- Hormuz stand-off enters its third week with Iran-US talks expected to reconvene in Islamabad.

- IMF Spring Meetings consensus: weak USD, EM-friendly commodity strength.

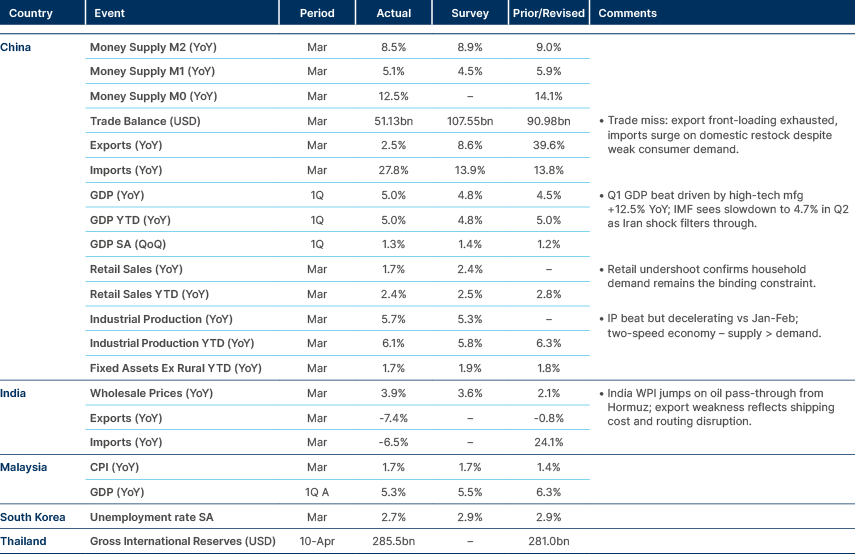

- South Korean import prices jumped 16.1% mom in March, sharpest since the Asian crisis.

- Argentina missed its IMF reserve accumulation target and needs a second waiver.

- Brazil's 2027 primary target of 0.5% has fallen to 0.1% after framework carve-outs.

- Colombia's BanRep Governor publicly accused the Finance Minister of vetoing the board.

- Peru's runoff race flipped to a possible Fujimori-Sánchez contest.

- Fitch cut Türkiye's outlook from positive to stable after USD 50bn in FX interventions.

- Saudi crude exports to China set to halve in May.

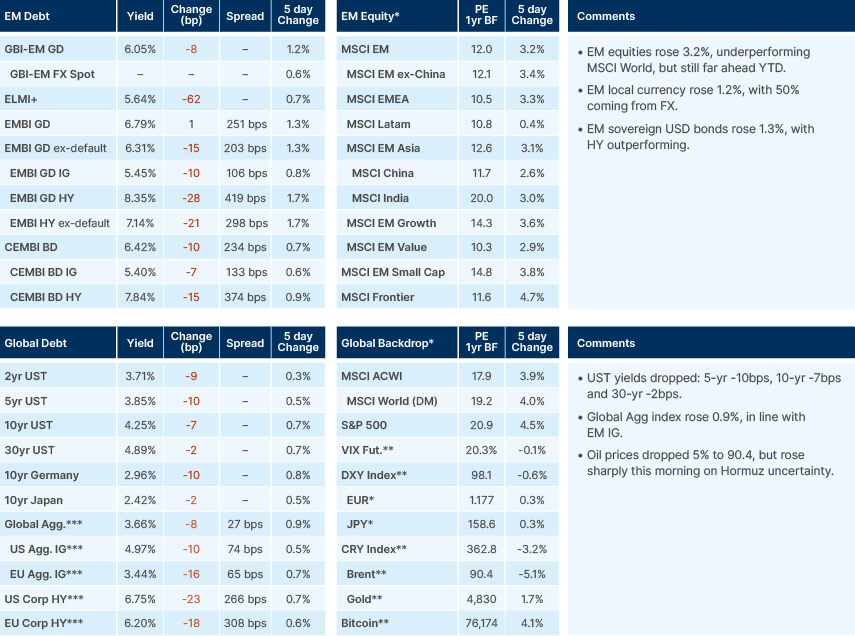

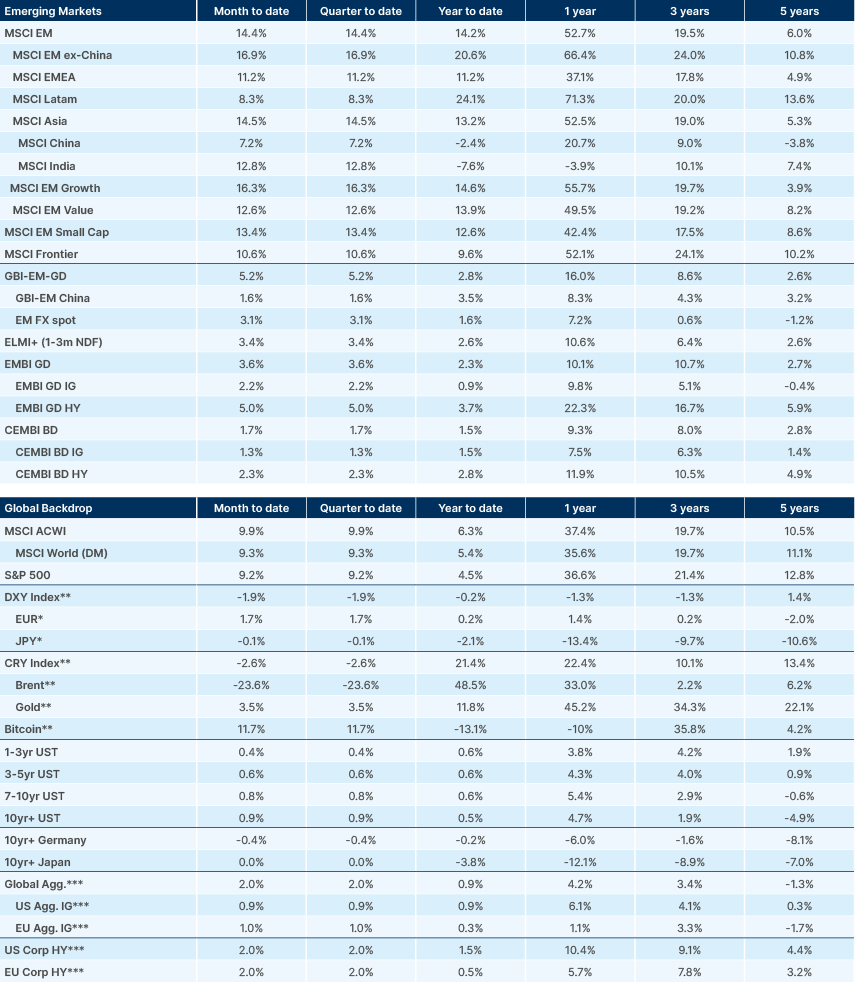

Last week performance and comments

Global Macro

The deadline for the 14-day US/Iran ceasefire looms tomorrow amid a murky picture for the Strait. Last Friday, Iran said ships could pass through the Strait, before stopping traffic less than 24-hours later. Another meeting in Islamabad, Pakistan, is scheduled for Tuesday with Vice President JD Vance and envoys Steve Witkoff and Jared Kushner flying out tonight. As Bloomberg’s Javier Blas points out, we have been in a two-week no-war, no-peace, no-oil stand-off. The fact that some ships have been allowed to pass the Strait and the unclear picture ahead suggests we may have a period when the Strait is both open and closed at the same time, like the famous thought experiment from Austrian physicist Erwin Schrödinger.

Against this backdrop, the Spring meetings of the International Monetary Fund (IMF) got underway in Washington DC. The contrast in mood between meeting attendees was notable. Country officials, economists, as well as commodities and geopolitical analysts, were downbeat, concerned with the supply chain disruption and the clear shortages of physical energy that contrasts with the more benign pricing on futures. Javier Blas highlighted over the weekend that physical crude trades at a staggering range of “USD 78 per barrel in Kansas to USD 286 in Sri Lanka”. Saudi Arabia will sell its flagship Arab Light to European customers at a premium of USD 27.85 in May vs. a discount of USD 0.65 in March. Some East Asian refiners are going to pay north of USD 175 for “landing prices” — the sum of the barrel cost, its transport expense and other elements.

On the other hand, market participants, particularly the ones in touch with US policymakers, were more upbeat that the conflict has been on a de-escalating phase for nearly two weeks and are looking through this shock. In particular, the staggering evolution of artificial intelligence (AI) models has been lost in the fog of war during March after six-months of lukewarm performance. The rebound in AI stocks has been fast and furious, driving the performance of global stocks. The massive outperformance was also a result of positioning that became lighter in March. Investors were then subsequently caught off guard by the rally. Momentum investors like CTAs (Commodity Trading Advisors) are still more likely to buy equities than sell, even if prices remain unchanged or marginally lower, supporting volatility suppression and price stability.

Despite the more hawkish tone adopted by policymakers, most commentary suggests they will remain patient and avoid acting before there is more clarity on the duration and impact of the conflict. This is wise and in line with our view that policymakers should talk hawkish to anchor expectations, but do nothing, in line with the seminal “Maradona Theory of Interest Rates” speech by Sir Mervyn King in 2005, a theme fitting for a World Cup year where Argentina is defending its title.1

The consensus coming out of the meetings was clear. Regardless of how long this conflict lasts, countries will double-down on national security matters, particularly on energy, materials, defence, and technology. This suggests commodities upside and dollar downside evolving in parallel with AI price disinflation and China exporting deflation to whoever is willing to buy. Weak USD, higher commodities, and further South-South trade and investments are bullish developments for emerging market (EM) assets. The weak dollar channel is expected to have more legs as the recent two major shocks emanated from unilateral US policy decisions, namely the Trade War in 2025 and Iran War in 2026. The mid-term elections and impact on US policy will be carefully monitored.

This week, the highlights will be the ceasefire negotiations alongside the US Senate hearing for the confirmation of prospective Federal Reserve (Fed) Chair Kevin Warsh. On the data front, the flash global purchasing manager indices (PMIs) for April will be keenly watched. The UK labour market is worth monitoring as well, given the country has been a faster adopter of AI than most DM peers. The impact will be overlaid with complicated local elections where the ruling Labour Party is being squeezed by new far-right (Reform) and far-left (Green) parties.

Emerging Markets

Asia

Malaysia: Petronas has extended its fuel security window by one month, confirming that petrol stations have sufficient supplies through to the end of June. The state firm reiterated calls for consumers to avoid panic buying (close to 40% of Malaysia's oil supply transits the Strait of Hormuz). The government has been tightening demand in parallel —a work-from-home mandate for public sector staff took effect on 15 April, the RON95 subsidy quota was cut from 300 to 200 litres per month, and the biodiesel blend was raised from B10 to B15 on 14 April via a phased B12 interim step. The cumulative effect is meaningful fuel demand suppression, which should buy Petronas more runway if Hormuz disruption persists.

Pakistan: Pakistan dispatched its first export shipment to Central Asia through a newly operational transit corridor via Iran, with frozen meat bound for Uzbekistan. The route is a direct response to the closure of the Afghan border after last October's clashes, which had severed Pakistan's overland access to landlocked Central Asia. Strategically, the corridor extends Pakistan's role in international transhipment and should lift activity at Karachi and Gwadar. Scale remains modest for now. FY25 exports to the five Central Asian countries totalled just USD 198m or 0.6% of total exports, mostly agricultural, but the geopolitical optics of a working Iran-Pakistan trade link amid the ongoing Iran war are significant in themselves.

South Korea: The Bank of Korea (BOK) published a structural analysis arguing that the country’s large trade surplus no longer provides meaningful support for the Won. Since 2015, the real effective exchange rate (REER) has trended lower despite persistent current account surpluses, and since 2023 the gap has widened as the Won has depreciated faster than most peers. The BOK frames this as a regime shift — surplus-generated external assets are increasingly recycled into private overseas investment (with US securities representing 63.4% of overseas holdings versus 25.3% on average for advanced economies) rather than into official reserves, and this "financial shock" channel now dominates the traditional export-appreciation channel. An ageing population reinforces the dynamic by lifting savings and weakening domestic demand. The policy implication is that deeper foreign investor participation via MSCI DM and WGBI inclusion is structurally important for Won stability.

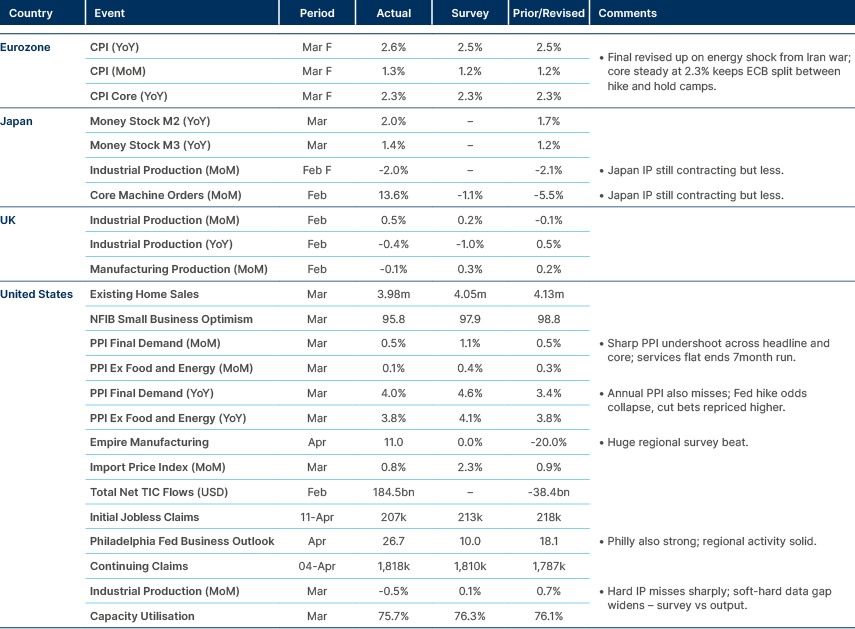

Import prices jumped 16.1% mom in March, the sharpest monthly gain since the Asian financial crisis and the biggest increase in more than 28 years. Crude oil import prices soared 88.5% mom, with Dubai crude nearly doubling to USD 128.52 from USD 68.40 in February, compounded by a 2.6% weaker Won. Naphtha rose 46.1% and jet fuel 67.1%. Export prices also rose 16.3% mom, the ninth consecutive monthly increase. Officials warned that sustained energy costs at these levels will broaden into core inflation if the Iran war drags on.

On the supply side, Seoul has secured 118 million barrels of alternative crude for April-May via routes bypassing Hormuz — 46 million for April, 72 million for May — sourced from 17 countries with Saudi Arabia the largest supplier. May's volumes cover around 82% of normal imports, and a further 22 million barrel strategic release is lined up for June via International Energy Agency (IEA) mechanisms. Naphtha remains the weaker link, with April supply running at 1.8 million tonnes against typical demand of 2.2; the government has ring-fenced KRW 674.4bn within a broader KRW 1.1trn supply-chain package to subsidise expensive imports and restore naphtha cracker utilisation toward 70% from roughly 55%.

Latin America

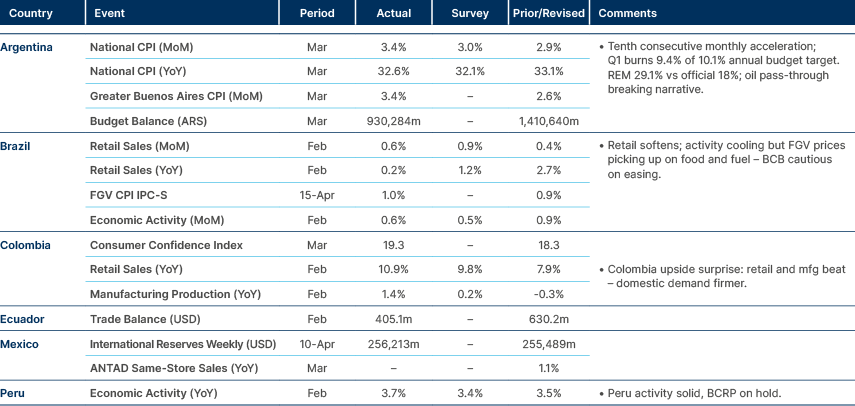

Argentina: The Central Bank of Argentina (BCRA) announced a further cut to the daily compliance share of reserve requirements, lowering it to 65% from 75%. The daily compliance regime requires banks to meet their full reserve requirement every single day rather than on an average basis over a maintenance period, forcing them to hold larger liquidity buffers and driving volatility in the overnight rate. It was imposed in August 2025 during election-driven dollarisation pressures. The unwind is welcome but has been notably slow. Reserve requirements on demand deposits remain at 45% versus 20% before the election stress, with 29% still unremunerated. Any further normalisation should support money and credit market functioning, but the trajectory suggests the BCRA remains cautious about giving up liquidity control.

Economy Minister Luis Caputo described the government's relationship with the IMF as "dream-like" following a Washington meeting with Managing Director Kristalina Georgieva, addressing questions about Argentina having missed its reserve accumulation target and needing a second waiver. The IMF's World Economic Outlook forecasts released alongside the review cut 2026 GDP growth to 3.5% from 4.0% but held 2027 at 4.0%. This is more optimistic than the local consensus of 3.3% and 3.1% respectively. The IMF sees an overall general government surplus of 0.5% of GDP in 2026 and gross debt falling to 70.4% from 80.3%.

Separately, Caputo told a Rosario audience that the "best 18 months in the last two decades" are starting, acknowledging March consumer price index (CPI) inflation would likely print above 3.0% mom due to the oil shock and seasonal education pressures, but insisting that disinflation is already resuming in April and activity is turning up. He framed the gap between government optimism and press pessimism as being at an all-time high.

Brazil: The government set a primary surplus target of 0.5% of GDP for 2027 in the Budget Guidelines Bill sent to Congress, with a BRL 73.2bn headline surplus and a +/- BRL 36.6bn tolerance margin. However, the bill excludes around BRL 65bn of expenditure, (BRL 57.8bn of judicial debt payments permitted for exclusion),reducing the de-facto surplus to just 0.1% of GDP. Debt is now projected to peak at 87.8% of GDP in 2029 before declining to 83.4% by 2036, a clear deterioration from previous projections that had the peak at 84.2% in 2028. The bill activates framework triggers after the 2025 deficit print, including a ban on new tax benefits and a cap on real personnel spending growth at 0.6%.

A Datafolha 7-9 April poll shows President Lula trailing Flávio Bolsonaro by 1pp (45% vs 46%) in a runoff simulation, a further though slowing improvement for Flávio. In the first-round scenario, Lula leads with 39% against Flávio's 35%. Lula has also lost his advantage against Ronaldo Caiado (PSD) and Romeu Zema (Novo) in runoff scenarios. Rejection is now 48% for Lula versus 46% for Flávio. The trend is consistent with a tight October race that could mirror or exceed the 2022 polarisation.

Mexico: Banamex Economic Studies Director Sergio Kurczyn publicly stated no one believes Banxico's or the Treasury's growth and inflation forecasts, marking the first substantive institutional criticism of Banxico's credibility from a mainstream analyst. Banxico has pushed its 3.0% convergence timing from Q3 2026 (held constantly since November 2024) to Q2 2027, while CPI inflation printed 4.59% yoy in March and core inflation has been above 4.0% for 11 straight months. Kurczyn argues the bank's de-facto target is 4.0%, not 3.0%, a critique that echoes Deputy Governor Jonathan Heath's recent dissent.

President Claudia Sheinbaum pre-announced budget cuts to offset fuel subsidy costs, which she put at MXN 5.0bn gross, MXN 2.5bn net after higher oil revenues. Sheinbaum refused to specify a timeline for dropping the subsidy and ruled out cuts to welfare programmes. This diverges from Fitch's assessment that the oil price impact would be fiscally neutral, and the austerity approach contradicts earlier warnings that operating spending cuts have reached practical limits — meaning the new cuts likely fall on public investment, contradicting the government's own growth-acceleration narrative.

The latest Banxico meeting minutes showed a 3-2 vote for a March rate cut, with the majority signalling one more 25 basis points (bps) cut to close the easing cycle. Deputy Governors Galia Borja and Heath called for caution. Core inflation at 4.45% yoy in March and consensus year-end CPI inflation at 4.21% highlight the disconnect with the board's 3.0% Q2 2027 convergence forecast. We expect a hold at 6.75% on 7 May, with a 25bps cut more likely in June but with the rising probability of a Q3 delay if energy and agricultural pressures persist. Fed policy divergence remains an under-discussed constraint.

Peru: With 92.9% of votes counted, Keiko Fujimori firmly secured first place at 17.06%, while the race for the second runoff slot tightened dramatically. Left-wing Roberto Sánchez of Together for Peru moved into second place at 11.97%, overtaking right-wing Rafael López Aliaga on 11.91%, a gap of just 9,309 votes. The remaining count is split between Peruvians abroad (lean right) and rural areas (lean left). López Aliaga has alleged fraud and demanded the National Jury of Elections annul the result within 24 hours, even threatening civil unrest. Markets have reacted sharply: USD/PEN approached 3.44 at Wednesday's close as investors repriced for a possible Fujimori-Sánchez runoff rather than the two-right-wing race previously discounted.

The earlier 65.6% count had shown a cleaner Fujimori-López Aliaga runoff scenario at 16.9% and 13.5%, but the subsequent shift puts that in question. The Senate result: Popular Force 22, Together for Peru 12, Popular Renewal 11, Good Government 7, marks the return of the bicameral system for the first time since 1993 and could improve governability if a right-wing coalition forms. However, post-campaign tensions between Fujimori and López Aliaga complicate that prospect, and the ultimate composition of Congress will materially shape the next administration's ability to legislate.

Central and Eastern Europe

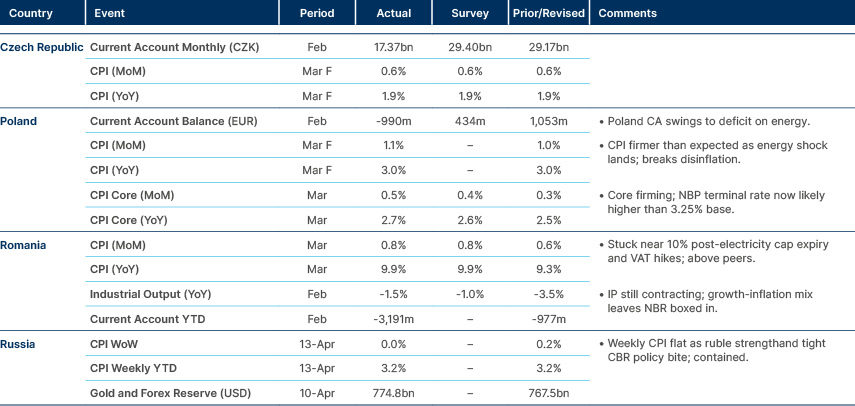

Poland: The Monetary Policy Committee (MPC) is likely to remain on hold at least until the 7-8 July sitting, when the inflation projection will be updated, and possibly for the rest of the year. At his 9 April press conference, Governor Adam Glapiński told reporters he does not expect changes in the near term, though he flagged concern about second-round effects. MPC members Wieslaw Janczyk and Ludwig Kotecki have both since indicated flat rates in coming quarters. Only the hawkish Joanna Tyrowicz has floated hiking, and even she views 4.75% as the optimal rate but favours a pause for uncertainty. The framework to trigger hikes is clear, CPI inflation of above 3.5% for three consecutive months plus other signs of inflation trouble. However, the government's fuel price measures and the broader inflation picture make this unlikely to materialise.

The setup implies a 3.75% hold through at least July and probably through November, with the November projection emerging as the next key decision point. The MPC has effectively ruled out further cuts without ruling in hikes,a holding pattern consistent with inflation settling in the 2.5-3.5% range rather than sustainably breaking below 2.5%.

Ukraine: The 32-hour Easter ceasefire ended at midnight after Moscow rejected Kyiv's offer to extend it and also rebuffed a proposed mutual halt on energy sector strikes. No long-distance strikes were recorded during the ceasefire and the front line did not move, though both sides claimed numerous violations; the Ukrainian General Staff alleged 7,696 Russian breaches. Russian drones hit a power facility in Chernihiv region this morning, cutting power to more than 12,000 residents, with further attacks reported in Zaporizhzhya. The brief pause leaves the underlying military and diplomatic picture unchanged.

Central Asia, Middle East, and Africa

Egypt: S&P affirmed Egypt's ‘B/B’ sovereign rating with a stable outlook on 10 April, balancing medium-term growth prospects and reform momentum against renewed external risks from a protracted Iran war. The ratings agency highlighted Egypt's strong pre-war external position — reform-driven gains in tourism, remittances and portfolio flows — but noted portfolio outflows of USD 10bn in the first month of the war, with non-resident holdings of local-currency government securities falling to USD 27bn at 25 March from a USD 38.1bn January peak. The EGP lost 13% of its value in March, but the authorities refrained from FX intervention, consistent with the flexible regime and IMF commitments. Downgrade risks include weakening reform momentum, renewed FX shortages, or higher borrowing costs; upgrade triggers require faster debt reduction, stronger foreign direct investment and progress on diversification.

Morocco: Prime Minister Aziz Akhannouch used a 15 April parliamentary address to reinforce the macro-stability narrative ahead of 23 September elections, highlighting 850,000 jobs created (170,000 per year versus 90,000 in 2016-21), MAD 52bn in direct social transfers to 4 million families, public investment up from MAD 230bn in 2021 to MAD 380bn in 2026, and tax revenues up 59.4% over the term. The fiscal deficit narrowed from 5.5% in 2021 to 3.5% in 2025, with Akhannouch reaffirming the 3.0% 2026 target. Public debt fell from 71.4% in 2020 to 65.9% projected in 2026, and inflation dropped from 6.6% in 2022 to 0.8% end-2025. Morocco regained investment-grade status in 2025 with S&P's upgrade to ‘BBB-’.

The policy mix is supportive for sovereign credit, but the key risk is pre-election fiscal drift as social spending expands and Iran war-driven commodity subsidy costs rise. Hitting the 3.0% deficit and debt trajectory is critical to preserving investment grade status. Akhannouch stepped down as party leader in February and rejected heading the next government, which reduces the perceived political stake in sustaining the current framework.

Nigeria: The Centre for the Promotion of Private Enterprise (CPPE) rejected a World Bank recommendation published in the 7 April Nigeria Development Update advising Nigeria to increase petroleum and food imports to ease supply constraints. The World Bank subsequently removed the report on 10 April and replaced it with a softer clarification. The CPPE argues the recommendation undermines progress toward energy self-sufficiency and risks eroding investor confidence in local refining while pressuring FX demand.

Saudi Arabia: Crude exports to China are set to halve to 20 million barrels in May, according to news agency reports. China had been the largest market for Saudi exports before the near-closure of Hormuz, and analysts point to record Asian premiums and China's drawdown of its strategic reserves as key drivers. The shift reflects both physical routing constraints and price-driven substitution.

OPEC data showed Saudi crude production fell 23.2% mom to 7.76 million barrels per day (mbpd) in March based on direct communication, though secondary-source data put actual production at just 6.97mbpd — the 0.79mbpd gap reflects the drawdown of extra February production into March export flows as part of the Kingdom's Hormuz contingency plan. The Arab Light price jumped 77% mom to USD 129/barrel in March. Production was slashed as storage capacity was rapidly exhausted.

The East-West pipeline, the critical workaround for bypassing Hormuz, has been restored to full 7mbpd capacity after last week's drone strike that had cut 700k bpd, alongside restoration of Manifa field output. The pipeline's nominal 5mbpd capacity can be temporarily boosted to 7mbpd, but vulnerability to further drone and missile attacks remains the binding constraint. Saudi's 7.2mbpd export capacity therefore still depends on this single asset holding up.

South Africa: The IMF’s April WEO downgraded South Africa's 2026 growth forecast to 1.0% from 1.3%, citing higher global energy prices and tighter financial conditions. The Middle East conflict is estimated to subtract a cumulative 0.6pps from growth over 2026-27. A modest recovery is expected from 2027 at 1.3%, rising gradually to 1.8%, which remains weak by both historical and EM-peer standards. Inflation is seen edging higher in 2026 before returning to target. The budget deficit is projected to narrow from 5.8% in 2025 to 4.3% in 2027 with the primary balance turning positive, but debt continues to rise given insufficient growth to stabilise the trajectory, and unemployment remains above 30% throughout the forecast horizon. The near-term cyclical shock is compounding a structural growth problem that continues to cap South Africa's fiscal consolidation path.

Türkiye: Fitch revised Türkiye's outlook from positive to stable while affirming its ‘BB-’ credit rating, acting outside of its scheduled 17 July review date. The ratings agency cited the sharp depletion of reserve buffers following the Iran war, with gross international reserves falling to USD 162bn in early April from USD 210bn at end-February and net FX reserves excluding swaps dropping to below USD 19bn from USD 79bn. The Central Bank of Türkiye (CBT) conducted more than USD 50bn in FX interventions. This removes the country’s last positive outlook across the major agencies, meaning near-term rating action in either direction has become less likely.

Fitch now sees the current account deficit widening to 2.5% of GDP in 2026 and 2.9% in 2027 on higher energy costs and lagged REER effects, gross FX reserves declining to 3.8 months of external payments by end-2027 (below ‘BB’ median), end-2026 inflation at 27% (up 2pps) before 21% in 2027, and GDP growth of 3.6% in 2026 and 4.2% in 2027 with downside risks. External financing needs remain heavy with USD 239bn of external debt maturing in the next 12 months. The fiscal deficit is projected to widen to 3.7% in 2026 and 4.0% in 2027 on pre-election stimulus.

Credit strengths remain a diversified economy, moderate public debt at 26% of GDP by 2027, resilient banking, and deposit dollarisation contained near 40%. The CBT's effective 300bps tightening in early March via a shift to overnight funding at 40% is judged supportive but insufficient to eliminate medium-term risks given Türkiye's history of abrupt policy reversals. Negative triggers would include renewed reserve deterioration, wider current account deficit, sharper dollarisation, or destabilising easing.

Zambia: Zambia secured a USD 1.5bn investment from China Machinery Engineering Corporation to develop a 900MW power portfolio split evenly across coal, solar and wind. The investment aligns with the 10,000MW by 2031 installed capacity target, a core pillar of industrialisation strategy. Electricity shortages have been a persistent drag on activity, particularly in mining, and the scale signals improving investor confidence alongside recent reform progress.

Developed Markets

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. https://www.bankofengland.co.uk/-/media/boe/files/speech/2005/monetary-policy-practice-ahead-of-theory#:~:text=In%20recent%20years%20the%20Bank,move%20either%20up%20or%20down