- Risk assets have staged a recovery since last Tuesday, but downside risks elevated.

- President Trump’s deadline tonight for Iran to ‘make a deal’ is a key inflection point

- US nonfarm payrolls came in much stronger than expected, cyclical upswing intact, for now.

- Iran granted ‘friendly’ country status to Philippines, Japan and France, now 10 countries in total.

- Korea’s government launched a two-month crude oil swap system with private refiners

- Brazil Central Bank Governor Galípolo supported the Copom’s conservative stance

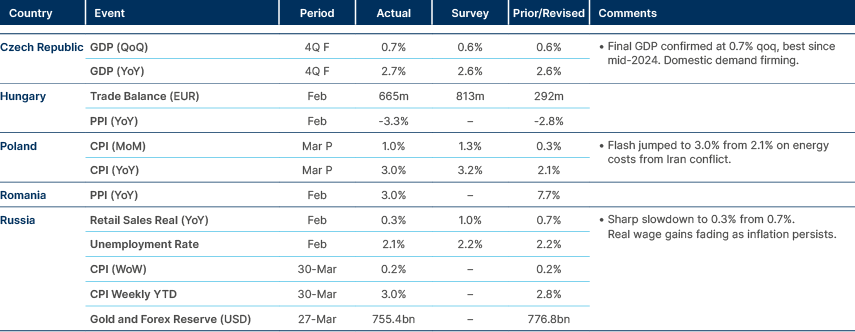

- Hungary intends to maintain the fuel price cap introduced on March 16 as long as possible

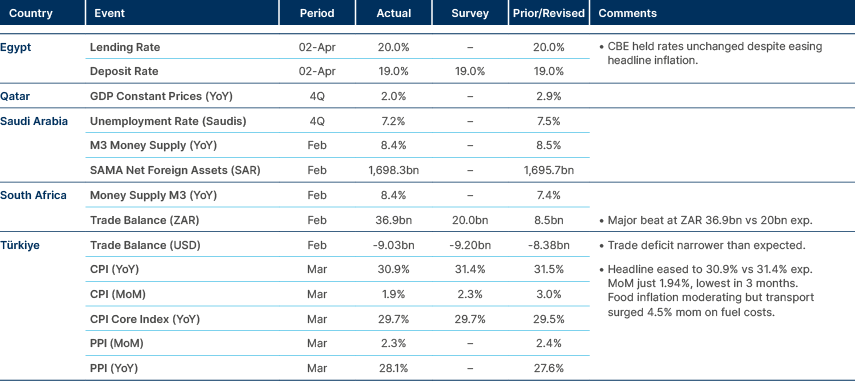

- Egypt’s monetary policy committee kept all rates unchanged on April 2, pausing its easing cycle

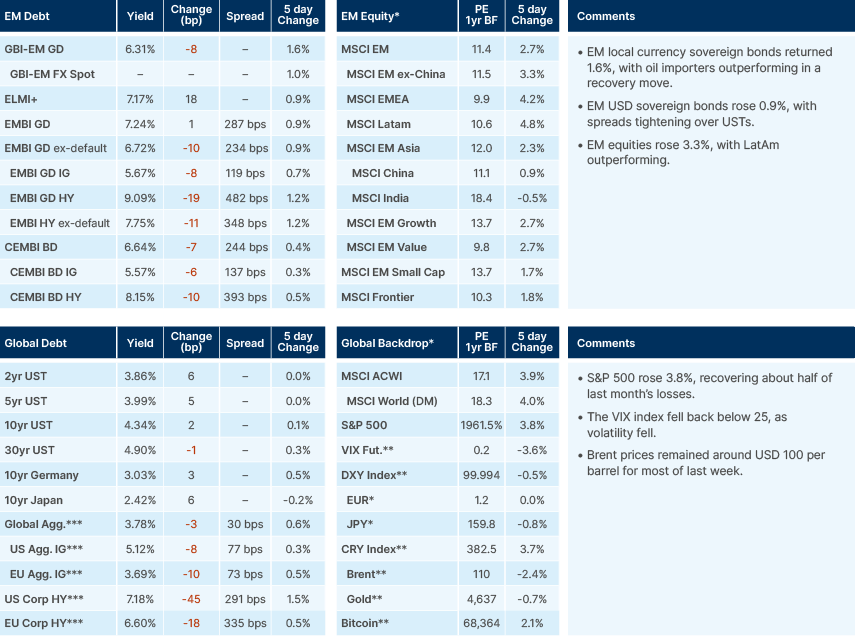

Last week performance and comments

Global Macro

Risk assets began to stage a recovery last week, even as military action across the Middle East intensified. The initial sharpness of the move higher on the 31st of March, particularly in equities, was likely driven by technical factors, with shorts being squeezed and covered as the mood music turned more positive. The catalyst for this shift in tone on Tuesday was US President Donald Trump’s admission that he would end the war in weeks even without a deal with Iran, because his principal objectives had already been achieved. Trump then announced a special White House address on April 1st, and optimism around an imminent ceasefire announcement rose. Reports of progress in multilateral negotiations also continued to filter through.

Market participants hoping for a ‘TACO’ (Trump Always Chickens Out), were disappointed, however. Trump did reiterate he would like the conflict to end in two to three weeks, but suggested escalation until then. This is what is currently playing out, with US and Israeli strikes on Iranian energy infrastructure and bridges being met with retaliatory strikes from Iran on infrastructure in the Gulf. Trump is threatening further, severe, escalation, with the deadline for ramping up strikes on Iranian energy facilities expiring tonight, (Tuesday, at 8pm E.T.) if the Strait of Hormuz doesn’t open. Trump is already calling it “infrastructure day”, reportedly. Today, the US President’s Truth Social posts could be seen as being particularly extreme. All this may well be a very high-octane example of Trump’s ‘art of the deal’ negotiation playbook. However, should Trump follow through with his threats, Iranian retaliation would likely involve the largest strikes in Gulf infrastructure so far, and possibly a full reclosure of access through the Strait, in a bid to drive oil prices higher.

Markets do not seem to be pricing this scenario, currently, and are calling Trump’s bluff even as the deadline approaches. The drop in volatility in recent days is likely for two reasons, in our view. First, some inertia. After a month of derisking, investors are reluctant to take more chips off the table, given the markets’ willingness to move sharply higher on any shreds of good news. There is the very possible risk that a deal may well emerge in the coming days, after an extension of Trump’s most recent deadline. But more importantly, there are signs that ship traffic through the Strait of Hormuz is improving and will continue to do so – barring another leg of escalation between the US and Iran. Ten countries are now on Iran’s ‘friendly list’ for safe Hormuz passage (provided payment of a toll) with the Philippines, Japan and France added last week.

Before the war began, 20 million barrels per day (mbpd) of liquid fuels passed through the Strait of Hormuz, with around 16mbpd being crude oil. Given rerouting of some Saudi and UAE oil away from Hormuz, and International Energy Agency (IEA) inventory drawdowns, Hormuz oil exports only need to reach around 50% of prior levels for a full restoration of global crude oil supply. This would be easily achievable just via demand from the ‘friendly’ countries.’ This is the narrative markets appear to be relying on, however risks of a new cycle of escalation, and another leg lower in risk assets are elevated. Qatar is reporting that its ships were unable to cross the Strait yesterday. Ultimately, what happens next is down to Trump, but today is an undoubtedly pivotal moment in the conflict.

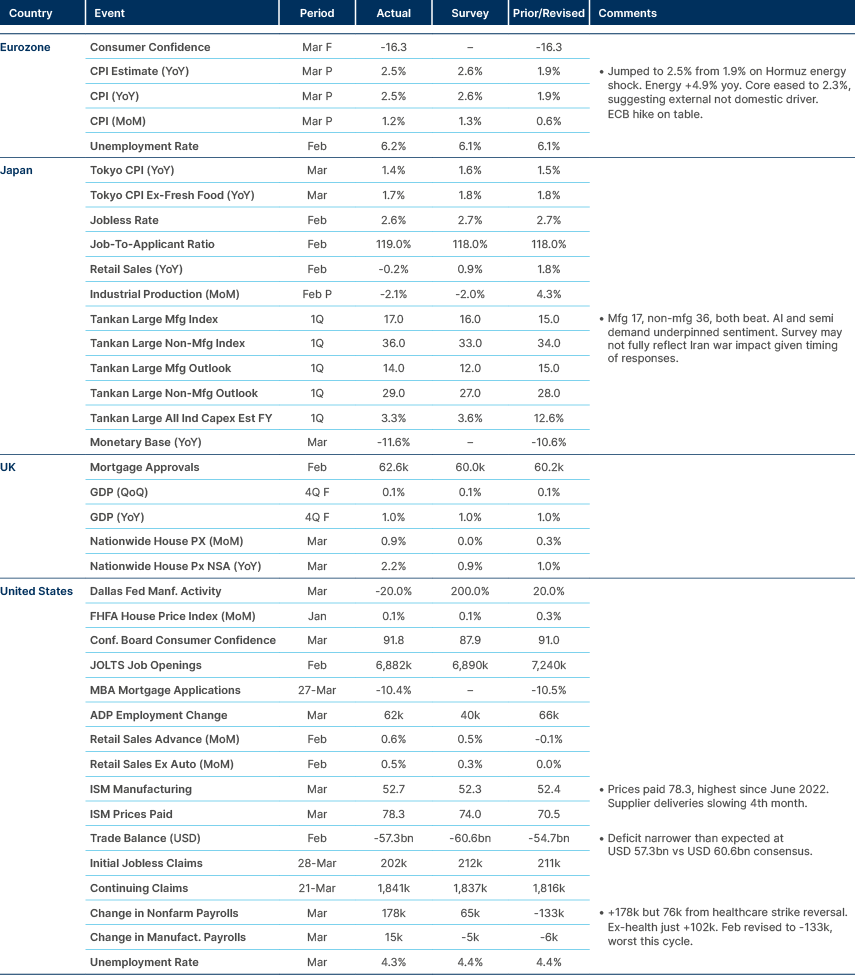

During such a high stakes global conflict, market attention understandably shifts away from macro data releases. However, the US non-farm payrolls came in much stronger than expected, following an upside surprise in manufacturing purchasing manager indices (PMIs) the week prior. The US added 178k jobs in March (vs 78k est) with a notable turnaround in hiring in cyclical industries like trade and transport, manufacturing and construction. On a three-month moving average basis, US hiring ex-healthcare turned positive for the first time since April 2025. We think this is an increasingly important metric for tracking US labour market health, given such a large proportion of hiring is driven by the non-cyclical Healthcare and Social Assistance industry.

The data is more evidence of the continuation of the cyclical recovery underway, a trend which was driving commodity prices higher in the first two months of the year even before conflict in Iran. This recovery in broad manufacturing, rather than just tech, is not just a US trend. Asian PMIs were also at 4.5-year highs coming into February. A recovery in European industry data was also taking root. The mega trends driving stronger manufacturing remain intact for now, and if a resolution In Iran to avert a looming energy crisis can be made, are likely to continue driving markets again. Recent reports from Samsung and TSMC confirm the AI tech supercycle shows no signs of slowing down yet. However, a sustained and more marked move higher in interest rates would make it difficult for interest rate-sensitive industries to continue their upswing. Already, inflation expectations in the US have risen from 2.8% over the next two years to 3.2% (2-year breakeven inflation) and all cuts for this year have been priced out in the US. In Europe, three hikes are now priced till the end of 2026, although this would still only take the reference rate to 2.75%, versus 3.75% in the US. Emerging market (EM) central banks are also broadly likely to pause rate cutting cycles given high levels of uncertainty. However, as we continue to point out, positive real rates across both EM and developed markets (DMs) keep the risk of a global interest rate hiking cycle low, even in the ‘bear’ scenario of a prolonged period of much higher oil prices.

Commodities

OPEC+ confirmed on 5 April that the eight participating countries will return 206k bpd in May from the 1.65mbpd voluntary cuts announced in April 2023. The group retained full flexibility to increase, pause or reverse the phase-out depending on market conditions, and the separate 2.2mbpd cuts from November 2023 remain in place. The statement flagged concern over attacks on energy infrastructure, noting that restoring damaged assets is both costly and slow, and commended countries that have used alternative export routes to maintain supply availability.

The IEA estimates 5.3mbpd of spare capacity across OPEC, with Saudi Arabia holding 3.1m, the UAE 1.1m, Iraq 600k, and Kuwait 400k. In practice, Iraq and Kuwait's spare capacity is largely academic while Hormuz remains constrained, as neither can meaningfully increase exports through the Strait. Saudi Arabia claims 12mbpd of total capacity against roughly 9mbpd of current output but has never actually produced at that level. After the 2019 Abqaiq attack, it took months to restore just 5.7mbpd of disrupted capacity, raising serious questions about the Kingdom's ability to surge from higher baselines under crisis conditions. Independent analysts at Energy Aspects and Rapidan estimate that true deployable spare capacity — production that can be brought online within weeks without major capital expenditure — sits at just 1.5 to 2.5mbpd, concentrated almost entirely in Saudi Arabia and the UAE.

Emerging Markets

Asia

Malaysia: PM Anwar Ibrahim confirmed that state oil company Petronas will ensure sufficient oil and gas deliveries at least through May, though he cautioned that Middle East supply chain disruptions could persist longer than expected. The government has implemented demand management measures including mandatory work-from-home for public sector employees from 15 April, a reduction of RON95 monthly quotas from 300 to 200 litres, and more controlled Eid celebrations to conserve energy.

Iran granted Malaysia free passage through the Strait of Hormuz for seven ships including four oil tankers, a notable diplomatic win for Anwar’s neutral foreign policy positioning. However, Malaysia still relies on the Strait for nearly 50% of its oil supply and there is no confirmation that future deliveries will receive the same treatment, limiting the strategic significance of the concession beyond its immediate symbolic value.

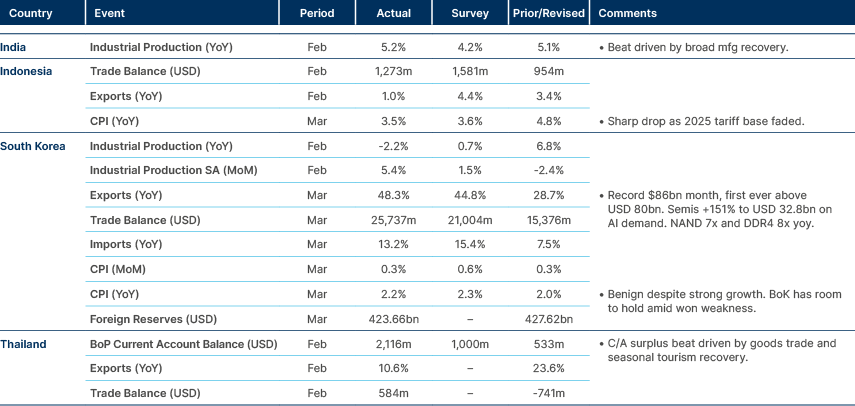

South Korea: The government launched a two-month crude oil swap system with private refiners, lending Middle Eastern crude from national reserves to be replenished later with alternative-sourced oil. Four refiners have applied involving up to 20m barrels. Korea has secured around 50m barrels of alternative crude for April, below the normal 80m barrel monthly import volume but described as manageable given reduced operating rates. A Korean Institute for International Energy Policy analysis warned that oil prices are unlikely to return to pre-war levels even under the most optimistic ceasefire scenario, projecting at least USD 90 per barrel due to damaged infrastructure. In a worst-case scenario with prolonged Hormuz closure, prices could reach USD 117 per barrel.

President Lee Jae Myung and Indonesia’s President Prabowo Subianto elevated bilateral ties to a “special comprehensive strategic partnership,” signing ten memoranda of understanding (MOU) covering critical minerals, defence, AI-based healthcare, and energy cooperation. Lee specifically requested stronger energy ties, citing Indonesia’s role as Korea’s sixth-largest liquefied natural gas (LNG) supplier. Major Korean corporates announced expansion plans in Indonesia including POSCO, Hyundai Motor, LG Energy Solution, and SK Plasma.

Domestically, retail data showed deepening K-shaped consumer polarisation. Department stores were the only major channel to record sales growth in 2025, driven by VIP customers accounting for nearly half of total sales at Lotte, Hyundai, and Shinsegae. Hypermarket sales fell 2% for the first time ever, with double-digit declines in home appliances and living goods. The divergence points to weakening middle-class consumption as higher-income households continue spending on premium offerings while lower-income groups retreat to ultra-low-cost alternatives.

Vietnam: Registered foreign direct investment (FDI) surged 42.9% year-on-year in Q1 2026 to USD 15.2bn, driven by a 2.4-fold jump in newly licensed project capital to USD 10.2bn across 904 projects. The shift toward larger, higher-value investments was notable. Manufacturing attracted 69% of new capital at USD 7.1bn, with power generation second at USD 2.3bn. Singapore led investors at 52% of newly licensed capital followed by South Korea at 36%, reflecting continued build-out of semiconductor-adjacent supply chains. Disbursed FDI hit a five-year Q1 high of USD 5.4bn with manufacturing accounting for 82.8% of disbursements. The key risk is whether energy cost inflation and logistics disruptions from the Middle East conflict slow conversion of pledges into active projects through the remainder of 2026.

Latin America

Argentina: A federal judge with Peronist links suspended most articles of the labour reform pending a constitutionality ruling, accepting a request from the CGT (General Confederation of Labour) The government will likely appeal to a higher labour court where it has a reasonable chance of getting the suspension overturned.

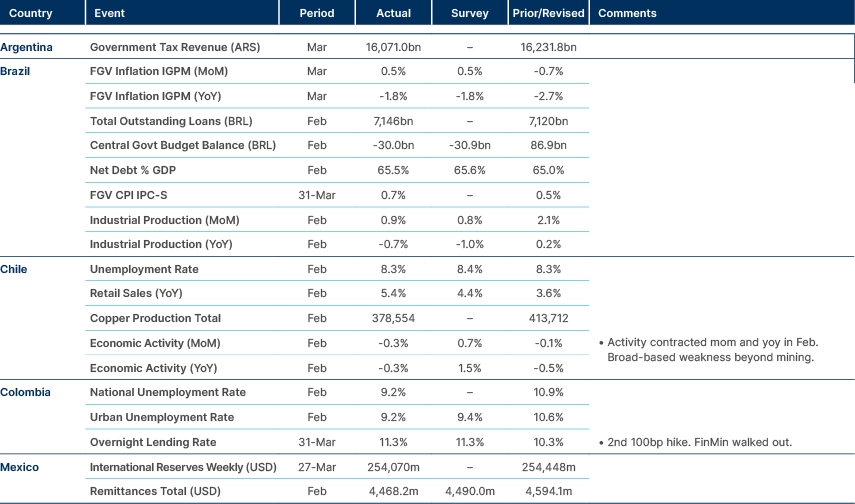

The Economy Ministry rolled over 138% of maturities in its latest auction, a new 2026 high. Demand was particularly strong for inflation-linked notes, reflecting shifting inflation expectations from the oil price shock. The high rollover was driven by bills maturing in 2027 and 2028, unusual for a market that typically prioritises short-dated instruments to stay liquid. The government placed the full USD 300m supply in its USD tranche, with the 2027 bond at 5.00% and the 2028 at 8.52%, the spread reflecting electoral risk. BCRA liquidity injection through USD purchases appears to be feeding through to stronger primary auction demand.

Brazil: President Lula suggested former Education Minister Camilo Santana as a potential successor, signalling that succession planning is becoming a priority. Fernando Haddad, long considered the leading contender, now appears less inclined toward a presidential bid and his tenure at Finance may have weighed on his popularity. It remains too early to determine Lula’s preferred successor, but the remarks reinforce this could well be an increasingly prominent issue as Lula’s age advances.

Central Bank of Brazil (BCB) Governor Gabriel Galípolo supported COPOM’s conservative stance, arguing that the hawkish approach through 2025 left Brazil in a comfortable position to absorb the external energy shock, allowing the start of the easing cycle in March with a 25 basis points (bps) cut to 14.75% even amid higher oil prices. EMW assesses there is room for another 25bps cut at the April meeting, though incoming data on the oil price pass-through will be key to determining the pace beyond that.

Central and Eastern Europe

Hungary: The government intends to maintain the fuel price cap introduced on March 16 for as long as possible, PM Office Head Gergely Gulyás confirmed. The cap has been sustained by releasing strategic reserves sufficient for 45 days of consumption. The National Bank of Hungary (NBH) assumed in its latest inflation report that the cap would be removed in mid-May. The EC has requested immediate removal, which the government rejected. Gulyás implied the government expects stronger bargaining power with Ukraine to reopen the Druzhba oil pipeline if it wins the 12 April elections, allowing unimpeded Russian oil imports and longer sustainability of the cap.

Central Asia, Middle East, and Africa

Egypt: The Monetary Policy Committee (MPC) kept all rates unchanged on 2 April, pausing its easing cycle and adopting a wait-and-see approach given heightened global uncertainty from the Iran war. The surge in energy and agricultural commodity prices driven by supply-route disruptions and elevated freight insurance premia has renewed upward pressures. The Pound has lost 14% since the start of the conflict but appears to have stabilised around USD/EGP 54.5. Capital outflows through the EGX were a relatively muted USD 2.1bn in March, covered by Central Bank FX deposits and commercial banks’ foreign assets.

The MPC revised its GDP growth forecast down to 4.9% for FY 2025/26 from 5.1% at the February meeting and flagged that its Q4 2026 inflation target of 7% +/- 2pps faces increasing upside risks from a prolonged conflict and higher-than-expected fiscal consolidation pass-through. Output is expected to remain below potential for longer, keeping demand-side inflationary pressures subdued in the short term.

Developed Markets

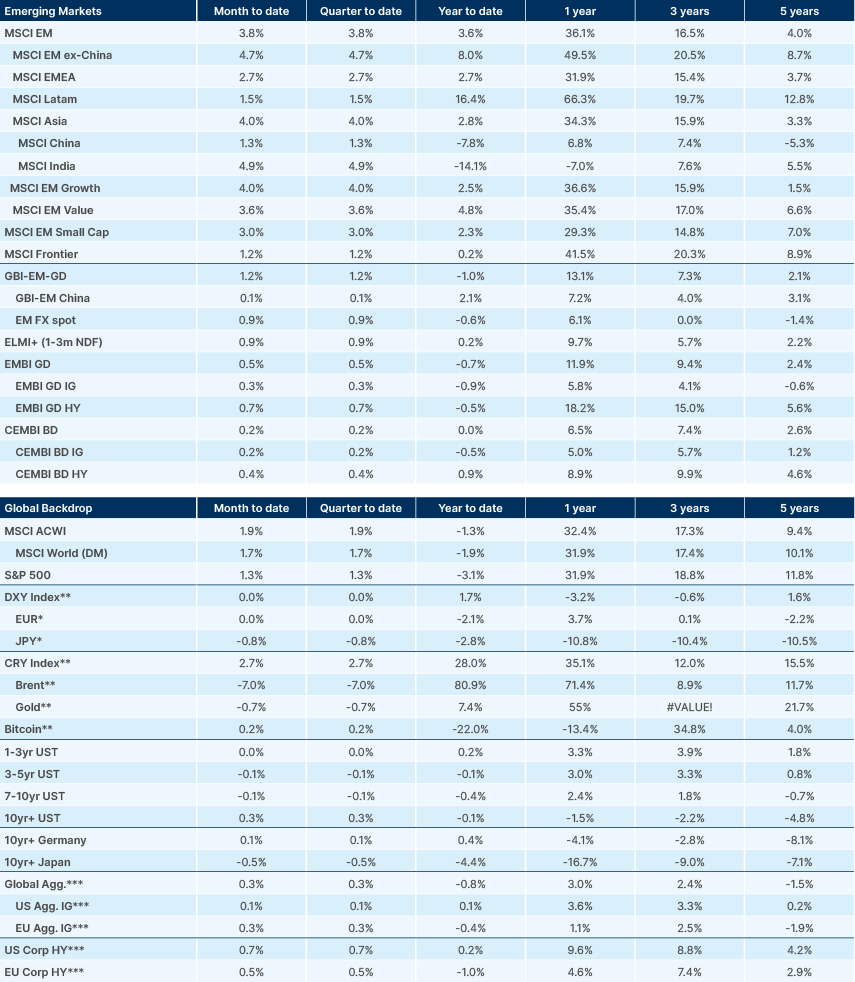

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.