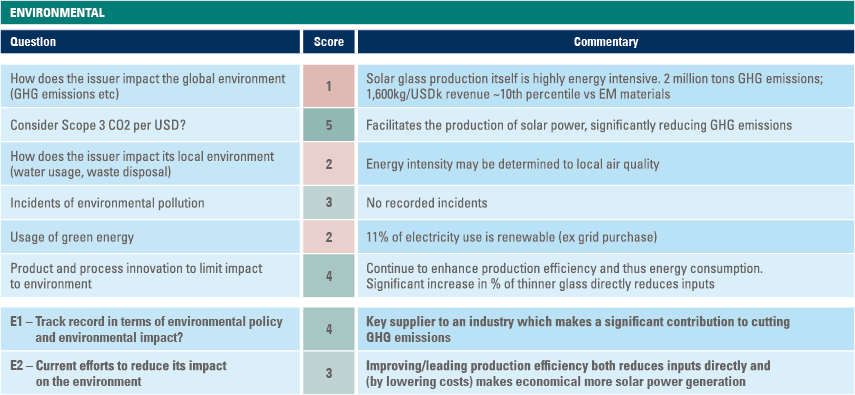

However, there are currently limited alternatives to this glass which indirectly enables approximately one third of global solar capacity, a critical tool in global climate action. While the poor carbon intensity should see the company penalised in an ESG score, and be a driver for engagement to improve, the overall ESG performance of the company should recognise its positive associated contribution to the environment. In the Ashmore scorecard extract, the company scores poorly on some measures, however this does not dominate the overall environment score and therefore portfolio eligibility.

Figure 6: Extract from Ashmore ESG scorecard for Xinyi Solar (1-5 low to high score)

Source: Ashmore 2022

CHALLENGE 5

How to deal with supply chain risk?

The supply chains of many of the world’s largest companies are based in Emerging Markets. Such supply chains are complex and can carry significant, often hidden, risk. If they are not properly analysed and assessed, they risk undermining optically strong, sustainability-focused, investments.

CASE STUDY

Cobalt and the Electric Vehicle supply chain

A key component in the Electric Vehicle battery supply chain is the cathode, which is commonly produced from cobalt, lithium, nickel and manganese (NCM). Approximately 70% of cobalt is currently produced in the Democratic Republic of Congo (DRC) where artisanal miners are responsible for around 20% of production (Source: Wilson Center). In the DRC there have been several reports of dangerous working conditions, human rights abuses and environmental damage.

While some companies have adopted policies to promote higher ethical standards, the several layers of refining mean ascertaining the origin and traceability of cobalt from different suppliers is difficult. Given the strategically important nature of the EV industry in the drive for global sustainability, excluding EV from the investable universe on this basis is a suboptimal solution. This is particularly relevant for EM investors given the leading global EV battery suppliers are primarily based in in China and South Korea.

CASE STUDY

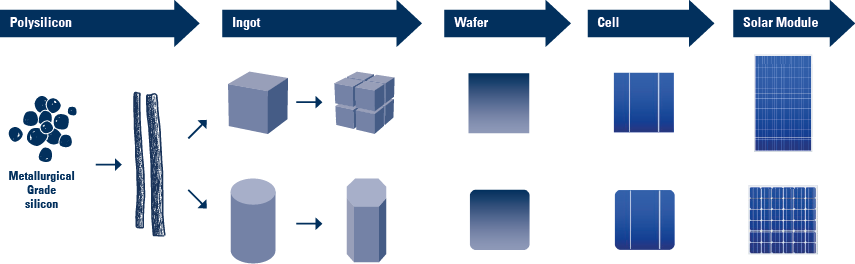

Solar modules and polysilicon

On the surface, investing in solar cell manufacturers looks compelling; for example China’s solar power generation is forecast to double from 2020 to 2025 (Source: Xinyi Solar). However, the manufacturing process comprises multiple processes and suppliers, and carries with it material risk, which requires in-depth analysis to truly assess.

The raw material component for solar photovoltaics (PV) is polysilicon, a high-purity form of silicon. The raw material’s production is concentrated in the Xinjiang region of China at over 50% of the globe’s supply given the region’s low cost supply of electricity and generous government subsidies. The region, however, is at the epicentre of allegations of human rights abuses in particular against Uyghurs ethnic minorities, with associated supply chain vulnerabilities.

Figure 7: Data Solar PV manufacturing supply chain

Source: Xinyi Solar 2022

To assess and minimise the associated risks adequately, a number of steps need to be undertaken. Primary research helps to identify high risk suppliers, which can be mapped to the module production companies and in turn eliminated from the investment universe. Engagement with management teams can also help to promote robust policies, third party verification audits and a strategy of sourcing away from high-risk suppliers.

The strongest examples of supply chain management tend to incorporate some of the following processes:

- the categorisation of suppliers by risk;

- the performance of on-site audits and consultations;

- the promotion of high standards across the supply chain via engagement;

- third-party verification of the processes.

CHALLENGE 6

How to make ESG count in portfolio construction?

Integration of ESG into an investment process is multifaceted through a combination of country and industry analysis, business exposure, corporate policies and its impact on the company’s financials. The ESG assessment is quantified in financial forecasts, revenues, margins and capital expenditure. The valuation cost of capital is also impacted to reflect ESG risk exposure. The ESG risk / opportunity, consequently, will help to determine final position sizing.

ESG integration can be combined with other responsible investment levers. This includes negative screening, such as industry/stock exclusion, although this poses the question what is an appropriate basis for exclusion? Some industries can be considered ‘non-redeeming’ and hence businesses that one would not want to provide liquidity to. Ashmore’s group-wide exclusions are Controversial Weapons and Pornography. There are also those industries that have high negative externalities, such as Defence, Tobacco, Gambling and Fossil Fuels, which are excluded from Ashmore’s ESG-labelled strategies.

An effective approach is through building strong dialogue with companies to influence ESG performance positively. In our opinion, nowhere does this likely matter more than in Emerging Markets. This is why Ashmore is using engagement with issuers as a key lever to influence companies both to manage ESG risks and sustainability impacts.

CHALLENGE 7

How to effectively engage?

Ashmore approaches engagement in principally two ways.3 One approach, typically led by our Responsible Investing function, focuses on collaboration with other investors, as well as participation in relevant industry initiatives. This can be an effective lever for change, although such efforts tend to target a select group of companies only. Another method, which is typically led by the Portfolio Manager and forms the majority of Ashmore’s engagements, is through bilateral engagement directly with a company. Such engagement activities are typically triggered by the identification of unintended ESG risks or sustainability issues and an engagement objective is determined in advance and the outcome monitored. Across the many Emerging Markets where Ashmore invests, we see large variances in the availability and quality of disclosure, as well as in the understanding of and emphasis on sustainability issues.

CASE STUDY

Brazil, Taiwan and India

We engaged with a Brazilian software company to reduce employee turnover which we deemed to be excessive. We identified several measures, such as improving employee training, to help improve the working environment which in turn should help enhance the sustainability of the business.

In the case of a Taiwanese electronics company, we voted, alongside dialogue with management, against the election of certain board members linked to our engagement requesting for more board independence. In another example, which in this case is a collaborative engagement with two other asset managers, we requested a private Indian bank phase out the financing of GHG intensive projects and publicly commit to a timeframe to achieve this goal.

Conclusion

The consideration of ESG factors is critical to successful investing in Emerging Markets. The incorporation of non-financial factors in an investment process is fundamental to building a robust understanding and assessment of a company, which, over time, will improve investment performance, promote better corporate business models and help foster more sustainable economic development.

Successful ESG integration, though, requires several challenges to be considered and overcome within a consistent and standardised framework. Such requirements are only likely to become more apparent to investors as approaches to ESG integration are assessed more stringently in the industry. In Ashmore’s case, we adopt an Emerging Markets tailored solution reflecting our deep specialisation and long experience managing across transformative parts of the world.