- Iran sent a new proposal to the US over the weekend, as backchannel negotiations continue.

- The epic rally in semiconductor stocks continued but may now be stretched.

- US inflation expectations, reflected in swaps markets, remain contained.

- China’s AI start-up DeepSeek released its V4 models.

- Fitch downgraded Philippines credit outlook to negative.

- Shin Hyun-song confirmed as BOK Governor.

- Brazil’s 2026 inflation expectations continued to rise.

- Economic sentiment in Hungary highest since January 2024.

- S&P affirmed Türkiye’s credit rating at ‘BB-’ with a stable outlook.

Last week performance and comments

Global Macro

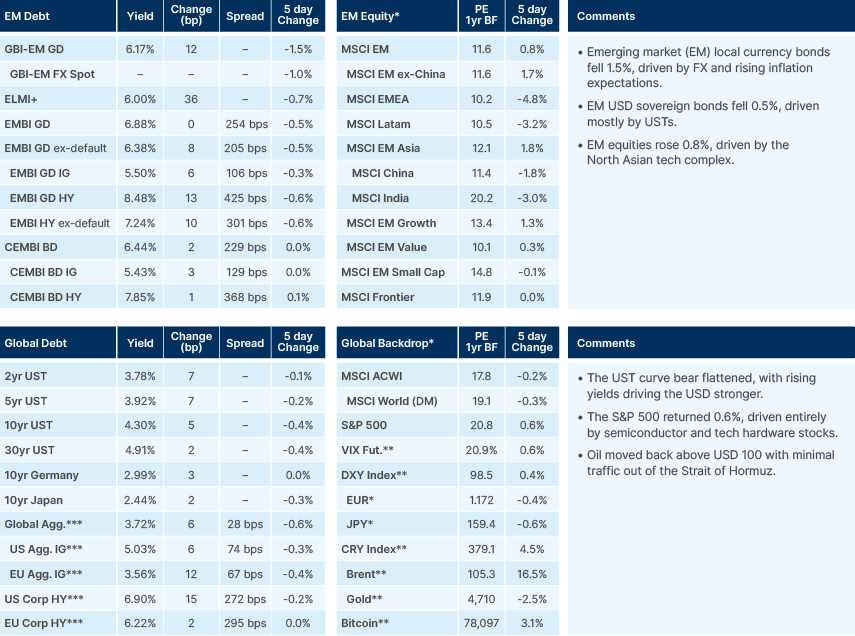

Late last week, hopes for a swift end to the US-Iran conflict were dampened further after US President Donald Trump cancelled plans for US delegates to travel to Islamabad to resume talks with Iran. However, markets were soothed again this morning by reports Iran had sent an updated proposal to reopen the Strait of Hormuz and end the US blockade. The key point of the proposal is that nuclear talks would be the second stage, after waterways have been opened. The US is yet to respond to the conditions of the proposal, but the fact that indirect negotiations are ongoing remains all the encouragement that capital markets need, for now.

Semiconductor stocks continued their parabolic move higher this morning, with SK Hynix and TSMC both up more than 5% already today. SK Hynix is now up 92% YTD, while TSMC is up 43% and remains supported by last week’s lifting of single stock investment caps in Taiwan. Perceptions around AI capex overspend have changed significantly in recent months after AI frontier labs continue to produce models that far exceed expectations.

The pricing out of AI ‘bubble’ risk has supported a broad reassessment of semiconductor stock valuations, as the perception around the sustainability of soaring earnings is changing. Memory chip manufacturers, such as SK Hynix, are growing earnings so rapidly that valuations have compressed meaningfully YTD. However, outside of memory, valuations have generally grown richer: TSMC’s forward price-to-earnings valuation has risen from 19x at the beginning of the year to around 23x, close to its October 2025 peak. Nvidia has seen a similar move since March lows, rising from 19x to 24x.

While we think this reassessment is probably correct, the move in tech hardware stocks is now very extended, with semiconductor stocks at overbought levels. The earnings visibility remains very clear on a forward-looking basis. However, we would be cautious in chasing the rally here, from a technical standpoint and because markets continue to behave as though the Hormuz disruption will be short-lived, in sharp contrast to physical energy markets. Technology stocks are less inflation sensitive, but a repricing of the discount rate mechanically lowers the valuations of high growth companies.

The US 2y2y forward inflation swap currently trades at 2.47%, up just 12 basis points (bps) from its 27 February close. For comparison, the same measure added 75bps during the equivalent period at the start of the Ukraine war in 2022. The 1y breakeven at 3.17% is 65bps lower than on the eve of the conflict. Physical markets tell a different story: the Shanghai Freight Rate is up 50% and jet fuel into Singapore has doubled. The Dallas Federal Reserve's recent Energy Survey adds to the disconnect: 40% of respondents expect the Hormuz disruption to persist until at least August, while 48% say it is very likely the Strait will be disrupted again within the next five years. If the physical market is right and the swaps market is wrong, the repricing in short-term inflation could be sharp.

The world’s five major central banks, the Federal Reserve (Fed), Bank of Japan, European Central Bank, People’s Bank of China and the Bank of England all meet this week, with all five expected to keep interest rates on hold. The substance will be in the communication, specifically how each central bank's reaction function is being shaped by the conflict and the associated stagflation risk. The tension between looking through a supply-driven energy spike and responding to rising inflation expectations is now the defining policy question across developed markets (DM). US Senator Thom Tillis dropped his hold on Kevin Warsh's nomination for Fed Chair over the weekend, arguing that the Department of Justice decision to end a criminal probe involving Jerome Powell removed a threat to central bank independence. Tillis said he had been assured the case was "completely and fully settled", although the Fed Inspector General continues a separate review of renovation cost overruns. This opens the door to a quick Senate confirmation vote on 29 April, ahead of Powell's term ending on 15 May. Powell's Governor seat runs to 2028.

The Supreme Court's International Emergency Economic Powers Act (IEEPA) ruling has taken a toll on the administration’s tariff revenue, but the damage so far has been limited. The revenue hit from the ruling totals approximately USD 60bn annualised at the current run rate, according to Standard Chartered, and could decline further in the coming months if the temporary remedies expire without replacement.

Emerging Markets

Asia

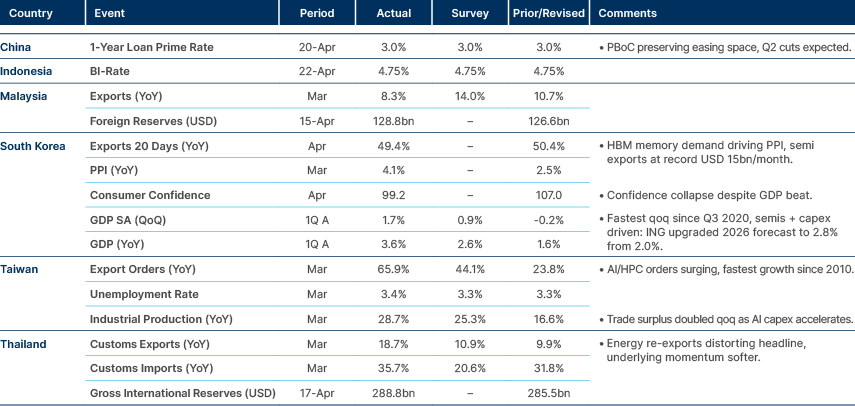

BI kept policy rates unchanged. Korean exports still very elevated.

China: Industrial profits rose 15.8% yoy in March, accelerating from 15.2% in the first two months of the year, defying expectations that the surge in global oil prices would weigh more heavily on manufacturers’ margins. The rebound in producer prices, turning positive during the month after three and a half years of deflation, appears to have offset the war-related cost pressures, with earnings in upstream sectors such as mining particularly strong. This suggests the first-round impact of the energy shock on Chinese industry is benign, at least in the data through March. The question is whether downstream margins compress in the April and May prints as input costs feed through more fully.

DeepSeek released its V4 models with a 1 million token context length and 1.6 trillion parameters, supporting longer-horizon agentic tasks. The inference efficiency improvements including reduced memory requirements and less reliance on Nvidia chips are likely supportive of Huawei and the broader domestic semiconductor ecosystem. The trend of bifurcation between US and Chinese AI supply chains continues to develop.

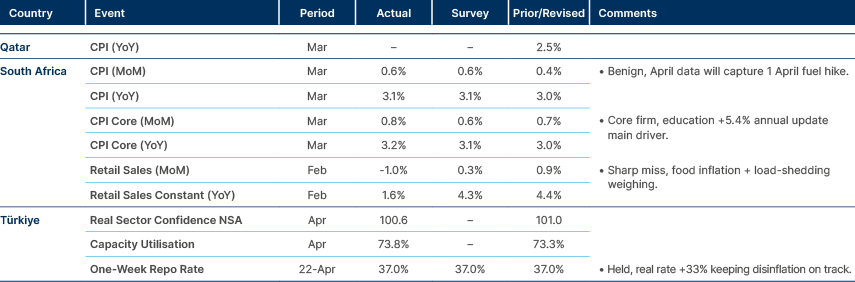

Indonesia: Bank Indonesia (BI) held its key rate at 4.75% at its 21–22 April meeting, in line with consensus. Inflation has eased back into the 2.5±1% target band, with headline consumer price index (CPI) inflation moderating to 3.48% yoy in March from 4.76%, and core CPI settling at 2.52%. But the framing of the decision was the news: BI centred its statement on Rupiah stability rather than inflation and explicitly stated it stands ready to strengthen policy if needed, a shift from neutral to slightly hawkish that caught some attention.

The IDR has weakened 0.9% since end-March, breaking through the psychologically important 17,000 level. BI maintained its 4.9–5.7% GDP forecast despite cutting its global growth assumption by 10bps to 3.0% and is leaning on triple FX intervention plus secondary-market debt purchases to manage the currency. A rate hike in May or June is possible if Rupiah pressure persists, particularly given an external backdrop of elevated energy prices and short-term dollar strength.

Malaysia: A survey of 222 manufacturers shows approximately 40% are already facing reduced production from raw material shortages tied to the Hormuz disruption, with plastics, chemicals and metals worst affected. Some firms with limited stock may halt production entirely within one to two months if supply does not improve. A prior survey had 90% of respondents expecting near-term disruption, so the actual hit is less severe than feared, but the sectoral concentration is concerning and the implications for Q2 industrial production are material.

Pakistan: Islamabad and Rawalpindi were effectively locked down for the second round of US-Iran peace talks. The Red Zone was sealed, public transport suspended, universities cancelled classes and over 10,000 policemen were deployed. C-17 cargo flights carrying US security equipment arrived on Sunday. The talks are proceeding despite renewed Hormuz tensions; the heightened security signals the meeting is on, following the first round held 11–12 April. The outcome of these negotiations is arguably the single most important near-term catalyst for energy markets and EM risk broadly.

Philippines: J.P. Morgan announced the Philippines will be added to the GBI-EM index from 29 January 2027, with a gradual phase-in to a 1.78% weight across nine eligible Peso bonds totalling approximately USD 49bn. The National Treasurer had previously estimated USD 3bn of inflows. The index revision also caps the single-country maximum at 9% from 10%. Saudi sukuk were added simultaneously at 2.52%. This is structurally positive for Philippine local rates and the Peso, and adds another layer of support to EM local currency fixed income flows into Asia.

Separately, Fitch revised the Philippines’ outlook to negative from stable on 20 April, affirming the ‘BBB’ rating. The drivers were disruptions to public investment, energy shock exposure, and erosion of the growth premium versus peers. Fitch now forecasts GDP at 4.6% in 2026, CPI inflation at 4.1% (above the 2–4% target), and the current account deficit widening to 3.8% of GDP from 3.3% on energy imports. S&P also moved the outlook to stable from positive earlier this month. The rating agency direction has clearly turned, even if an actual downgrade remains some distance away.

South Korea: Shin Hyun-song was confirmed as Bank of Korea (BOK) Governor on 20 April after a delayed second hearing — the first such delay since the confirmation system began in 2014, on opposition concerns about his daughter’s nationality and passport. In his inaugural address, Shin promised “prudent and flexible” policy, warned that higher oil simultaneously raises inflation and lowers growth, and flagged expanded non-bank monitoring, won internationalisation, offshore won settlement and central bank digital currencies (CBDC) use as strategic priorities. The tone suggests continuity with recent BOK caution rather than any sharp policy pivot.

On the energy front, the government is actively expanding Red Sea routes as an alternative crude supply channel. A Korea-owned tanker carrying 2m barrels of Saudi crude loaded at Yanbu on 17 April and is now sailing. Around five such contracts have been signed, each for approximately 2m barrels. The Houthi threat at Bab el-Mandeb remains the binding risk, but no incidents have been reported so far. What started as one-off diversions is scaling into a systematic alternative to Hormuz transit.

President Lee Jae Myung’s approval rating rose to 65.5% from 61.9% according to Realmeter, up from 53.1% at the start of the year. The increase is attributed to the government’s broad and rapid response to the energy crisis. The Democratic Party (DP) rating remains stable at 50.5% while the People Power Party sits at 31.4%. The opposition remains fragmented, and the DP is commanding heading into early-June local elections.

Latin America

Mexican inflation flat lining in April. Argentina’s surplus surged on agriculture exports.

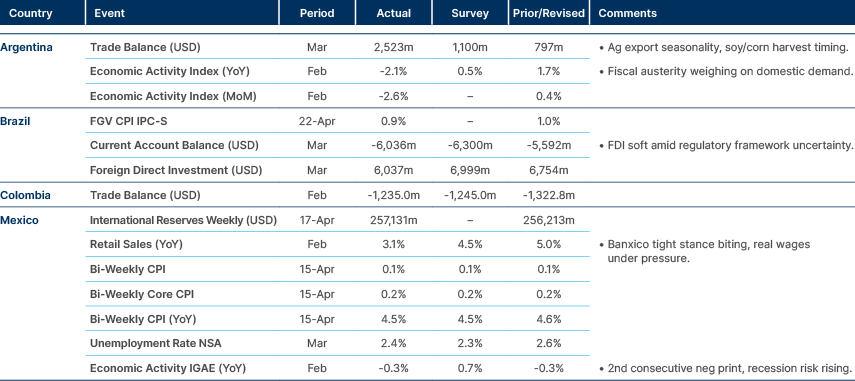

Argentina: The goods trade surplus widened to USD 2.5bn in March from USD 623m a year earlier, bringing the 12-month surplus to USD 15.8bn (2.3% of GDP). Exports surged 30.1% yoy, driven by volumes (+25.3%) on record wheat and barley harvests, plus gold and beef price effects. Industrial exports rose 23.6% year-to-date, led by gold, lithium and light commercial vehicles. Energy exports were up just 1.9% YTD, with March data not yet reflecting the oil price spike — that impact will land in the April release.

The import side tells a different story. Imports rose just 1.7% yoy in March, but are down 7.3% YTD. Capital goods, intermediate goods and parts are all declining, which is a yellow flag on domestic activity. Fuel imports fell 38.5% on import substitution. Vehicle imports jumped 28.9% as automakers shift to cheaper sourcing from Brazil, Mexico and China. Weak import demand at this real effective exchange rate level is the concern — it signals soft domestic activity even as the ARS strengthens.

Finance Minister Luis Caputo said financing needs are covered for 18 months without tapping global markets: USD 4bn from local USD bond issuance, USD 4bn from International Finance Institution (IFI)-guaranteed loans, and USD 2bn from privatisations. The logic is to wait for President Javier Milei’s 2027 re-election campaign to compress political risk before returning to international markets. The counterargument is that delaying market return also delays rating upgrades, and stacking senior debt works against sovereign risk. Either reading is defensible — the bet is on political risk being the dominant spread driver.

Brazil: The March trade surplus declined yoy as imports grew 19.9% versus exports at 9.5%, with fertiliser imports a notable drag from the Middle East shock. Foreign direct investment was USD 6.0bn in March, and the 12-month total of USD 75.7bn (3.2% of GDP) still fully covers the current account deficit. The Central Bank of Brazil sees the deficit narrowing to USD 58bn (2.2% of GDP) in 2026.

The Focus survey showed 2026 CPI inflation expectations raised to 4.80% from 4.71%, the sixth consecutive upward revision and the second week above the 4.50% upper band of the target. The 2026 Selic forecast was lifted to 13.0% from 12.5%, trimming expected total easing to 200bps from 250bps. Consensus still points to a 25bps cut at the April meeting and another in June. The 2027 Selic forecast was cut to 10.50%, and GDP edged up to 1.86%.

Flávio Bolsonaro is reportedly backing reform of mandatory expenditure as part of his platform by re-indexing health, education and social benefits to inflation rather than net current revenue and minimum wage. If implemented, this could reduce spending by approximately 2% of GDP. The proposal is constructive for fiscal sustainability and the neutral rate but requires a supermajority in both houses.

Colombia: President Gustavo Petro told Finance Minister German Ávila to raise the minimum wage if BanRep hikes again; a mid-year adjustment would be unprecedented. Petro’s framing that energy is driving inflation does not withstand scrutiny: energy subtracted 30bps from headline inflation in Q1. The March rise came from services ex-rents, consistent with prior minimum wage pressure rather than energy passthrough. Law 278 sets the annual December procedure, but does not absolutely bar additional adjustments and the Constitutional Court’s “mobile remuneration” doctrine could theoretically be used as cover. The constraint is political and reputational rather than clearly juridical.

Colombia announced a buyback of USD 5bn worth of Eurobonds, increasing the technical shortage of bonds despite the deteriorating fiscal picture. This strategy will be tested if Petro succeeds in electing his successor amid ongoing policy deterioration.

Ecuador: The International Monetary Fund (IMF) approved the fifth Extended Fund Facility review on 22 April, unlocking USD 394m and bringing cumulative disbursements to USD 3.7bn under total access of USD 5.0bn. Combined with the January USD 4.0bn voluntary issuance and the associated buyback, this signals meaningfully reopened market access. The EMBI spread compressed to 404bps on the day of the IMF statement.

Reserves stood at gross USD 10.5bn at end-March, down 8.9% mom, but up 35.6% yoy. The IMF projects reserves rising to USD 13.8bn by end-2026 and USD 17.5bn by end-2027. The open question is the composition of fiscal adjustment. The government is leaning on tax expenditure cleanup and efficiency gains rather than visible spending cuts, which lowers political cost but may limit the cash impact. If growth disappoints or markets reprice, official financing dependence rises and the political sustainability debate reopens.

Central and Eastern Europe

Solid activity data from Poland, as PPI rebounds in Czech.

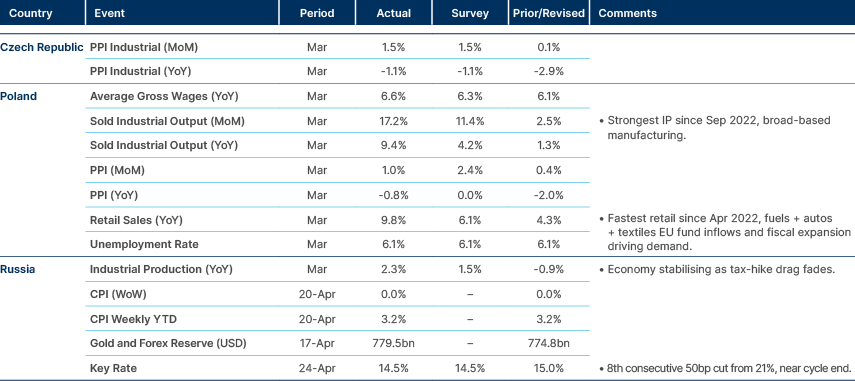

Hungary: The GKI economic sentiment rose by 3.2 to -10.7 in April, its highest level since January 2024. The improvement was driven by election expectations and the Tisza Party win, although the results were not incorporated in the survey, so further sentiment gains are likely in May. Business confidence increased by 3.4pts on improved predictability and EUR adoption hopes, while consumer confidence was up 2.5pts to a 28-month high. All four major sectors posted increases, with trade leading the improvement.

Prime Minister-elect Péter Magyar asked the outgoing Orbán government to extend the Ukraine-related state of emergency to end-May (currently expires 13 May). As many as 160 pieces of legislation depend on it and the new government needs runway to review them. Mass-immigration emergency still in place until 7 September. This is procedural rather than a political signal.

Ukraine: Repairs to the Druzhba pipeline have been completed, and Russian oil transit resumed on 22 April, according to Reuters. Ukrainian president Volodymyr Zelenskyy expects the EU's EUR 90bn loan to be unblocked, with EU foreign policy chief Kaja Kallas signalling “positive decisions”. Hungary had blocked the loan ahead of the 12 April election, with prime minister Viktor Orbán linking any unblocking to the restoration of the pipeline. The original April disbursement is now likely to be delayed until May or June. The victory of Magyar and his Tisza Party is expected to improve relations between Ukraine and Hungary, although Hungary continues to hold around USD 80m in cash and gold belonging to Oschadbank.

Separately, Zelenskyy warned the EU may "lose Ukraine like you lost Georgia" if new accession conditions emerge or deadlines slip. He rejected proposals from Germany for a lighter form of associate EU membership and from Italy for security guarantees modelled on NATO Article 5. He also pushed back against IMF and EU demands for tax increases, noting Ukraine’s parliament has already rejected a proposal to apply VAT to independent professionals. Frustration with Brussels appears to be building, even as the loan moves closer to being unlocked.

Middle East and Africa

Türkiye kept monetary policy at 37%, but effective short-term rate at 40%

Kuwait: Kuwait Petroleum Corporation declared force majeure on crude and product shipments around 17 April, citing the Hormuz blockade. Kuwait produces approximately 2.6 million barrels per day (mbdp), and exports around 1.9mbpd of crude plus 860,000 bpd of products, almost entirely through the Strait. Production cuts and refinery reductions are underway as storage fills and tanker availability in the Arabian Gulf remains constrained. Iraq and Qatar are implementing comparable cuts.

Iran’s proposed transit toll, payable in rials, alongside prohibitions on Israeli-linked vessels and flexibility for non-hostile states, is shaping which cargoes can move. US estimates suggest Gulf production fell by more than 9mbpd in April, pushing Kuwaiti output to 1990s lows. With oil accounting for roughly 90% of Kuwaiti government revenues, the FY26–27 deficit will run materially above the now-obsolete baseline of KWD 9.8bn (USD 32bn).

South Africa: Finance Minister Enoch Godongwana told Bloomberg that the fuel relief measure — a ZAR 3 per litre levy cut introduced in April at an estimated cost of ZAR 6bn per month — can be sustained for a maximum of three months, describing it as a “hard, hard deadline.” The current measure expires on 5 May, with a decision on any extension expected at the end of April. Tax increases are off the table given pre-municipal-election politics, so any extension would need to be funded through reprioritisation within the existing fiscal envelope, with health, education, policing or infrastructure taking the hit.

South Africa is a net importer of oil, but exports a larger amount of coal. Absent fiscal expansion, elevated fuel prices may drag growth even if second-round inflation effects are contained. The government openly acknowledges uncertainty on the duration of the shock.

Türkiye: S&P affirmed the country’s ‘BB-’ rating with a stable outlook, contingent on the government sticking to its 2026–2028 Medium Term Programme and global energy prices easing in the second half of the year and returning to pre-war levels by 2027–28. CPI inflation ran at 30.9% yoy in March. The 2026 average inflation forecast was revised sharply higher to 29.3% from 23.4%, on energy passthrough plus the January wage adjustment.

External vulnerability was flagged as the central concern. Non-residents have unwound USD 25-30bn in bonds, equities and carry positions since the conflict started, draining reserves materially. The Central Bank of Türkiye has responded with FX intervention, the suspension of one-week repo operations, tighter lira reserve requirements and the expanded use of swaps. Alongside this, the Ministry of Treasury has introduced a sliding scale that adjusts the special consumption tax on fuel. S&P continues to view reserve adequacy as a core weakness given the high degree of dollarisation. Growth remains resilient, with GDP expected to expand by 3.4% in 2026 (from 3.6% 2025). The fiscal deficit is projected to widen modestly to 3.5% of GDP. All three ratings agencies have now assigned a stable outlook, reducing the likelihood of near-term rating action in either direction.

Developed Markets

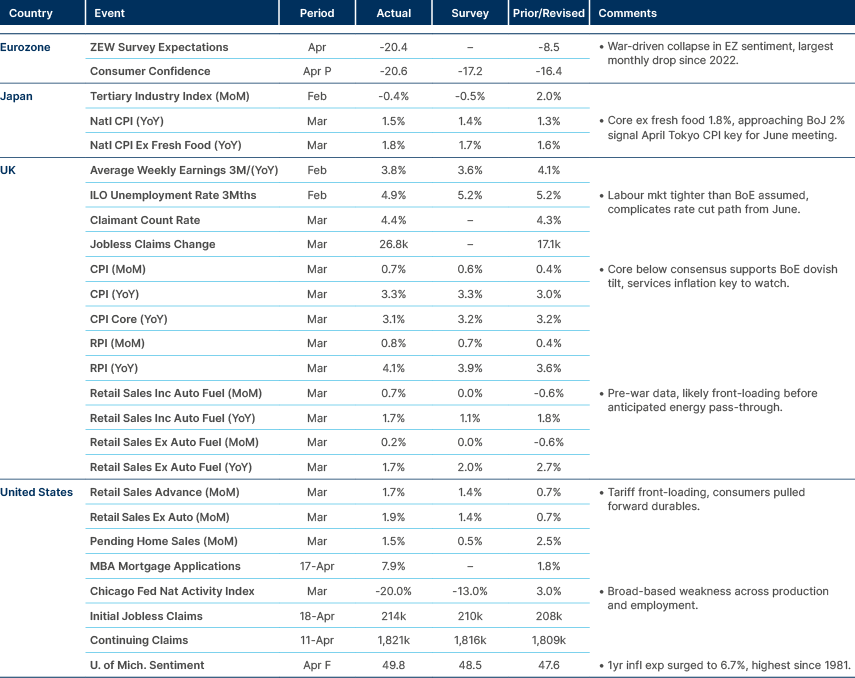

Inflation rose more than expected in Japan and broadly in line in the UK.

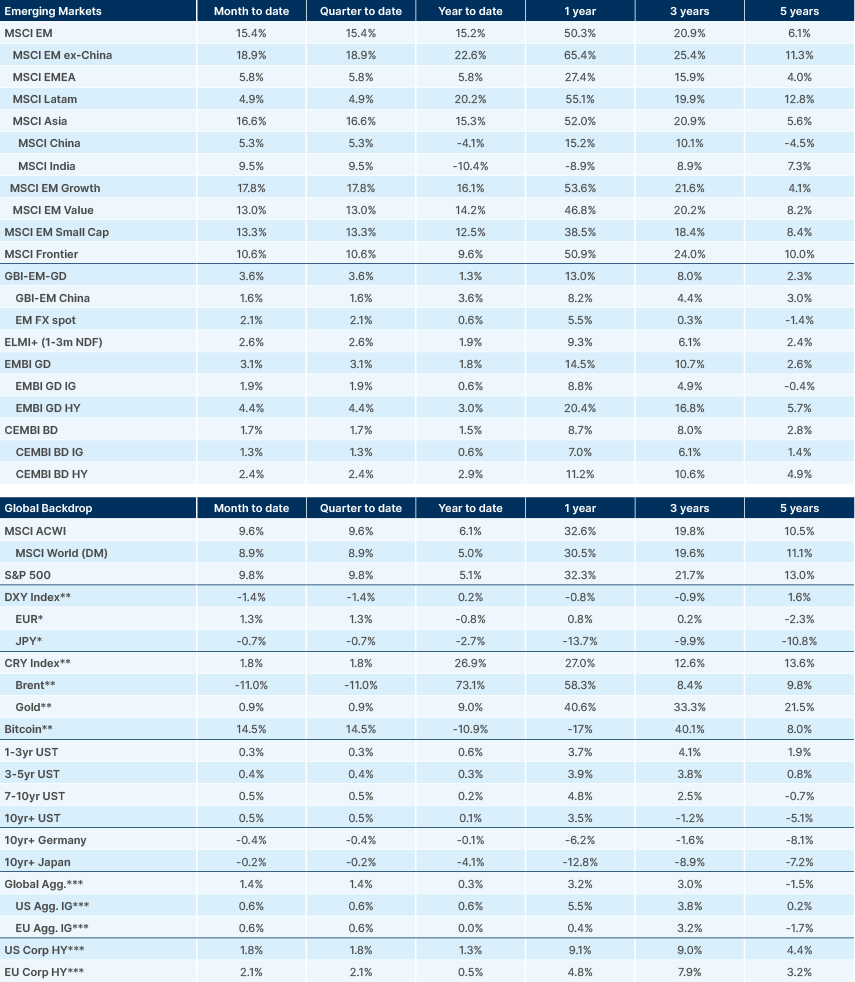

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.