Falling oil prices bring nominal rates lower and real rates higher

- Oil prices are bringing inflation expectations down with them.

- US growth has continued to come in stronger than expected.

- Volatility in semiconductor stocks now at dramatic levels.

- Korean chipmakers announced enormous capex plans.

- Vietnam outlined an expansionary fiscal framework for 2026–2030.

- S&P reaffirmed Brazil at ‘BB’ with a stable outlook.

- Chile’s Senate gave initial approval to President Kast's economic omnibus bill.

- ECB June Convergence Report found Hungary met none of its euro adoption criteria.

- Aramco expected to cut its Arab Light premium for Asian customers for the third consecutive month.

- IEA reported UAE oil exports recovered to roughly 85% of pre-Iran war levels at 4.3mn bpd in early June.

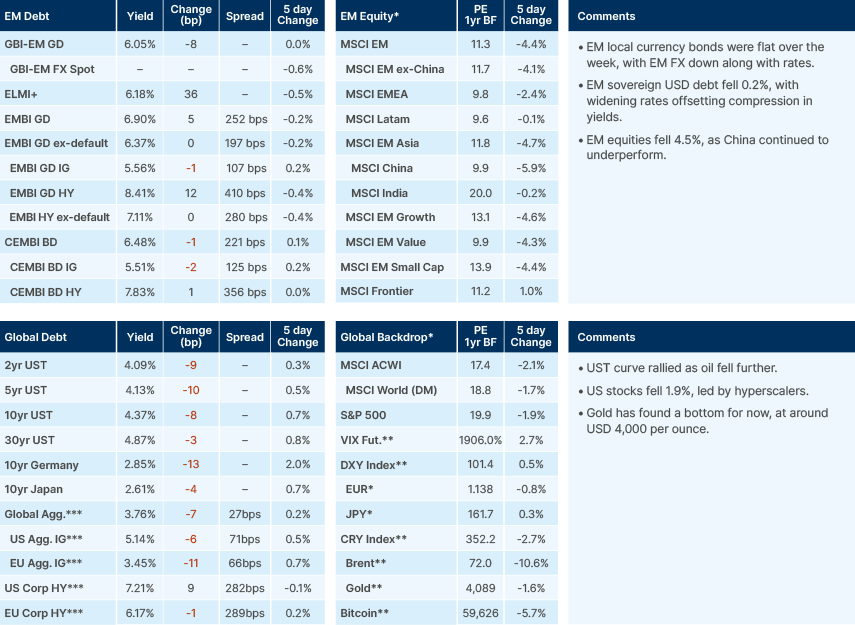

Last week performance and comments

Global Macro

Another round of US/Iran hostilities over the weekend again underlined the fragility of the current ceasefire. Even so, oil outflows have picked up meaningfully and prices have fallen in tandem, all the way down to around USD 70 a barrel last week. With the global market still short several million barrels a day, that is a remarkable move, and it reflects ongoing demand destruction, sustained inventory releases, and the unwind of speculative long positions. Whether oil can keep falling from here is debatable, but the decline has already pulled inflation expectations sharply lower. One-year USD inflation swaps have dropped from a peak of around 3.5% to 2.2% today, and one-year breakeven inflation rates on US Treasuries, which capture both inflation expectations and the demand for inflation protection, have collapsed from over 5% at the peak back to 1.6%.

Collapsing oil prices and inflation expectations suggest we have probably passed the peak in US headline consumer price index (CPI) inflation. Most banks, however, still expect core personal consumption expenditures (PCE) to stay elevated for the rest of the year, partly on pass-through from the energy shock and partly on other supply-driven factors, such as semiconductor-led consumer-electronics inflation. But the main reason for stickier inflation expectations is that the cyclical growth signals are turning up. Business sentiment is improving, with manufacturing purchasing manager indices (PMIs) the strongest in around three years. Moreover, hiring appears to be picking up against a labour pool that is no longer growing, given the Trump administration's immigration policies. If that trend continues, the labour market should tighten, which could stabilise and then lift wage inflation that is currently falling in real terms. The consumer side is being reinforced by fiscal policy. The OBBBA1 tax changes have boosted refunds, and Bank of America data show customer deposits rising faster between January and May 2026 than a year earlier. Because lower-income households have the highest propensity to spend a tax windfall, this points to a broadening of consumption rather than a narrow, top-end recovery, which adds to the cyclical upturn the activity data are already signalling.

The divergence between CPI disinflation and sticky PCE expectations sits at the heart of the hawkish shift new US Federal Reserve (Fed) Chair Kevin Warsh delivered at his inaugural Federal Open Market Committee (FOMC) meeting. Several sell-side banks have raised their end-year Fed Funds forecasts over the past month, with Bank of America the most hawkish, forecasting three hikes. The important second-order effect is that the Fed's hawkish messaging is now anchoring nominal rates, so falling CPI inflation now translates directly into higher real rates, tightening financial conditions and doing part of the Fed's job for it. Headline CPI is now running above the Fed Funds rate, so spot real rates are negative. However, it is realised inflation a year out that determines the real rate a borrower pays ex-post. On that measure, the move is already meaningful, with the 1y1y real rate up from around 0.8% in January to 1.5% today.

That same rise in real yields is reshaping the Dollar and gold. The Dollar has caught a bid on the combination of a hawkish Warsh and higher real yields, and the question now is whether it can test the 103 to 105 range on the index. The mirror image is gold, which is trying to rebound after testing USD 4,000 per ounce. The broader read is a partial reversal of 2025's de-dollarisation or 'debasement' trade. When real yields rise and the dollar firms, the opportunity cost of holding a non-yielding reserve asset climb, and capital rotates back toward dollar assets. Re-dollarisation and gold weakness are, for now, two sides of the same move.

Semiconductors had a volatile week, particularly in the memory space, underlining how extended the rally has become. Micron reported bumper earnings, comfortably beating consensus, and rose as much as 20% having drawn down around 16% from intraweek highs ahead of the print. It also announced long-term agreements covering roughly 20% of its DRAM[2] volume and a third of its NAND[3] volume through 2030, with a meaningful portion at fixed prices near current, very high levels. That is unambiguously good news for forward visibility, yet the stock still closed the week lower than it began. The Korean memory names saw similar volatility, amplified by very high levels of leveraged trading in the Korean retail system, though some of the pressure was month- and quarter-end rebalancing after the extraordinary runs in SK Hynix and Samsung.

That backdrop frames the most significant development of the week. On Monday, alongside President Lee Jae Myung, Samsung and SK Hynix unveiled a combined KRW 800trn investment, or roughly USD 518bn, to build four new memory fabs, two each, in the country's southwestern region around Gwangju. A separate KRW 550trn commitment from SK, GS Group and Naver will fund AI data centres, scaling national AI data centre capacity toward 18.4 gigawatts (GW) by 2035, and SK Group's total pledge runs to KRW 1,100trn. Taken together, the Samsung and SK decade-long programmes are reported to reach as much as KRW 2,000trn, around USD 1.3trn, a figure that dwarfs the US CHIPS Act[4] many times over and amounts to the largest semiconductor investment commitment in history. The fact that the firms closest to AI memory demand are committing unprecedented capital to meet it is difficult to reconcile with any view that the AI-capex cycle is about to roll over.

Emerging Markets

Asia

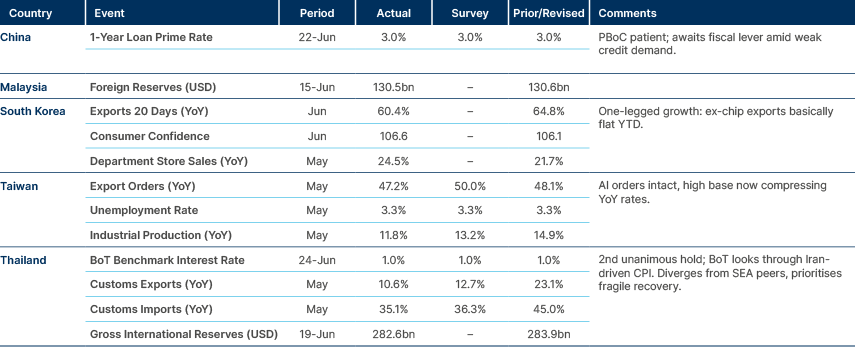

Korean exports remain strong, also reflected in record US trade deficit.

China: The National Development and Reform Commission and other agencies will impose binding targets dictating what share of both electricity and non-electric energy (heating, green fuels) must come from renewables, marking a pivot from building clean generation to forcing its consumption. Provinces and companies face quarterly monitoring and annual evaluations, and those that fall short must buy green electricity certificates, which should lift demand and revenue for the wind and solar operators that generate those credits. The specifics on industries and target levels remain undefined, but the inclusion of non-electric energy targets signals support for green hydrogen, flagged as a priority in China's five-year plan to 2030.

India: Amazon announced an additional USD 13bn to expand and support AI and cloud infrastructure in Mumbai and Hyderabad. It will launch more than 20 new fulfilment centres and over 100 new delivery stations across India this year. Cumulative investment in India from 2010 to 2030 now stands at more than USD 88bn.

Indonesia: Officials are reportedly weighing a further budget cut of over USD 2bn alongside reductions to the free meal programme's kitchens and beneficiaries, Reuters reported. The National Nutrition Agency is targeting a reduction of at least 15% from this year's IDR 268trn budget, and one source put the cut as high as IDR 50trn. The Finance Ministry said it was awaiting a budget sharpening plan from the agency.

MSCI postponed its decision on Indonesia's potential downgrade to frontier market (FM) status until November, giving authorities more time on capital market reforms. The original January warning targeted share ownership opacity that limits free float. The IDX Composite is down 29% year to date, the worst EM performer globally, and a downgrade would trigger automatic selling by EM-mandate funds.

The Finance Ministry confirmed it will not investigate the source of funds invested in Patriot Bonds, taking the explicit view that state development benefits outweigh money laundering concerns. Investors and their companies remain prosecutable but the bond funds are protected from confiscation. Issuance is modest so far at IDR 50trn plus an additional IDR 12.6trn tranche. The transparency overhang reinforces offshore portfolio caution alongside the MSCI free float concerns.

South Korea: South Korea's AI infrastructure buildout dominated the week. GS Group plans two 1.2GW AI mega-data centres in Dangjin and Donghae by 2030, co-located with existing 2.4GW LNG and 1.19GW coal plants under a local production, local consumption model. These would be Korea's first GW-scale AI facilities, sitting alongside SK's five sites, NHN's Pohang project and Samsung SDS's Haenam plant. The execution wildcard is the climate ministry's preference for direct renewable procurement for AI centres, though we expect government flexibility given AI's centrality to growth. The National Growth Fund separately approved KRW 370bn across three projects: a 72MW Yeongyang wind farm at KRW 270bn supplying a Naver data centre, KRW 80bn for LS Cable submarine capacity, and KRW 20bn for Simtek substrate. Cumulative NGF support is now KRW 13.6trn across 19 projects.

SK Hynix moved ahead with a NASDAQ American Depositary Receipt (ADR) listing targeted for 10 July, with up to 17.79 million new shares (around 2.5% of outstanding) potentially raising around KRW 45.45trn. Proceeds will fund the Yongin Phase 1 fab and Cheongju advanced packaging. The government is also reportedly considering using excess tax revenue from the chip supercycle (KRW 40trn plus this year, around KRW 100trn expected annually for two to three years) to fund the USD 350bn US investment commitment rather than drawing down FX reserves. With KRW/USD persistently above 1,500 and intervention room limited, that shift would be a clear positive for the currency.

The Bank of Korea's June Financial Stability Report assessed the system as broadly stable. The vulnerability index rose to 46.0 in Q1 against a long-term average of 45.7, while the stress index fell to 17.2 in May, below the 24 crisis level but above the 12 warning threshold. Flagged risks include renewed Seoul apartment price rises, expanded leveraged investment, and vulnerable-sector defaults as longer rates rise.

Vietnam: Vietnam outlined a more expansionary fiscal framework for 2026-2030 under Decision No. 1119, aligned with an average GDP growth target of at least 10% per year. Total budget mobilisation is to rise by 1-2 percentage points to around 18% of GDP, with the domestic share of revenue lifted to 87-88% from 86-87%. The fiscal deficit ceiling will widen to around 5% of GDP by 2030 from the previous 3%, and the public debt ceiling rises to 50% from 45%. Development investment is targeted at roughly 40% of spending and recurrent expenditure at 51-52%.

The package combines the expansionary stance with structural reforms spanning tax modernisation, base broadening, tighter state-owned enterprise oversight, and transfer pricing and trade fraud enforcement. Macro-financial supports include a targeted sovereign rating upgrade and the development of international financial centres and free trade zones. The 10% growth target is aspirational, but the structural reform agenda is the more important takeaway for credit and foreign direct investment sentiment.

Latin America

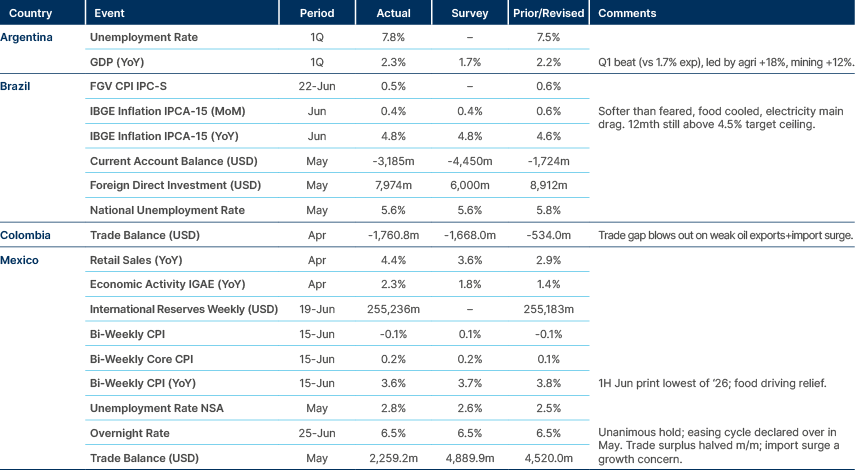

Brazilian & Mexican inflation softer than expected. Colombian deficit widens.

Argentina: The Lower House of Congress passed the 'Super RIGI' investment incentive regime for new economic activities, covering projects of at least USD 1bn with 20% disbursed in the first two years. If approved by the Senate, the bill will include a five-year enrolment period from the law's approval, 30 years of stability with international arbitration, and a 15% income tax rate, down from 25% under the original RIGI. It bars participating districts from creating local taxes and caps provincial gross income tax at 0.5%. Other benefits include unlimited loss carry-forward, a 3.5% tax on dividends and profits, trade duty exemptions, 10% employer contributions, investment incentives, and local supplier requirements.

Brazil: S&P reaffirmed Brazil at 'BB' with a stable outlook. The rating reflects a strong external position, flexible FX, the inflation targeting framework, an independent central bank, and domestically funded debt. Fiscal remains the binding weakness, with the overall deficit expected to stay near 7% of GDP and net debt rising to 74% by 2029 from 60.4% in 2025. S&P forecasts GDP at 1.8% in 2026 versus 2.3% in 2025 and sees the Selic at 10.0% by end-2028 with policy restrictive through 2029. President Lula remains the frontrunner for re-election against Flavio Bolsonaro, with a centrist congressional majority expected to limit the appetite for fiscal consolidation.

The central bank (BCB) raised its 2026 GDP forecast to 2.0% from 1.6% on stronger Q1 growth, a better agriculture and extractives outlook, and fiscal and credit stimulus. The 2026 inflation forecast was hiked to 5.2% from 3.9%, with the probability of breaching the 4.5% upper limit rising to 79% from 30%. Inflation should remain above the limit through end-2026, triggering a formal letter to the Finance Ministry, before easing to 3.7% by end-2027 and 3.1% by end-2028. The combined upgrade to growth and inflation forecasts validates Copom's hawkish stance and defers the realistic terminal Selic timing.

Chile: The Senate floor gave initial approval to President Jose Antonio Kast's economic omnibus bill, with 26 in favour, 23 against and one abstention. The legislation would cut the corporate tax rate to 23% from 27%, implement employment subsidies, streamline the investment permitting process and eliminate property levies for senior citizens. Lawmakers still need to vote on each item, a process likely to change the contents. For example, the bill would provide 25-year tax rate guarantees for large investment projects, but some lawmakers are pressing to reduce that timeframe. The government has signalled it is open to negotiating parts of the proposal.

Colombia: The National Election Council (CNE) certified Abelardo de la Espriella's runoff win, with the final tally at 12,960,166 votes (49.66%) against Ivan Cepeda's 12,708,312 (48.70%). The final count moved 400 votes from Cepeda and added 624 for de la Espriella, leaving a margin too wide to challenge credibly. President Gustavo Petro announced the transition phase on Tuesday and Cepeda conceded Wednesday. The COP touched 3,452 per USD intraday before easing to 3,428 as the concession came through.

The rifle vote issue, which describes coerced voting in zones under armed-group influence where Cepeda won several frontier regions outright, is likely to persist as a Cepeda-camp narrative into 2030. An ICP/Fundacion Colombia 2050 study flagged unusual turnout at 504 polling stations in armed-group areas.

Peru: Keiko Fujimori widened her lead over Roberto Sanchez to 43,386 votes with 99.8% of tally sheets counted, taking 50.1% of valid national votes against 49.9% for the Together for Peru candidate. Only 131 sheets remain, making the trend effectively irreversible barring judicial challenges. Fujimori dominated the overseas vote at 63.2%, while Sanchez maintains a very narrow lead in the domestic-only count. The National Jury of Elections will formally proclaim results in the first half of July.

Sanchez refused to recognise a potential Fujimori victory and alleged fraud without evidence, while calling for peaceful weekend protests. A narrow win, deep regional divisions and a pre-emptively rejecting opposition create a difficult starting point for the transition.

Central and Eastern Europe

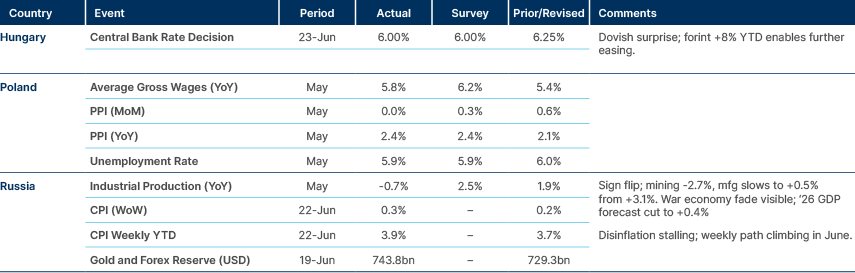

Polish wages rose less than expected. Hungary cut as expected.

Czech Republic: The government approved a CZK 100bn AI gigafactory at an existing Ceske Radiokomunikace site. CRA contributes CZK 70bn, the government CZK 15bn, and the EU another CZK 15bn, with formal European Commission support expected in July. The facility will serve government, academia and start-ups, with the ambition of developing an independent Czech AI model with supervised access to sensitive state data. Cost is the main execution risk given the surge in memory chip prices.

Hungary: The European Central Bank (ECB) June Convergence Report found Hungary meets none of the euro adoption criteria, against the Tisza government's stated 2030 target. May HICP inflation was 3.3% yoy versus the 2.7% benchmark, with further pressure expected from energy and Middle East spillovers. Long-term yields averaged 6.7% against a 5.1% benchmark but have compressed since April's election. The Forint has appreciated 11.4% over the two-year window but remains outside ERM II.

Fiscal is the binding constraint. The excessive deficit procedure is in abeyance, but the 2026 deviation from the expenditure path could trigger a step-up, and public debt is projected to keep rising. Institutional issues around central bank independence and the monetary financing prohibition also remain outstanding. The 2030 timeline looks optimistic, in our view.

Kazakhstan: Prime Minister Oljas Bektenov met Chinese Premier Li Qiang in Beijing, with the Belt and Road Initiative (BRI) the headline topic. The sides flagged expanded trade and investment in agriculture and transport, and Li urged closer alignment of development strategies. Kazakhstan positioned itself as a regional connectivity bridge while emphasising openness to all partners, a calibrated signal that Astana is not picking sides. The Middle Corridor sits within the BRI, but Kazakhstan continues to develop it with European partners in parallel.

Poland: Prime Minister Donald Tusk announced that TEEMA, which groups around half of Taiwan's electronics industry including Foxconn, will invest billions of dollars in a tech park in Miekinia, southwestern Poland. The park will focus on AI server production and electric vehicle-related systems. The plot is ready and construction can begin quickly, with the site previously earmarked for Intel before that project was shelved. Individual companies are expected to announce specific projects in due course.

The deal secures meaningful European AI hardware capacity for Poland and reinforces the broader diversification of Taiwanese manufacturing away from mainland China, a theme that has consistently benefited CEE since 2022.

Ukraine: Hungary blocked an EU-27 joint letter on Ukraine's accession process. Prime Minister Peter Magyar opposed opening the remaining five negotiating clusters at last week's summit and stripped an acceleration clause from the European Council's final declaration. Hungary had lifted its veto on the first cluster earlier this month, but is now signalling sustained resistance, with President of Poland Karol Nawrocki echoing concerns on agricultural competition. Opening all six clusters this year now looks unlikely.

The World Bank approved a USD 3.4bn package, a USD 2.4bn grant plus a USD 1.0bn loan, backed by USD 540m from Japan and USD 500m from the UK. Kyiv also expects the first USD 3.2bn tranche of the EU's EUR 90bn package this week. Financing is intact even as the political track slows.

Central Asia, Middle East, and Africa

Egypt: China's SANY Group signed a memorandum of understanding to build Egypt's first wind turbine factory and a 2GW Gulf of Suez wind farm. The plant has 2GW of annual production capacity and should be completed within two years of a final agreement, with investment reportedly around USD 300m. The deal aligns with Egypt's 45% renewables target within two years and adds manufacturing localisation to what has been a generation-only renewables build.

Gabon: Moody's revised Gabon's outlook to negative from stable on 24 June, affirming 'Caa2' (non-investment grade). The action reflects financing requirements of 15-20% of GDP annually over the next three years, weak public financial management and difficult funding conditions. The fiscal deficit is seen narrowing to 6.5% in 2026 and 4.5% in 2027 from an estimated 8.5% in 2025, with public debt rising toward 88% of GDP by 2027.

The tail risk is the comprehensive debt audit, which could reveal undisclosed liabilities and trigger further debt exchanges. Moody's was explicit that distressed exchanges would be treated as defaults. In May, Fitch affirmed 'CCC-' foreign and 'CC' local.

Nigeria: Dangote Petroleum Refinery and Petrochemicals plans to raise as much as USD 2bn in Africa's biggest IPO. The offering has sparked an investor frenzy across Nigeria.

Oman: Oman opened temporary shipping corridors near the Strait of Hormuz through its territorial waters off the Musandam Peninsula, and explicitly waived transit tolls. The Strait carries 20-21% of global petroleum liquids daily, and Oman's sovereignty over the standard outbound lane and median buffer gives it real leverage. Standard lanes remain disrupted by lingering mines, and the temporary corridors hug Musandam in deeper waters normally restricted during peacetime.

Under international law, fees are not permitted on innocent strait passage, and Oman's explicit reminder positions the country as a custodian of the maritime commons. The intervention reflects Oman's longstanding neutrality and mediation doctrine and likely sets up a more permanent role if regional tensions resurface.

Saudi Arabia: Aramco is expected to cut its Arab Light premium for Asian customers for the third consecutive month, with analysts pointing to a USD 6 to 8 per barrel cut that brings the differential to USD 1.5 to 3.0 above the Oman/Dubai average. The pressure reflects weaker Chinese refinery demand, cheaper US and West African barrels, the post-US-Iran spot drop, and expectations of higher Iranian exports under the temporary sanctions reprieve. Aramco also resumed loadings at Ras Tanura after a nearly four-month suspension, with Yanbu having reached 5 million barrels per day (mbpd) export capacity in May. A third consecutive cut plus Ras Tanura back online suggests Saudi Arabia is shifting from supply discipline to market share defence as Iran returns.

UAE: The International Energy Agency (IEA) reports UAE oil exports recovered to roughly 85% of pre-Iran war levels at 4.3mbpd in early June, from 1.9mbpd in March. The recovery was driven by the Habshan-Fujairah pipeline, which bypasses Hormuz entirely, alongside Fujairah storage that maintained Asian deliveries through the worst of the disruption.

The Habshan-Fujairah pipeline currently carries up to 1.8mbpd. The accelerated West-East expansion, ordered in May, doubles this to 3.6mbpd by 2027. ADNOC is pushing total capacity to 5mbpd by 2027 against an OPEC+ quota of 3.41mbpd, the UAE having left OPEC+ on 1 May to remove that constraint. The UAE looks like the most operationally resilient Middle East oil exporter and a structural EM crude supply growth source into 2027 and 2028.

Developed Markets

Core PCE in line with expectations. US GDP revised higher.

Japan: Bank of Japan (BOJ) board member Naoki Tamura stated that underlying CPI inflation has already reached a level generally consistent with its price stability target of 2%. He flagged a high risk that CPI inflation moves above the BOJ's 2.0% target for three reasons. First, firms' and households' medium- to long-term expectations have reached around 2% and continue to rise, unlike in 2022, when expectations were still shaped by deflationary behaviour. Second, price setting has become more active, with higher pass-through from import prices, logistics and personnel costs, and price hikes now seen beyond large firms to regional consumer-facing firms. Third, demand continues to exceed supply, as the output gap remains positive and labour shortages intensify.

Tamura said the BOJ should move the policy rate toward neutral before it falls behind the curve and is forced into disruptive tightening. In February, he saw neutral at around 1%. He now sees it as most likely around 2%. Tamura recommends a baseline path of 25 basis point hikes every few months toward neutral, or faster if upside risks to prices become more likely to materialise. This raises the likelihood that he votes for the next hike at the September Monetary Policy Meeting (MPM).

Tamura is the hawkish tail of the BOJ Board, but has recently pulled the rest of the Board closer to his views. His dissenting vote in favour of a hike at the April MPM, together with Hajime Takata and Junko Nakagawa, helped to bring about the June rate hike. His latest position on upside risks to underlying inflation and the need to move faster toward a higher neutral rate may pressure the BOJ to hike by October, currently 60% priced, especially if other hawkish-leaning members move toward his inflation expectations and neutral-rate framing.

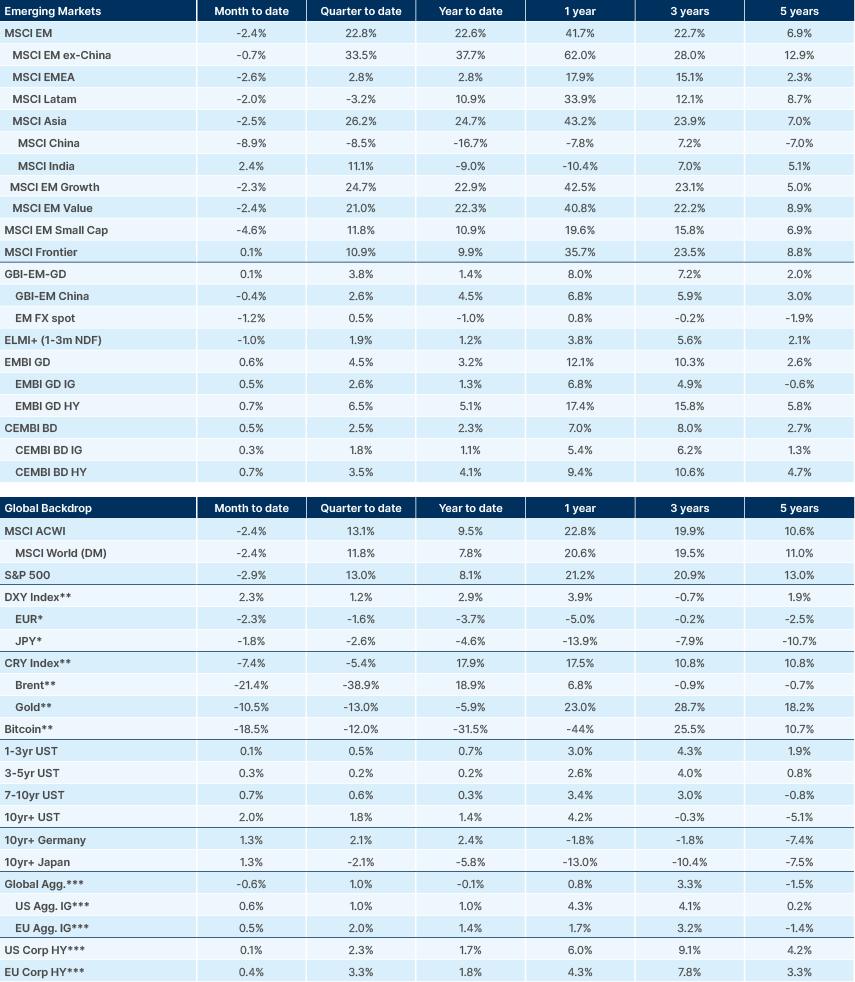

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. One Big Beautiful Bill Act.

2. Dynamic Random-Access Memory.

3. Not And memory.

4. Creating Helpful Incentives to Produce Semiconductors Act (2022).