- Markets are risk-on this morning on lower oil prices.

- El Niño is officially underway, according to US government agency NOAA.

- European Central Bank hiked rates for first time in three years.

- US CPI inflation in line with expectations; jobs data came in stronger than expected.

- Beijing announced higher infrastructure capex as fixed asset investment dropped.

- Korean exports rose 46.1% yoy in first 10 days of June.

- S&P raised Argentina's long-term rating by one notch to ‘B-’ with a stable outlook.

- In Colombia, de la Espriella consolidated his lead ahead of 21 June runoff.

- Keiko Fujimori is the likely winner of the Peruvian runoff as per the latest results.

- Putin rejected Zelenskyy's request for direct talks and restated his demand for Donbas.

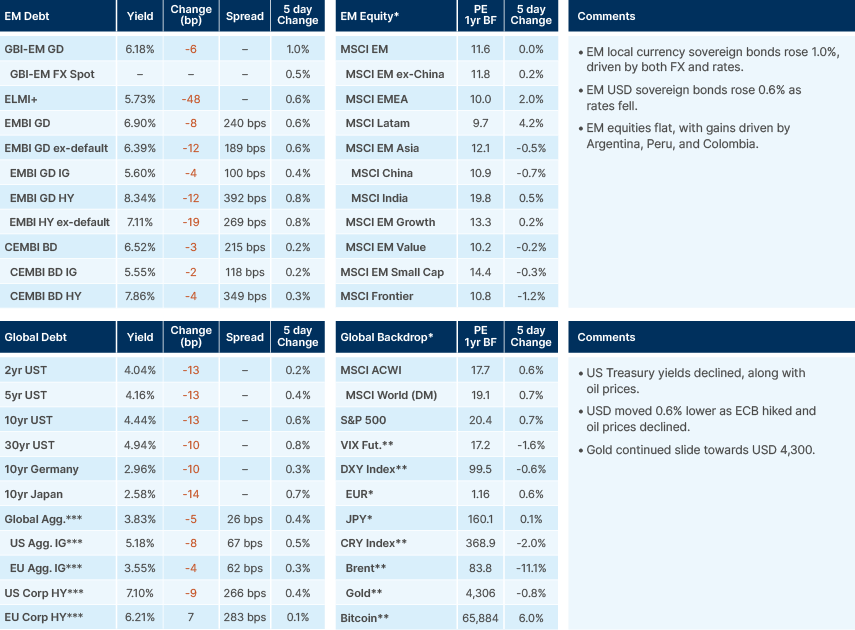

Last week performance and comments

Global Macro

Markets are trading risk-on as the week begins after US President Trump and third parties such as Pakistan indicated that an agreement for a ceasefire extension will be signed on Friday, including a full reopening of the Strait of Hormuz. Brent oil prices are down to around USD 83 per barrel, the lowest since the early days of the conflict in March. This agreement is closer to a memorandum of understanding (MOU) than a final deal and negotiations on Tehran’s nuclear program will continue. However, all markets really care about at this stage is the Strait opening. ‘Deal or no deal’ oscillations have been incessant over recent weeks and months, but oil prices dropping this quickly is clearly an important signal. GPS data shows that traffic through the Strait also increased materially last week with signs that stress in physical oil and product markets is abating.

The US government weather agency NOAA1 declared an El Niño is officially underway, with 63% odds of a “very strong” event this year. El Niño weather events are typically inflationary via higher agricultural commodity prices, particularly rice, corn, wheat and sugar. The regions most exposed are South and Southeast Asia, notably India and Thailand. However, South America can also suffer from reduced rainfall and hotter temperatures. Weather patterns will be key to monitor for the rest of the year and may become the dominant swing factor in current accounts for various emerging market (EM) countries with knock on effects on FX and rates.

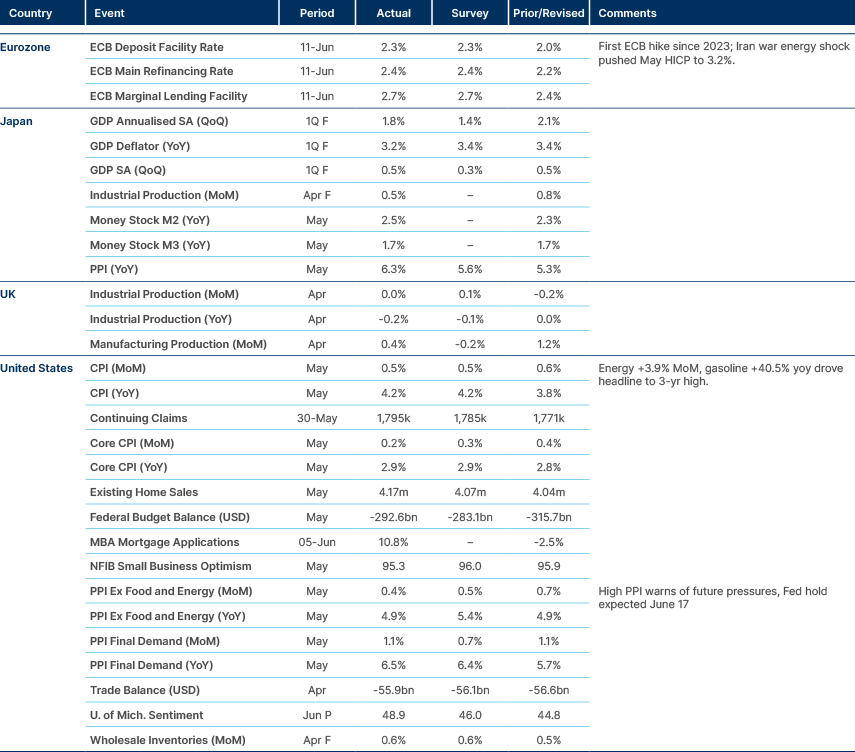

The European Central Bank (ECB) hiked its key interest rates by 25 basis points (bps) last week to 2.25%, due to higher inflation. The market is pricing one further hike for the year, the ECB’s policy statement highlighted data dependency and meeting-by-meeting decisions, as usual. The market is expecting the Bank of Japan to also hike this week. This week’s first US Federal Open Market Committee meeting (FOMC) under new Fed Chair Kevin Warsh is unlikely to see a change in rates, but possibly a continuation of the hawkish commentary we have seen in recent months, with the bias towards easing removed.

US consumer price index (CPI) inflation came in line with expectations last week at 4.15% yoy. Given the drop in oil prices, this may well be the peak. The one-year breakeven declined last week, back to 2.4%, as the leading indicator Truflation remained below 2.0%. Perhaps more surprising was the strength of payrolls in recent months, which seem to have broken their downtrend and are flagging a recovery in cyclical industries. However, average hourly earnings remain flat and higher energy prices continue to erode purchasing power as a result.

US jobs data improving is an important signal, but so is the global credit impulse which, according to UBS, is now at around 1.3% of GDP having still been negative in late 2025 after dropping to -4% in late 2023. The global figure is primarily a US story and mostly bank loans to both households (45%) and corporates (55%).

OpenAI is reportedly considering drastic price cuts as it seeks to win customers from Anthropic, lowering token prices in anticipation of similar cuts it expects Anthropic to deliver. The move follows growing pushback from business executives, who have started to balk at the high prices for AI usage. Sam Altman acknowledged that costs have become "a huge issue", adding that "I think we'll have a lot of ways we can help people get more value for less spend". Separately, Claude's Fable (Mythos with guardrails) has been disabled due to security breach concerns.

In China, H-shares have underperformed A-shares and regional peers, with the divergence most visible in ‘China Tech’: HSTECH and KWEB are the biggest laggards, while STAR50 has led the rally and printed a new all-time high in May. The A-H tech divergence is driven by the same force behind the rally in semis – investors prefer pure AI hardware exposure, which in China is predominantly listed onshore.

Emerging Markets

Asia

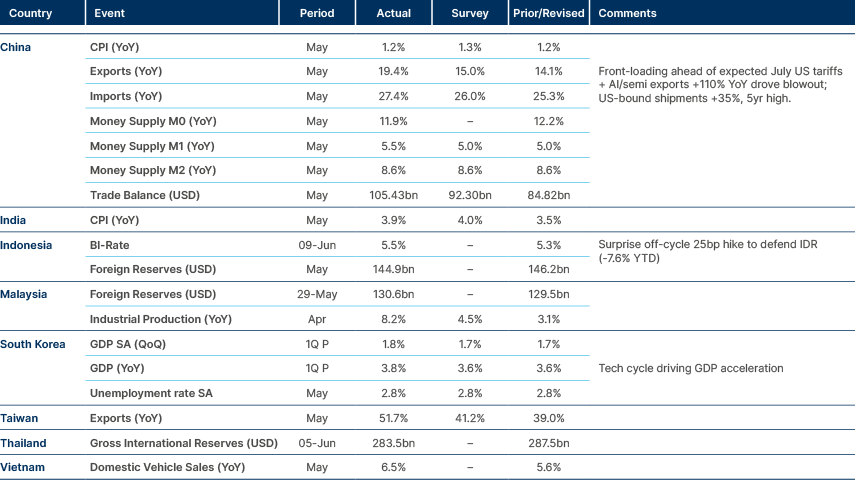

Indonesia hikes rates, Chinese and South Korean exports surge.

China: Beijing has shifted decisively into implementation mode after a visible slowdown in fixed asset investment, with three high profile project launches landing in quick succession. The Three Gorges waterway project (~RMB 77bn) is the headline infrastructure piece, the data centre buildout (~RMB 2trn) underwrites the domestic AI strategy and ties into the onshore hardware bid, and a renewed push on urban renewal extends the property adjacent stimulus channel that authorities have favoured over direct household transfers. Taken together these initiatives flesh out the Six Networks framework which carries a planned investment envelope of more than RMB 7trn for the year, signalling that policymakers intend to backstop growth through state directed capex rather than wait for organic demand recovery.

Indonesia: Indonesia is awaiting an MSCI verdict that, if adverse, risks up to USD 13bn in passive outflows. The trigger is the index provider's review of recently introduced market structure rules and short selling restrictions which have raised questions about Indonesian equities' standing within EM benchmarks. The risk is asymmetric for IDR and local rates, given how much of the foreign positioning is index driven, and the decision date is worth flagging on the calendar as a discrete event risk.

Philippines: Acting Senate President Sherwin Gatchalian confirmed that a 16-member majority will be required to convict Vice President Sara Duterte at the 6 July impeachment trial, even with only 22 of 24 senators able to attend. The arithmetic is consequential because conviction would remove Duterte from office and bar her from the 2028 presidential race, ending the dynastic challenge to the Marcos camp ahead of midterm politics. The maths leaves the outcome live, but the threshold is high in a chamber where Duterte allies retain a workable bloc. The trial is therefore a key political risk event in the regional calendar.

South Korea: Korean exports rose 46.1% yoy in the first 10 days of June, on a business day-adjusted basis, with semiconductors continuing to lead and China and the US absorbing the bulk of the surge. Imports were up 35.6% yoy, leaving an early month trade surplus of USD 5.28bn. Bank of Korea (BOK) Governor Shin Hyun-song reaffirmed a hawkish stance, arguing rates should rise without delay to protect price stability, which keeps the BOK as one of the more aggressively positioned Asian central banks heading into H2. The tech complex remained the dominant macro signal: Samsung is reportedly in talks to fabricate part of Google's most advanced AI chip on its 2nm process and is planning a new advanced packaging plant in Gwangju, while Nvidia deepened partnerships with SK Hynix, SK Telecom, Naver and Doosan, extending the Korean leg of the AI supply chain.

On the political front, President Lee Jae-myung's approval rating fell below 60% for the first time in four months to 57% per Gallup, with the ballot paper crisis driving the slippage. The ruling Democratic Party slipped to 41% against the opposition PPP at 29%, still a comfortable lead, but narrowing. Lee also flagged higher property holding taxes on multi home owners, with details due in July alongside the 2027 budget framework, a signal that the housing cooling agenda remains live and could weigh on construction and household sentiment into year end.

Taiwan: TSMC reported a 30% yoy rise in May sales to NT$ 416.98bn (USD 13.2bn), with combined April–May revenue up around 24% on the prior year and market expectations looking for a roughly 35% increase in second quarter sales. The print extends the foundry's reacceleration and continues to validate the AI hardware leadership thesis that has driven the divergence between A-shares' STAR50 and offshore China tech. For Taiwan macro, the data support the export-led growth story, but also concentrates the cycle in a single name, with implications for index composition and currency dynamics that portfolio managers holding the broader Asia book should keep in mind.

Vietnam: The Politburo mandated a further 5–10% cut in public sector staffing for the 2027–2031 period, alongside wage reform and stricter performance rules. Restructuring under the existing programme had already removed approximately 145,000 positions by end-2025 and is estimated to have saved VND 39trn in recurrent spending. The continued push reflects Hanoi's effort to create fiscal headroom for infrastructure and to streamline the apparatus ahead of the next Party Congress cycle, and is part of a broader supply side reform agenda that has been one of the more credible structural stories in EM Asia.

Latin America

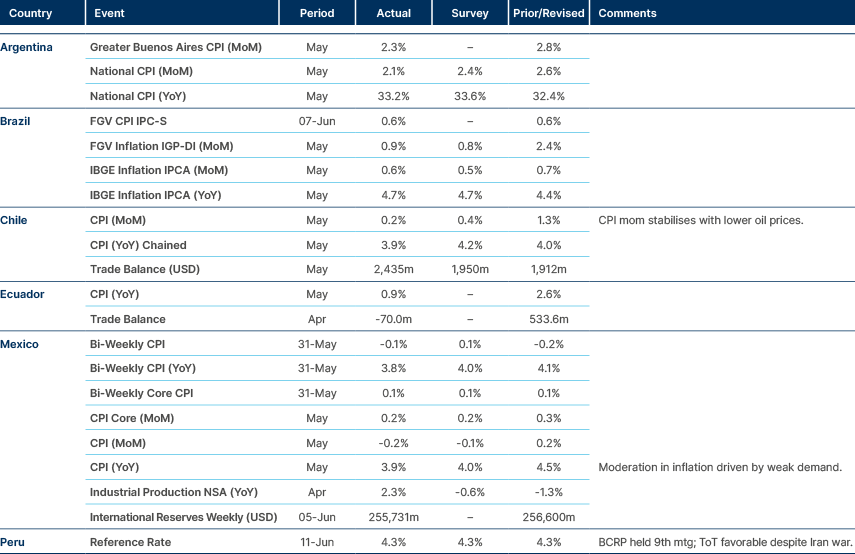

CPI inflation stabilises across region.

Argentina: S&P raised Argentina's long term rating one notch to ‘B-’ from ‘CCC+’ with a stable outlook, citing positive fiscal outcomes and improved access to liquidity. The ratings agency referenced easing economic vulnerabilities and gradually improving external liquidity as the basis for the move, which it judges as setting the stage for continued recovery. The upgrade gradually expands the pool of investors mandated to hold Argentine debt, with mechanical demand implications for spreads. Moody's is now the laggard at sub ‘B-’, but the gap is likely to close before long given the steady accumulation of FX reserves.

Separately, Argentina’s central bank (BCRA) eased FX lending rules and will now allow banks to lend dollars to non-exporting firms for the first time since 2002, subject to FX guarantees from companies with verifiable foreign currency cash flows. The Louis Dreyfus Company, an agricultural goods processor, also committed roughly USD 400m to a soy and sunflower processing plant, with construction starting by end 2026, an incremental but symbolically meaningful foreign direct investment (FDI) vote of confidence in President Javier Milei's macro programme.

Brazil: The Senate approved a rural debt relief bill that the government estimates could cost BRL 140bn, pointing to substantial fiscal slippage if enacted. A presidential veto and Supreme Court challenge are under consideration, but the political optics of opposing rural debt forgiveness are unhelpful. A Senate committee also approved a constitutional amendment granting the central bank (BCB) financial autonomy, though passage this year is unlikely. The combination underlines the perennial tension between fiscal discipline and congressional pressure that continues to set the ceiling on Brazilian risk asset performance.

President Lula widened his runoff lead over Flavio Bolsonaro to 44% versus 38% according to Quaest, helped by the Banco Master scandal and renewed US tariff threats, with the first round lead now at 10pps. The polling drift continues to favour incumbency and dilutes the right's runoff chances, with implications for the policy mix into the back end of the cycle.

Chile: Chile's new government set out a softer fiscal consolidation trajectory, targeting a structural deficit of 2.6% of GDP in 2026 narrowing to 1.5% by 2030, against an earlier pledge of balance by 2030. The 45% of GDP debt anchor was retained unchanged, a mild positive surprise that suggests fiscal anchors remain meaningful even as the glidepath slips. The framework leans on optimistic growth assumptions tied to passage of the omnibus reform bill, which introduces material execution risk. The market is likely to give the credit some benefit of the doubt provided the anchor holds, but the dispersion of outcomes around the 2030 endpoint is wider than the official numbers imply.

Colombia: Aberlardo de la Espriella has consolidated his lead ahead of the 21 June runoff at 52.2% versus 44.5% for Ivan Cepeda according to AtlasIntel, with markets pricing roughly 88% probability of victory. The candidates' platforms are diametrically opposed on monetary architecture: Cepeda has described central bank financing of public spending as a valid discussion, while de la Espriella has floated dollar accounts and eventual dollarisation. The central bank (BanRep) meets on 30 June, nine days after the vote, with May inflation at 5.84% yoy and the debt market pricing 75bps of hikes, leaving it caught between an inflation profile that argues for tightening and a political moment that argues for caution. The runoff outcome will reset Colombian asset pricing across the curve.

Ecuador: President Daniel Noboa reduced the cabinet from 14 to 10 ministries and appointed a new team, a move read in markets as signalling commitment to the International Monetary Fund (IMF) programme's consolidation path. Direct fiscal savings will be marginal against the targeted 6.6% of GDP improvement in the non-oil primary balance by 2028, but the political signal is what matters at this stage. The reshuffle should help maintain disbursement momentum on the IMF programme, which remains the proximate driver of external debt performance.

Mexico: President Trump suggested the US might not renew the USMCA2 agreement, though the Peso shrugged off the comments and the base case remains that the agreement survives a revision now certain to miss the 1 July deadline. Separately, the opposition Institutional Revolutionary Party (PRI) swept all 16 Coahuila legislature seats, a small but symbolically meaningful blow to the MORENA Party ahead of the 2027 midterm elections. The state result will not move the federal balance of power, but does suggest the honeymoon experienced by President Claudia Sheinbaum since she swept into power is fading at the state level, and feeds into the longer term question of whether MORENA can sustain its political dominance into the next cycle.

Panama: Panama authorised emergency imports of 786,000 quintals of rice as El Niño-related shortages left inventories covering consumption only until late September. The imports form part of a wider food security and water conservation response that includes specific measures to protect Canal operations, which remain economically critical and water constrained. The episode is a concrete illustration of how the El Niño weather story is already translating into EM policy responses and current account dynamics, and is worth keeping in mind for the broader Asia and LatAm grain importer complex.

Peru: The Central Bank of Peru (BCRP) held its policy rate at 4.25%, as expected, with headline inflation easing to 3.9% yoy but core inflation stuck at an above-target 4.4%. The core stickiness will keep the BCRP cautious about further cuts even as headline inflation reduces, which supports the carry case for the Sol on a relative basis.

The runoff count remains on a knife edge, with Keiko Fujimori roughly 9,000 votes ahead of Roberto Sanchez at 50.05% to 49.95%, with 98.59% of ballots counted. Challenged tally sheets worth around 1.7% of the total are likely to delay the final result to mid-July. Fujimori is the likely winner given the trajectory of overseas votes, but the closeness of the count guarantees a contested legitimacy backdrop regardless of who prevails, which has implications for governability and the durability of any policy programme.

Venezuela: US investment bank Lazard has undercut Centerview in the contest for the Venezuela financial advisory mandate. According to a Bloomberg-cited letter sent to interim Venezuelan President Delcy Rodríguez, Lazard proposed a fee of USD 25m, a fraction of the at least USD 150m Centerview was negotiating as recently as last month, when Centerview was announced as Venezuela's sole financial adviser. The competitive process around the mandate is itself a signal that the post-Maduro transition is moving into a more orderly restructuring phase.

The US military killed Niño Guerrero, a leader of the Tren de Aragua gang, in a joint operation described as “coordinated closely with our friends in Venezuela”, with the CIA providing the underlying intelligence. The framing of cooperation is the more interesting piece, signalling a working operational channel between Washington and the interim authorities. Protesters have returned to the streets in post-Maduro Venezuela, with reporting capturing the sentiment that they have more freedom to say what they want, suggesting the political opening is being tested in real time.

Central and Eastern Europe

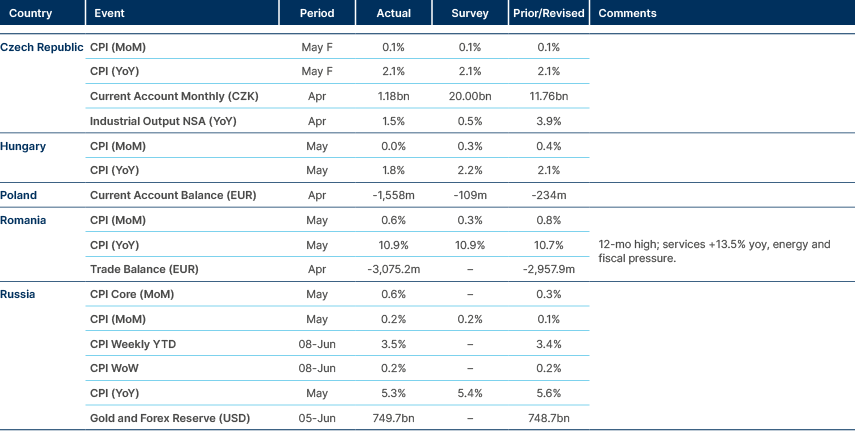

CPI hits 12 month high in Romania.

Czech Republic: The central bank (CNB) Governor Aleš Michl indicated a rate hike on 18 June is a real possibility given excessive money supply growth and elevated core inflation at 2.9% yoy, a day after the ECB's own 25bps move. EmergingMarketWatch sees a 25bps hike as more likely than not — it would be the first under Michl's governorship — followed by a return to wait and see. The shift represents a meaningful change in tone for a governor who has been associated with the dovish side of Central and Eastern European policymaking, and would tighten relative positioning across the region.

Hungary: Hungary’s Government Debt Management Agency (AKK) sold HUF 176.5bn of bonds at auction, with the bulk of the size in 37A's against indicative target sizes of HUF 20bn per maturity. The substantial upsize reflects continued strong domestic appetite for long-end paper and gives the debt agency further runway on its 2026 funding plan, although the structural overweight to one maturity is notable for anyone tracking secondary liquidity at the long end.

Kazakhstan: Kazakhstan signed a critical minerals cooperation memorandum with Saudi Arabia, backing a sector push that includes close to USD 500m of exploration spending over three years. Work began on a 2.5 billion cubic metres (bcm) gas processing plant at Kashagan under a Chinese EPC consortium, with the status of Qatari investor UCC now unclear. KAZ Minerals also unveiled a USD 1.5bn copper smelter project targeting 2030–31 completion. The pipeline of upstream and midstream investment is consistent with the broader Central Asian repositioning towards a more diversified set of strategic partners, and reinforces Kazakhstan's relevance in the critical minerals supply chain flagged previously.

Poland: Prime Minister Donald Tusk said the government will propose a 3% public sector wage rise for 2027, slightly above its 2.5% inflation forecast, and therefore implying a modest real increase ahead of the autumn 2027 elections. There were hints that the final figure could be higher. The pre electoral wage cycle is a familiar pattern and complicates the central bank (NBP)'s policy outlook, particularly given the still-elevated services inflation profile.

Ukraine: President Volodymyr Zelenskyy unveiled plans to roughly double frontline infantry pay to at least UAH 300,000 per month and lift basic soldier wages by a third, with the increases funded by the EU's EUR 90bn package. Parliament raised 2026 defence spending by UAH 1.6trn to UAH 4.4trn, with grant-heavy external assistance narrowing the deficit to 12.1% of GDP from 18.5%. The shift to grants over loans is materially supportive of the debt trajectory, even as headline spending rises.

Russian President Vladimir Putin rejected Zelenskyy's request for direct talks and restated his demand for all of Donbas, with Roman Abramovich reportedly acting as messenger between the sides. Mandatory evacuations began around Kramatorsk and Slovyansk as Russian forces advance. An ECFR poll showed European publics sceptical on both Ukraine's EU membership and post-war peacekeeping, which is a worrying signal on the durability of political support over a longer horizon and complicates the EU package's optical mandate.

Central Asia, Middle East, and Africa

Higher energy prices halt Türkiye’s rate-cutting cycle.

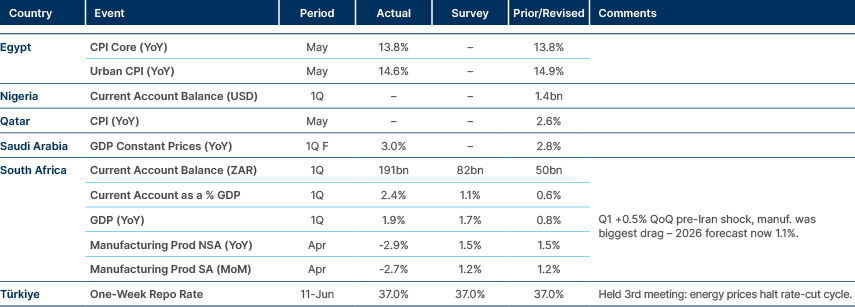

Egypt: Egypt cleared the final USD 440m of arrears to foreign energy companies, down from USD 6.1bn at the peak, with the oil majors already ramping up investment in response. Finance Minister Ahmed Kouchouk put 2026/27 external financing needs at USD 8bn to USD 9bn, with over half concessional and around USD 4bn to be raised from markets, including a planned USD 500m ‘samurai’ bond. The arrears clearance is a meaningful unlock for upstream gas investment, which has been the binding constraint on the external balance, and the funding plan looks manageable given the support framework now in place.

Ghana: President John Mahama's approval rating fell to 58.9% from 68% in December, according to the IEA poll, with electricity supply issues and corruption joining the economy among the leading grievances. The economy still ranks as the top reason for his continued support, but the deterioration in the headline number reflects the wear-and-tear of incumbency in a country where service delivery shortfalls translate quickly into political pressure. The honeymoon is shortening, though no immediate political risk event sits on the horizon.

Morocco: Phosphate giant OCP Group launched a MAD 5bn (USD 540m) perpetual subordinated bond targeted at Moroccan institutional investors to fund green growth initiatives, including the Meskala phosphate mine and additional desalination capacity. The local issuance follows April's 4.6 times oversubscribed USD 1.5bn international hybrid, confirming both deep domestic and international appetite for OCP paper at a time when the credit's strategic position in the global phosphates and fertilisers value chain has been reinforced by geopolitical tensions in competing supply.

Nigeria: The Senate ordered the arrest of former Nigerian National Petroleum Company (NNPC) chief Mele Kyari over an alleged unaccounted NGN 210trn between 2017 and 2023. Kyari's former CFO has rejected the claims as exceeding NNPC's NGN 54.5tn revenue over the period, which suggests the figures in the public domain are politically charged rather than reconciled. Separately, the IMF warned that the planned USD 5bn total return swap with First Abu Dhabi Bank is risky and opaque, recommending Eurobonds or concessional borrowing instead — a notable intervention given Nigeria's reliance on creative financing structures.

The IMF's Article IV urged a neutral fiscal stance, warning that the 2026 deficit would otherwise widen to 4.4% of GDP, and recommended tight monetary policy with inflation still running at 15.7% yoy. Dangote Refinery was valued at USD 39.1bn in a USD 1bn private placement that drew over USD 2bn of interest, as tightening global jet fuel markets boost its exports to Europe. The Dangote valuation is the most concrete EM corporate story of the week, and signals that capital is willing to back Nigerian assets when the operating model is credible, despite the broader macro fragility.

Saudi Arabia: Aramco cut the Arab Light premium for Asia by USD 6.0 mom to USD 9.50 per barrel for July, the second consecutive reduction and a reflection of softer Chinese demand and rival barrels from non-OPEC supply. Red Sea rerouting via the East-West pipeline continues to keep exports flowing, with March oil export revenues up 37% yoy to USD 25bn. The cuts are consistent with the view that the price for volume trade-off is shifting in OPEC's calculus, as cohesion wears and non-OPEC supply continues to surprise to the upside, and they reinforce our cautious stance on the back end of the oil curve.

South Africa: The Q1 2026 current account surplus widened to ZAR 191bn (2.4% of GDP), comfortably above consensus of ZAR 82bn (1.1% of GDP), driven by a larger trade surplus alongside a narrower services deficit on lower service payments, while service receipts were largely flat. Widening of the primary income deficit and a flat secondary income account were absorbed without difficulty. The story remains commodities, though notably not gold this time, with gold exports down from end-2025 levels. The surplus print is Rand supportive on the margin and reinforces the case that South Africa's external accounts are in better shape than the noise around fiscal and structural concerns implies.

Türkiye: The central bank (CBRT) held the policy rate at 37.0% as expected, noting some easing in the underlying inflation trend in May, while flagging energy price and geopolitical risks and, notably, omitting its usual guidance on preliminary June inflation. Treasury and Finance Minister Mehmet Şimşek and CBRT Governor Fatih Karahan reiterated the commitment to push inflation back into single digits, with Şimşek dismissing reserve adequacy concerns and predicting the budget deficit will beat the 3.5% of GDP target. The combination of held rates, removed forward guidance and continued Şimşek-Karahan messaging preserves the orthodox programme's credibility, but leaves the policy mix data-dependent into the summer.

Political risk remains elevated. The prosecutor behind the Imamoglu, Aktas and CHP congress files was reassigned to Ankara, sharpening legal pressure on CHP Party leader Özgur Özel and on fallback candidate Mayor Mansur Yavaş. The Özel-Kilicdaroglu split deepened around the congress route, with a possible 26 July eligibility deadline emerging as the key battlefield. Separately, Chinese EV manufacturer BYD paused its planned USD 1bn Manisa plant after shifting production efforts into Hungary, an incremental negative on the FDI picture though the underlying driver is the EU tariff regime, which allows BYD to bypass trade barriers, rather than anything specific to Türkiye.

Zambia: The 2053 Eurobond buyback gained meaningful creditor support, with a group holding over 25% of the notes accepting the improved 84.35 cents offer backed by a USD 600m African Development Bank (AfDB) facility. The transaction advances the debt-for-energy programme which channels up to USD 275m into grid investment over 15 years. S&P affirmed the ‘CCC+/C’ rating with a stable outlook and treated the buyback as liability management rather than a default event, which is the constructive interpretation for ongoing market access.

The minerals regulator aims to clear approximately 1,600 backlogged mining licence applications by the end of June, supporting the push towards 1 million tonnes of copper output this year and 3 million tonnes by 2031. The licence backlog clearance is the operational unlock needed to translate the country's reserve base into incremental supply growth, and reinforces Zambia's positioning as one of the more credible Africa copper stories.

Developed Markets

US CPI inflation hits three-year high, driven by energy.

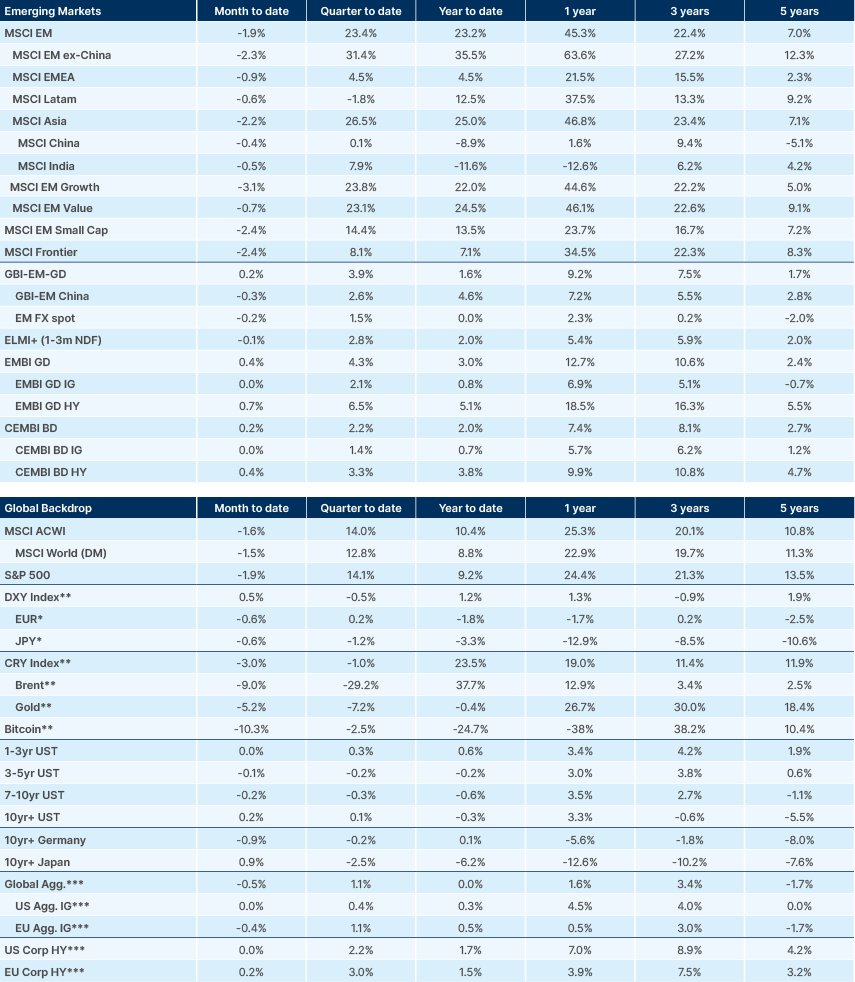

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. National Oceanic and Atmospheric Administration.

2. United States-Mexico-Canada Agreement.