- The US struck Iranian military assets after Trump indicated a preliminary deal was close.

- Positioning in equities increasingly bullish.

- South Korea will use semiconductor tax windfall to seed new sovereign wealth fund.

- Colombian polls suggest a first-round victory for Cepeda, but runoff victory for de la Espriella.

- Polls in Peru have Fujimori at 39% against Sánchez at 35%, ahead of 7 June runoff.

- 73% of Czech farmers are considering scaling back 2026 output.

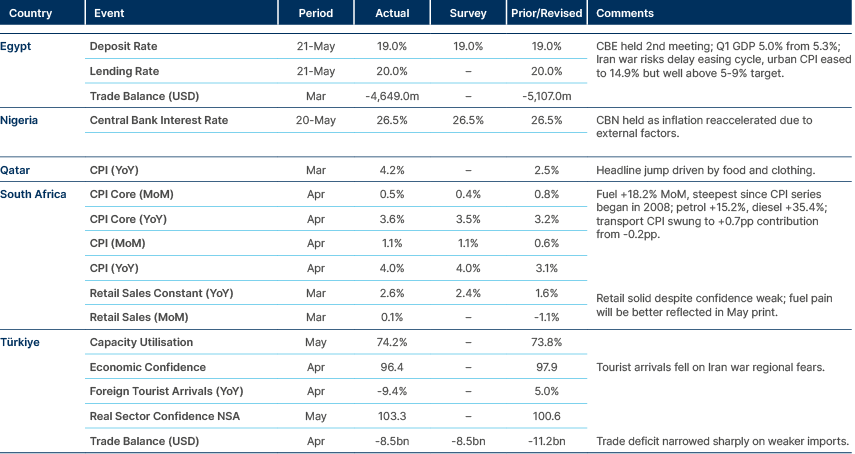

- Rates held in Egypt and Nigeria, despite higher inflation.

- Aramco is reportedly preparing its largest privatisation programme to date.

- Total UAE investment in the US now exceeds USD 1trn, according to ADNOC CEO.

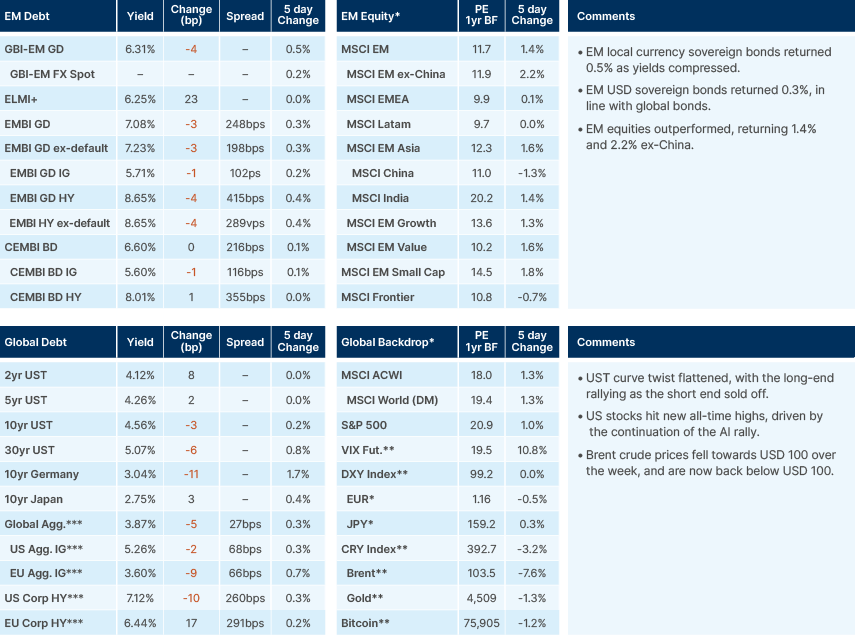

Last week performance and comments

Global Macro

US President Donald Trump said on Saturday that the US and Iran had "largely negotiated" a memorandum of understanding to reopen the Strait of Hormuz. Brent crude fell from Friday's USD 103.54 close to an intraday low of USD 96.02 by Sunday evening. In typical fashion, Trump then changed the mood in a Monday morning Truth Social post ("Great Deal for all or no Deal at all, back to the Battlefront and shooting, but bigger and stronger than ever before"). In New Delhi, US Secretary of State Marco Rubio struck the same conditional tone, saying the US would give diplomacy every chance "before we explore the alternatives." Overnight, US and Israeli jets struck missile launch sites and mine-laying boats in Southern Iran. US Central Command described the action as self-defence and explicitly said the ceasefire still holds. Iran has vowed some form of retaliation, however. Brent sits at USD 97.87 this morning, around 5.5% below Friday.

On substance, there is no real change in language from six weeks ago. The "deal is very close" framing has cycled before and kinetic activity has now resumed. Yet, Trump's jawboning still moves the front of the curve materially. There is some evidence from the Iranian side that we may now be closer to a deal. Iran's ISNA news agency reported Iran was responding to a US text that "has narrowed the gaps." There is also word that China would consider taking Iran’s 60% enriched uranium. Under the 2015 Obama nuclear deal, almost all of Iran’s enriched uranium was transferred to Russia, so this framework has strong precedent.

It is true that with Trump’s approval rating on inflation and the economy at record lows of 25% and 35%, and the FIFA World Cup kicking off in the US on 11 June, the incentive for Trump to wrap up operations in Iran has never been stronger. The sticking points remain Iran's nuclear stockpile, sanctions language, and Strait management. Trump rejected any Iranian toll on transit: "we want it open, we want it free, we don't want tolls." Iran has now changed language around tolls to a “service charge”, legal gymnastics which may make charging for usage permissible under international maritime law. Trackable vessel exits did pick up last week, with three Very Large Crude Carriers (VLCCs) and two liquified natural gas (LNG) tankers exiting bound for China, Pakistan, India and South Korea. This supported lower oil prices, but against pre-war levels, this amount remains negligible.

Christopher Waller, historically one of the more dovish US Federal Reserve (Fed) Board members, turned materially more hawkish on Friday. He said the recent labour market and inflation data had caused him to reassess the balance of risks, with inflation becoming the "driving force" behind monetary policy in the near term. Waller will support removing the easing bias from the statement language and making it clear that "a rate cut is no more likely in the future than a rate increase." Coming from Waller specifically, this is a significant marker on the Federal Open Market Committee (FOMC) and a clear signal that the bar to a near-term cut has moved up.

Central banks more broadly remain on the fence rather than committed to hiking. European Central Bank President (ECB) Christine Lagarde captured the consensus posture last week: "While the energy crisis is pushing up inflation and weighing down on the economy, long-term inflation expectations remain broadly well anchored. The implication of the war for medium-term inflation and economic activity will depend on the intensity and duration of the energy price shock and the scale of its indirect effects." The market-based metrics are consistent with this: 1y breakeven swaps dropped sharply to 2.7% while 10y breakevens remain well-anchored at 2.4% and Truflation sits around 2.0%. The question is whether that picture would survive another six to eight weeks of conflict into the July meetings.

Mega-cap IPOs are on track to push big AI to nearly 50% of US market cap, the highest concentration since the railroads. Bank of America flags consensus max-bullish positioning, with yields breaking up suggesting profit-taking risk here. The Philadelphia Semiconductor Index (SOX) has retraced its correction back to all-time highs and is flashing levels overbought, and the BAML Fund Manager Survey sell signal has triggered on tech after a record jump in equity allocation funded mostly by cash, which has 3.9%. There have been 17 such sell signals since 2002, with average two–three-month losses of 2–3% (60% hit ratio) and 15–20% drawdowns in the worst cases.

The fundamental question remains whether the AI semiconductor bottleneck can sustain the trade. The adoption story is still tracking well: AI is the fastest 0-100m and 100m-1bn user technology on record on a population-adjusted basis. Monetisation is also improving with Anthropic forecasting Q2 2025 to be its first profitable quarter. But the wealth-stocks-boom loop is now in tension with very low consumer confidence, worsening business confidence, equal-weight consumer stocks below global financial crisis-era lows relative to the S&P 500, and AI leaving payrolls intact but real wages compressed.

Emerging Markets

Asia

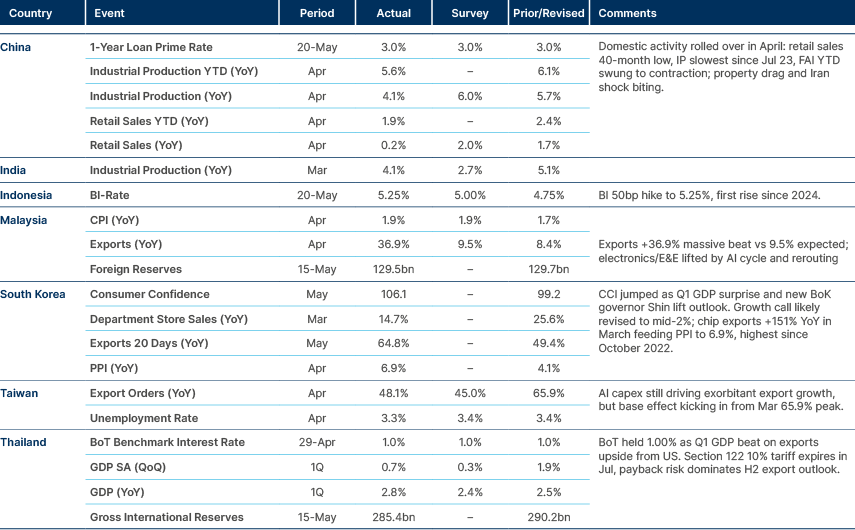

Chinese domestic activity turns weaker, Korean and Taiwan export boom continues.

India: India and the Netherlands signed 17 agreements during Prime Minister Narendra Modi's visit and upgraded ties to a strategic partnership, covering semiconductors, critical minerals, renewables, water and agriculture. The headline deliverable is a Tata Electronics-ASML memorandum of understanding to build India's first front-end semiconductor fabrication plant in Gujarat, an estimated USD 11bn project. Modi then travelled to Sweden, where European Commission (EC) President Ursula von der Leyen reaffirmed the EU's commitment to sign and implement the EU-India free trade agreement this year, with a separate investment pact also under discussion.

Indonesia: S&P warned that Jakarta's plan to centralise the export of crude palm oil, coal and iron alloy through a single new state-owned enterprise (SOE), Danantara Sumberdaya Indonesia, carries material execution risk. Private exporters must transfer buyer contracts to the SOE between June and August, after which foreign buyers will deal directly with the SOE. S&P flagged risks across exports, government revenues and the balance of payments, and noted that businesses are already managing Iran-war supply chain disruptions and shifts in royalties and pricing formulas.

The government's stated aim is to lift the revenue-to-GDP ratio, which has sat around 15% and is a long-standing weakness of the sovereign credit profile. S&P rates Indonesia ‘BBB’/Stable, against Fitch ‘BBB’/Negative and Moody's ‘Baa2’/Negative. A poorly executed rollout risks denting business confidence and investor sentiment further.

Malaysia: The Malaysian Housing Contractors Association said higher diesel prices have pushed construction costs up by as much as 15%, with building material prices rising 20–30%, and some customers are postponing home builds. The construction sector is excluded from the government's targeted diesel subsidy regime, which covers logistics, public transportation and fisheries, and the association is seeking income tax relief. This is a clean read on Iran-war energy pass-through reaching domestic non-tradeable sectors.

South Korea: The government will use part of the semiconductor-driven "super tax revenue" to seed a new sovereign wealth fund with initial capital of nearly KRW 30trn, to be launched later this year. The vehicle is modelled partly on Norway's GPFG and Singapore's Temasek, but will function as a domestic-focused strategic growth fund, taking long-term stakes in later-stage Korean firms in priority sectors. Financing combines in-kind contributions of public enterprise and inheritance tax shares with cash injections to be legislated in June and reflected in the 2027 budget. Critics warn the domestic concentration, alongside the existing KRW 150trn National Growth Fund, risks inflating valuations if capital is misallocated.

One of the 26 Korean ships stranded in the Strait of Hormuz since late February successfully exited under a route proposed by Iran, the first such passage. The HMM-operated tanker Universal Winner carried roughly 2.0 million barrels of crude. Seoul said no tolls or compensation were paid and is working to extricate the remaining 25 vessels, prioritising those with Korean crews and essential cargo. Iran is insisting on its designated routes, raising shipper concerns over both safety and US sanctions exposure, though Seoul judges the current US advisory does not make the transit sanctionable.

Korean power infrastructure firms are scaling rapidly into the US AI data centre buildout. LS Group affiliates Gaon Cable and LS Electric have secured major US AI hyperscaler contracts, with Gaon's US unit Lscus supplying bus ducts worth KRW 50bn this year and potentially KRW 4.0trn over five years, and LS Electric shipping USD 70mn of vacuum circuit breakers. HD Hyundai Marine Solution will supply 33 20-megawatt engines plus maintenance to a Texas data centre project, repurposing marine engines for land-based power generation. Q1 revenue and operating profit rose meaningfully across LS Cable, Gaon Cable and Taihan Cable & Solution. The global power grid market is forecast to more than double from USD 10.98bn in 2025 to USD 24.37bn by 2035.

New Bank of Korea (BOK) Monetary Policy Board member Kim Jin-ill struck a hawkish tone at his inauguration, flagging inflation risks from higher oil prices and financial stability risks around household debt, housing and capital flows. He had previously said he would have preferred the base rate roughly 0.125pp higher than the current 2.50%. He signalled no immediate hike at the next (28 May) meeting, arguing tightening should be gradual and well-telegraphed, and pushed back on simple hawk/dove labels.

Latin America

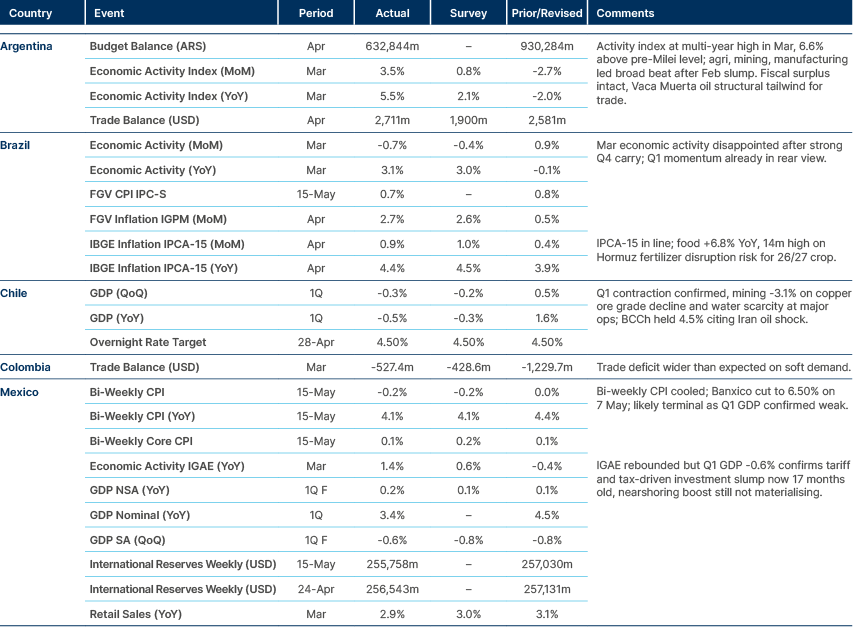

Argentina economic activity growth hits multi-year high.

Argentina: State-controlled YPF announced a USD 25bn Vaca Muerta upstream project, "LLL Oil", across five contiguous blocks, with 1,152 wells planned over 15 years and production reaching 240,000 barrels per day (bpd) by 2032. All crude output will be exported via the new VMOS pipeline, while associated gas remains in the domestic market. YPF estimates annual exports of USD 6bn and more than USD 100bn over the life of the project, with around 6,000 direct jobs in construction. The project has been submitted to the RIGI investment regime, following Chevron's earlier USD 10bn RIGI application.

The rush to submit RIGI applications ahead of the October 2027 elections is rational, given the regime offers fiscal benefits and tax invariability locked in for 30 years and approval can take more than a year. Vaca Muerta is moving from thesis to flow, and the cumulative E&P pipeline is becoming a material structural FX-earner for the sovereign credit profile.

Brazil: BCB Focus analysts raised the end-2026 Selic forecast to 13.25% from 13.00%, implying a smaller 175 basis points (bps) easing cycle this year as the Middle East energy shock continues to pressure prices. A 25bps cut at the mid-June Copom meeting is still expected, which would take Selic to 14.25%. The 2026 IPCA forecast rose to 4.92% (the tenth consecutive weekly increase, well above the 4.50% upper tolerance band), and the 2028 forecast rose to 3.65%, a horizon Copom has flagged as particularly relevant given de-anchoring concerns. GDP and FX forecasts were broadly unchanged.

Senator Flávio Bolsonaro's support in a runoff against President Lula fell 6pps to 41.8% in the May 13-18 Atlas poll, after recordings emerged of his exchanges with disgraced Banco Master owner Daniel Vorcaro. The previously tied runoff now shows Lula leading 48.9% to 41.8%. Some 51.7% of respondents see direct Flávio involvement in the Banco Master scandal, 64.1% say the tapes weakened his campaign, and rejection of Flávio rose to 52.0%, above Lula's 50.6%. Allies are publicly backing him, but reportedly conditioning support on further Banco Master disclosures, and Michelle Bolsonaro remains a possible alternative, though her father-in-law does not appear supportive.

Colombia: First-round polls continue to point to left-wing Historic Pact senator Iván Cepeda winning the 31 May first round in the 37-44% range, but the runoff picture has tightened sharply against him. The Guarumo/Ecoanalítica poll shows Cepeda losing both potential runoffs (39.9% versus 44.8% against Paloma Valencia, and 40.0% versus 43.6% against Abelardo de la Espriella). AtlasIntel shows de la Espriella defeating Cepeda 44.0% to 40.4%, with a Cepeda-Valencia matchup a technical tie. The Colombia Invamer poll remains the outlier, still showing a comfortable Cepeda win.

Hardline right candidate de la Espriella has risen materially, from 18.2% in January to 27.5-32.9% now, on a security-and-crime platform, drawing comparisons with Trump and El Salvador’s Nayib Bukele. Drivers of right-wing momentum cited in the reporting include Gustavo Petro's increasingly confrontational stance towards BanRep, elevated inflation, a widening fiscal deficit, and the suspension of arrest warrants for 29 Clan del Golfo leaders. The decisive variables for the 21 June runoff are how the centrist bloc swings, and whether Valencia voters transfer cleanly to de la Espriella, which surveys are not yet measuring directly.

Mexico: President Claudia Sheinbaum will ask Congress to delay the next judicial election by one year to avoid concurrence with the 2027 midterms, following requests by senior lawmakers and the electoral registry (INE). The reform will also widen the candidate examination process and limit participation, with the stated aim of simplifying the ballot. The risks include narrowing the candidate pool for judges not aligned with the Morena Party, though the bulk of judges up for election are already Morena-aligned. The base case is tighter Morena control over the justice system in this second phase of judicial reform, which continues to weigh on the business climate and investment conditions, even if mostly priced in since 2024.

Peru: The latest Ipsos poll has Keiko Fujimori at 39% ahead of the 7 June runoff against Roberto Sánchez at 35%, a narrow 4pp lead within margin of error. Fujimori gained 1pp from April, Sánchez lost 3pp, and undecideds rose sharply to 12% from 7%. Fujimori dominates Lima (54% versus Sánchez's 23%), while Sánchez retains rural strongholds (49% against Fujimori's 26%, but with undecideds in rural areas jumping to 11% from 3%). The campaign is now in its decisive phase, with Fujimori hardening her security rhetoric and Sánchez likely to moderate parts of his structural reform agenda to pick up undecided voters. Rafael López Aliaga has reiterated he will not back Fujimori, removing one potential consolidation channel.

Central and Eastern Europe

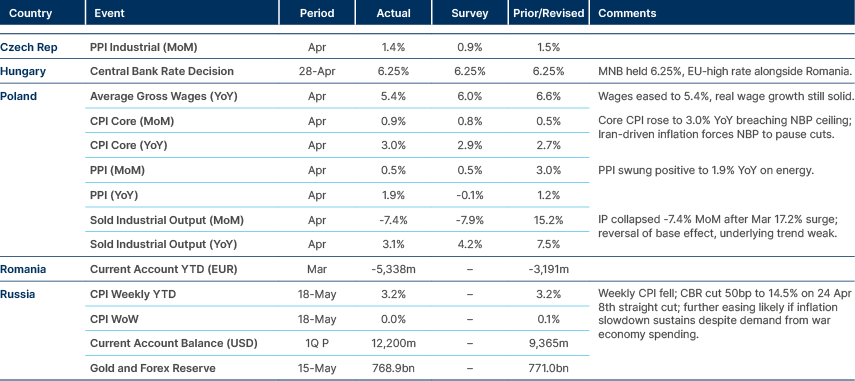

Core CPI inflation in Poland breaches central bank ceiling.

Czech Republic: A Czech Agricultural Association survey found 73% of producers are considering scaling back 2026 output on higher costs, with fertiliser and diesel the two main drivers. Roughly 38% have secured more than 70% of their fertiliser needs, so cost rather than availability is the binding constraint. Fertiliser prices are up an estimated 18-20% on average, and diesel rose 28% mom in March and 6% mom in April. About a third of producers expect production costs to rise 6–10% by year-end, with another half expecting 11–20% or more, averaging around 14–15%.

Assuming partial pass-through, agricultural producer prices could rise 5–10%. Given the 16.9% food weight in the consumer price index (CPI), this implies a headline lift of at least 0.7pp and up to 1.7pp in the worst case, partially mitigated by imports and a firm CZK. The Czech National Bank's August staff forecast looks pivotal, and the real risk is de-anchored household inflation expectations.

Hungary: Prime Minister Péter Magyar warned in Vienna that the budget is in very difficult shape and the 2026 deficit will be very high, while suggesting the previous Fidesz government had falsified the budget, which we read as referring to off-balance-sheet payment commitments on existing contracts not booked as expenditures. Magyar had previously cited unofficial Fidesz numbers showing a 6.8% of GDP deficit versus the 5% official target. The government's review concludes end-June. Magyar reiterated that special taxes cannot be phased out immediately, and markets should read this as implying that the EC's assumption of special-tax removal in 2027, which drives the EC's 5.8% 2027 deficit forecast, is unlikely to hold.

Kazakhstan: The National Bank of Kazakhstan (NBK) will introduce a cap on borrowers' debt-to-income ratios from 2027 at a level equivalent to eight annual incomes, with no differentiation across loan types initially. The existing debt-service-ratio cap at 0.5 (50% of income) will continue alongside. Together with prior macroprudential tightening, the NBK reads retail lending as already cooling and has held back from differentiated caps for now.

Russia's deputy Prime Minister Alexander Novak said an agreement is in place "in principle" for higher Russian crude transit to China via Kazakhstan, rising from 10 million tonnes annually to 12.5 million tonnes. Details are being formalised. The OFAC license extension granted in April runs through 19 March 2027, and Kazakhstan's Energy Ministry is seeking a more permanent arrangement.

Romania: Fitch maintained the country’s ‘BBB-’ rating with a negative outlook and warned that the political crisis following the fall of the Bolojan cabinet materially increases risks to multi-year fiscal consolidation. The ratings agency does not expect early elections, but flagged a lack of clarity on the new government's policy direction. Q1 fiscal performance was strong, with a RON 22bn deficit (1% of GDP), roughly half 2024-25 levels, and the 2026 target is 6.2% of GDP from 7.7% in 2025. Medium-term visibility on the 2027-28 fiscal strategy has deteriorated, and the next rating review is 31 July.

GDP contracted 1.7% yoy in Q1, weaker eurozone demand and higher energy prices likely push 2026 growth below Fitch's earlier 1.1% forecast, and April inflation hit 10.7% yoy, constraining policy room. The country’s recovery and resilience facility (RRF) funds remain critical with 1.8% of GDP still pending (EUR 4.6bn grants, EUR 2.7bn loans). Separately, the caretaker cabinet reported that the National RRP implementation has exceeded 60% with EUR 10bn still to be drawn through requests 5 and 6, and the Health Ministry needs urgent decisions to keep NRRP-financed hospital projects on track for August completion.

Middle East and Africa

Egypt and Nigeria hold interest rates.

Nigeria: The Central Bank of Nigeria (CBN) retained its monetary policy rate at 26.5% with all major policy parameters unchanged. Governor Olayemi Cardoso characterised the recent inflation uptick as temporary and externally driven, and said reforms have shielded Nigeria from Iran-war spillovers. External reserves rose to USD 49.5bn as of 15 May from USD 48.4bn end-April, covering around nine months of imports. Daily FX turnover has risen from around USD 100m at the start of the administration to roughly USD 550m, with some days reaching USD 1bn, and CBN intervention is now only 1.2–1.3% of market turnover. A revised FX Operations Manual is due 1 June.

Separately, Nigeria and the US conducted further joint strikes against Islamic State militants in the northeast on 17 May, following an earlier joint operation that killed ISIS's reported second-in-command in West Africa. Trump has hinted at further strikes if attacks continue. The security cooperation is escalating against the backdrop of his earlier criticism of Nigeria's protection of Christians.

Saudi Arabia: Aramco is reportedly preparing its largest privatisation programme to date, targeting as much as USD 35bn from divestments of energy facilities, infrastructure and potentially real estate. Aramco will retain full upstream control, but will divest minority stakes in mid- and downstream assets. Possible transactions reportedly include sale-and-leasebacks of real estate (including the HQ campus in the Eastern Province), stake sales in export and storage terminals, and deals involving gas-fired power plants and water infrastructure. This builds on last year's USD 11bn BlackRock lease arrangement for the Jafurah gas plant and Riyas NGL fractionation facility.

Pakistan deployed 8,000 troops, a squadron of fighter jets, drones and an air defence system to Saudi Arabia under last year's mutual defence pact, per a Reuters exclusive citing security and government sources. Saudi Arabia is financing the deployment, and the role is primarily advisory and training for now, though the source said numbers could rise materially. Aramco also activated the Kingdom's first quantum computer with Pasqal, a 200-qubit neutral-atom platform with commercial Quantum-Computing-as-a-Service access, positioned within Vision 2030's technology pillars.

UAE: The Abu Dhabi National Oil Company (ADNOC) CEO Sultan Al Jaber said total UAE investment in the US now exceeds USD 1trn, with energy investments alone (ADNOC, XRG and Masdar) above USD 85bn across 19 states. XRG, created in 2024 to consolidate Abu Dhabi's lower-carbon energy and chemicals assets, controls an enterprise-value portfolio above USD 150bn. The US strategy is heavily skewed toward natural gas and LNG: XRG holds an 11.7% stake in Rio Grande LNG Phase 1 and an additional 7.6% in Trains 4-5, with ADNOC Trading on a 20-year, 1.9 million tonnes per year LNG offtake. XRG also holds 35% in ExxonMobil's proposed Baytown low-carbon hydrogen and ammonia facility, and Masdar holds 50% of Terra-Gen.

The West-East Pipeline, designed to double UAE export capacity through Fujairah on the Gulf of Oman and bypass the Strait of Hormuz, is 50% complete with delivery accelerated to 2027. Current Habshan-Fujairah capacity is 1.8mbpd, and the expansion aims to lift this to 3.6mbpd. Al Jaber reiterated the commitment to the USD 150bn five-year capex programme and noted that global spare capacity at around 3mbpd should be closer to 5mbpd. The world drew 250 million barrels from storage in two months, with effective cover now at 30-35 days, and full Hormuz flows are not expected to return before Q1-Q2 2027.

Developed Markets

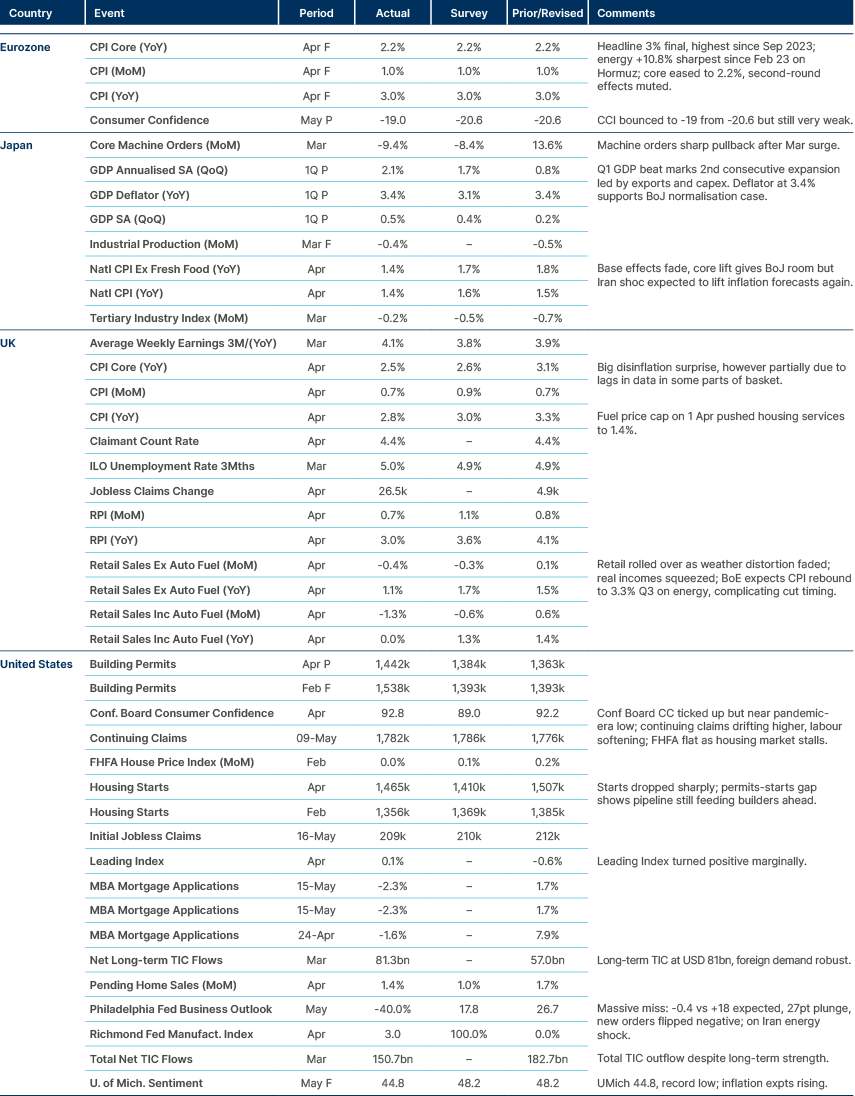

Eurozone inflation back at 3.0%.

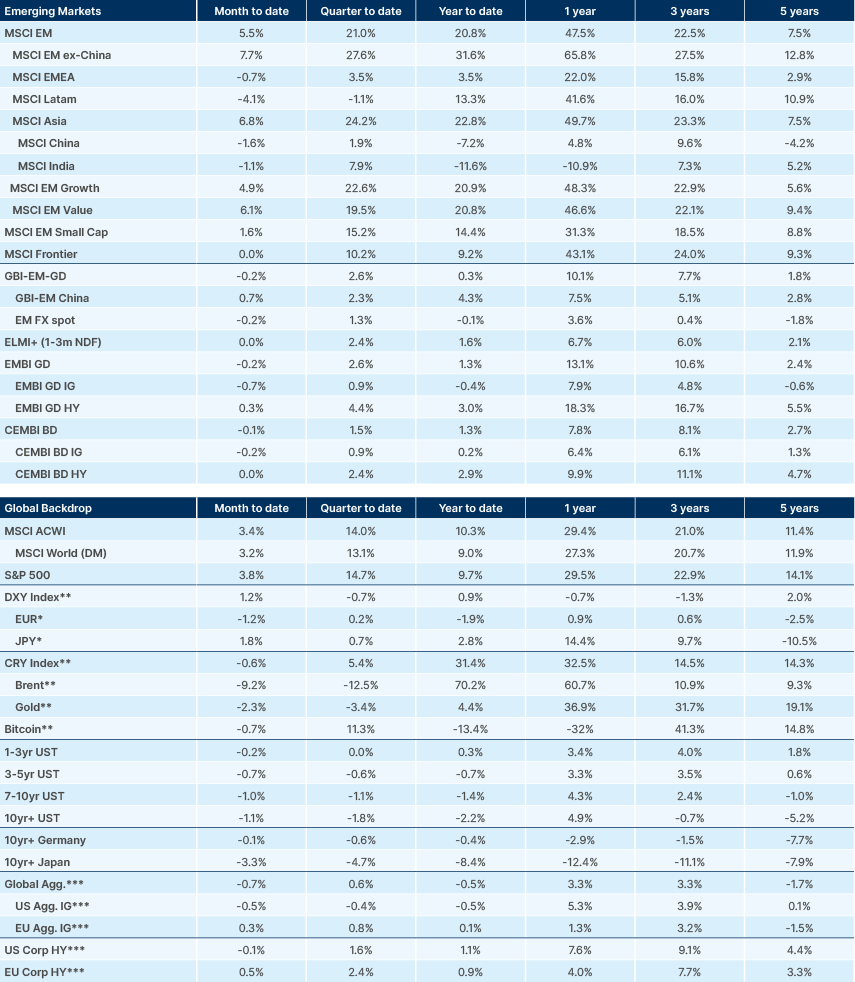

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.