- Brent crude rose back above USD 110 after Iran struck a nuclear plant in the UAE.

- US-China summit achieved the goal of managing downside risks.

- China retail sales were weak in April, fixed asset investment also declined.

- Samsung Electronics extended talks with its labour union to avert a severe strike

- The World Bank increased Vietnam growth estimates, despite macro concerns.

- S&P revised down Mexico’s ‘BBB+’ sovereign rating outlook from stable to negative.

- Polish monetary policy council member said rate hikes may be on the table by July.

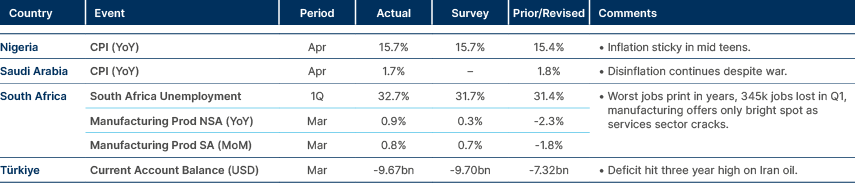

- S&P raised Nigeria’s sovereign rating from ‘B-’ to ‘B’, the first upgrade since 2012.

- Russia launched what looks like the heaviest aerial strikes of the year overnight on Ukraine.

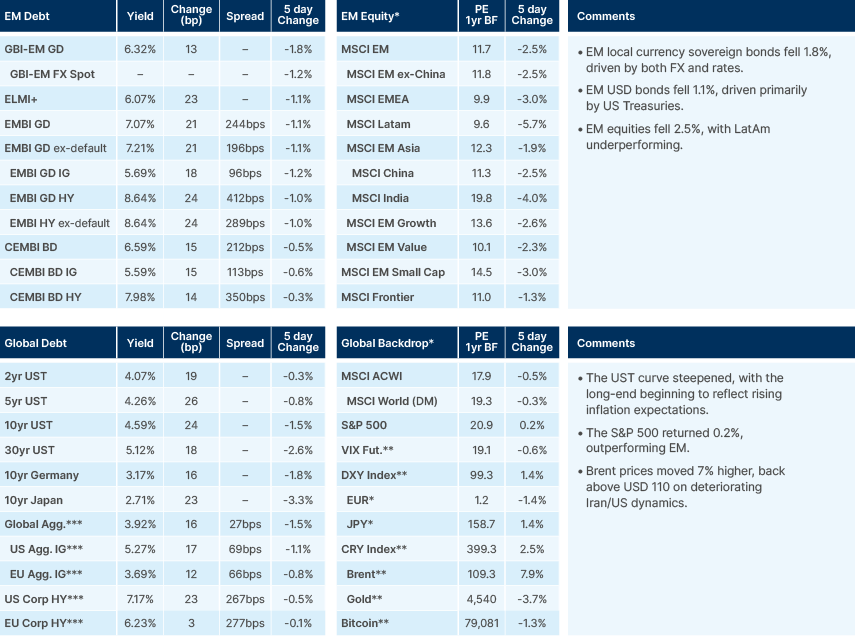

Last week performance and comments

Global Macro

Brent crude rose above USD 110 again this morning after a drone strike hit a United Arab Emirates (UAE) nuclear power plant. US President Donald Trump posted that "for Iran, the clock is ticking, and they better get moving, FAST, or there won't be anything left of them. TIME IS OF THE ESSENCE." Markets are reading this as a return to a coercive negotiating posture rather than a renewed war footing, though the distinction is thin. The persistence of the Strait of Hormuz closure (SoH), and with-it high oil prices, is now leading to the long end of global yield curves to move higher, given the limited expectations for rate hikes this year. The yield on 30-year US Treasury hit 5.13%, the highest since 2007. At the same time, UK 30-year Gilts above 5.8% trade at their highest level since 1997, 30-year Japanese Government Bonds are at a record high at 4.1%, and German Bunds at their highest level since 2011 at 3.68%. Concerns around fiscal deficits continue to drive in UK and Japanese yields higher. Japanese Prime Minister Sanae Takaichi is reportedly about to announce an extra budget measure to combat rising fuel prices, reportedly between 0.4-0.7% of GDP, according to Reuters.

These moves in rates, alongside a lack of good news on Iran and oil inventories continuing to drain, threaten to change the mood around risk assets, after a very strong two-month run driven primarily by semiconductors and the AI infrastructure ecosystem more broadly. The equity market rally has been supported by strong Q1-2026 corporate earnings, which overshadowed concerns around the immediate impact of high oil prices on the economy. However, corporate earnings season is now mostly behind us, and equity prices have reacted to positive outlooks and earnings beats already. The last of the big AI names to report is the biggest, Nvidia, which will give its Q1 earnings and outlook on Wednesday. Nvidia has beaten earnings expectations for the last 13 quarters in a row and is widely expected to do so again. But with positioning across global stocks now heavier, the macro picture deteriorating from rising inflation and interest rates, and the positive catalyst of earnings now in the rearview mirror, the bar for Nvidia earnings to deliver the ‘wow’ factor that may be necessary to keep the pump going is undeniably high.

The US-China summit delivered on the modest ambition that was set for it, which was to manage downside risk rather than reset the relationship. This is the first of four scheduled bilateral engagements in 2026, with Chinese President Xi Jinping due to visit Washington in the autumn alongside the G20 (US-hosted) and APEC (China-hosted) summits. The White House factsheet framed the outcome as "strategic stability on the basis of fairness and reciprocity," language that is deliberately low-ambition and designed to avoid commitments either side might struggle to deliver.1 The same document mentions the establishment a Board of Trade and a Board of Investments to manage capital flows between countries.

On Iran, the two sides agreed that Iran can never possess a nuclear weapon, that the Strait of Hormuz must reopen, and that China opposes any tolling regime on the waterway. China also committed to buy more US crude to reduce dependence on the Gulf chokepoint. In Taiwan, Xi emphasised that mishandling of the relationship could lead to collision; Trump said policy has not changed but added in an Air Force One interview that “the last thing the US needs is a war 9,500 miles away” The pattern across all three flashpoints is similar:enough common framing to keep the channels open, no binding commitments that constrain either side.

On trade, China committed to purchase USD 17bn more than last year's target, which was itself met, of agricultural products and 200 Boeing jets. On tech, Chinese state media is reporting that ten named Chinese tech firms, including Tencent and Alibaba, are now cleared to buy Nvidia H200 GPUs. This has not been confirmed on the US side, but the fact that Jensen Huang was present at the meeting is itself a signal. If confirmed, this is the most market-relevant single deliverable from the summit, given the implications for both Nvidia's addressable market and the broader pricing of the export-control overhang in US semiconductor names.

Russian President Vladimir Putin is due to visit Xi in Beijing this week. Chinese media is framing the trip as independent from Trump's visit, but the timing could be viewed as suspicious as this is the 25th Putin-Xi meeting, underscoring a relationship that is structurally deeper than anything either leader maintains in the West.

In other news, the Abu Dabi National Oil Company (ADNOC)'s investor relations team indicated that more vessels are moving through the Strait of Hormuz than the media is reporting, with production above the 1.5 million barrels per day (mbpd) figure widely cited (versus 3.5mbpd pre-war). ADNOC has infrastructure capacity to reach 5mbpd in 2027, with additional capex required to move to 6mbpd. The pipeline to Oman is set to double capacity bypassing the Strait of Hormuz, from 1.5 to 3.0mbpd, by 2027.

Bloomberg has separately reported that both Saudi Arabia and the UAE counter-attacked Iran, with the UAE having tried unsuccessfully to coordinate the response with Qatar and Saudi Arabia. This is probably the proximate reason the UAE was pushed out of OPEC earlier than the formal timeline suggested. ANZ Research now sees the effective floor on global oil inventories, defined as 20 days of cover, being reached by late July, which is the timeline the rates market is increasingly pricing.

Emerging Markets

Asia

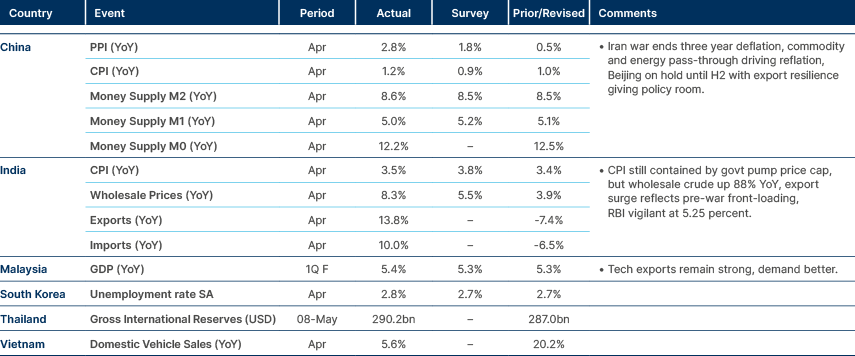

Inflation below expected in India, above expected in China.

China: April’s activity data disappointed across the board. Retail sales were essentially flat at 0.2% yoy against consensus of 2.0%, the weakest print since December 2022, while industrial production grew 4.1% yoy versus 6.0% expected, the slowest in three years. Oil-intensive segments led the slowdown as gasoline and diesel exports fell sharply, though autos and electronics accelerated. The composition fits a domestic economy where fuel-price pass-through is choking consumption even as the AI-driven export complex continues to power ahead.

Fixed asset investment contracted 1.6% yoy in January-April against expectations of a 1.7% expansion, with property investment down 13.7% yoy, deeper than the 11.5% drop priced in, while new home prices fell 0.2% yoy. The property sector remains the binding constraint on any cyclical recovery, and the combination of weak consumption, contracting investment and a still-deflating housing market raises the bar for a policy response that does not address the underlying balance-sheet repair. The Chinese cyclical impulse cannot be relied on to offset the Iran-shock drag on the rest of emerging markets (EM).

India: The government is fast-tracking a deep-sea gas pipeline between Oman and India through the Arabian Sea, estimated at INR 400bn over five to seven years, to bypass the Strait of Hormuz. India imported 21.3m tonnes of liquified petroleum gas (LPG) and 25.8m tonnes of liquified natural gas (LNG) in FY26, equivalent to roughly 64% and 50% of consumption respectively, with around 90% sourced from the Middle East. Customs duties on gold and silver were raised from 6% to 15%, and platinum to 15.4%, alongside Indian Prime Minister Narendra Modi urging households to defer gold purchases for a year and cut fuel, cooking oil and fertiliser use.

The Indian rupee remains at record lows despite aggressive Reserve Bank of India (RBI) intervention. Reserves fell to USD 690.7bn on 1 May from USD 728.5bn at end-February, which is the visible cost of the defence so far. Petrol consumption rose 7.6% yoy in March and 6.8% in April, reflecting frozen pump prices that leave households with little incentive to adjust behaviour. The government has become more vocal about the fiscal burden of the freeze in recent days, which reads as preparing the ground for pump price increases in the coming weeks.

Malaysia: Central Bank Governor Rasheed Ghaffour said that broad-based measures to address the Iran-war fallout were not needed for now, signalling no near-term policy change. Household debt-to-GDP is stable at 84-85%, and consumer price index (CPI) inflation may reach the upper end of the 1.5-2.5% forecast range in 2026, although Ghaffour characterised pressures as supply driven rather than demand driven.

Prime Minister Anwar Ibrahim said the government is examining fuel subsidy cuts for the top 15% (T15) earners or top 20% (T20) earners, with the announcement expected mid-month. The T20 accounts for an estimated 30% of all fuel subsidies, so exclusion would save around MYR 1.5bn per month against a MYR 5bn monthly RON95 subsidy bill. The 2025 reform targeted T15 exclusion but never delivered, and the execution mechanism for identifying T20 users remains the real constraint, alongside political exposure given Chinese-Malaysian representation in the T20 base of Anwar's coalition. The standard unleaded petrol grade (RON95) accounts for around 5.5% of the CPI inflation basket, so any move will feed through to headline inflation.

South Korea: Samsung shares jumped as much as 6.7% in Seoul this morning as management entered make-or-break wage negotiations with its largest union aimed at averting a strike that could disrupt operations at the world's biggest memory chipmaker. A Korean court partially granted an injunction against potential illegal union actions, reducing tail-risk pricing. Before the de-escalation, the Industry Minister had warned of emergency arbitration if the union proceeded with the planned 18-day strike from 21 May to 7 June. Samsung's scale is systemic, with revenue at roughly 12.5% of GDP, 129,000 employees and 1,700-plus suppliers. Strike-related production disruption could cost up to KRW 1trn per day, with in-process wafer losses potentially reaching KRW 100trn given five-month production cycles.

Ratings agency Fitch flagged upside risk to growth on surging semiconductor demand, with Q1 GDP at 3.6% yoy led by chips. It expects sustained current account surpluses in 2026-27, a stronger Won by end-2026 and end-2027, and a policy rate around 2.5% with a possible hike in late 2026 if Middle East energy shocks push inflation higher. Fitch sees the Strait of Hormuz effectively blocked until July, with oil at USD 100-110 before sliding to USD 70 in September. Separately, Seoul apartment listings dropped 4.2% in two days after the heavy capital gains tax on multi-homeowners was reinstated, with districts like Seongbuk, Guro and Gangdong seeing 18-21% declines in a pattern that closely resembles the Moon-era listing lockup.

Vietnam: The World Bank lifted its 2026 Vietnam GDP forecast to 6.8% from 6.3%, with recovery expected in 2027-28 as the oil shock subsides. The medium-term story remains intact, supported by resilient exports, sustained foreign direct investment (FDI) and broadly stable macroeconomic conditions.

Beneath the headline, the World Bank flagged a widening set of vulnerabilities. Corporate sector leverage is now the highest in the Association of Southeast Asian Nations (ASEAN), credit is concentrated in real estate with early signs of bank liquidity strain, and FX pressures are building from a Q1 trade deficit, a stronger dollar and higher oil import costs. The central policy challenge is shifting the FDI calculus from quantity to quality and mobilising private capital at scale to finance the approximately USD 320bn public investment pipeline that the traditional bank-based model cannot fully fund.

Latin America

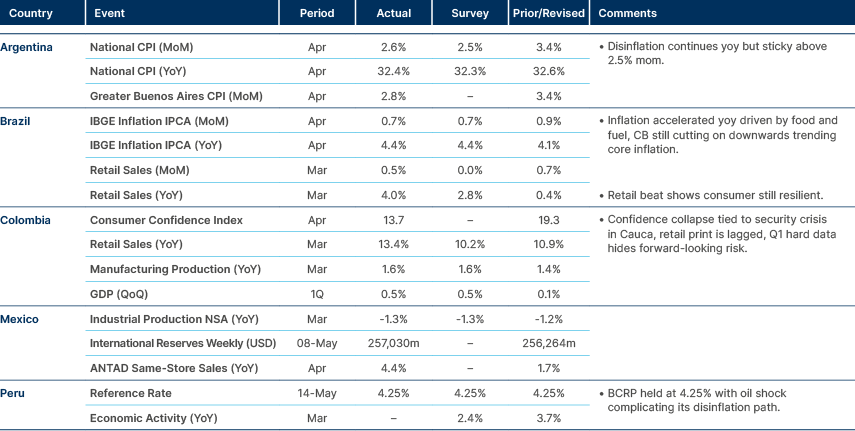

Inflation higher in Brazil but still under 4.5% threshold.

Brazil: Brazil’s Extended National Consumer Price Index (IPCA) printed 0.67% mom in April, with food and health and personal care driving the surprise, while transport eased as airfares offset fuel pressures. Headline inflation rose to 4.39% yoy from 4.14%, approaching the 4.50% upper band around the 3.00% target. Focus 2026 inflation rose for a ninth consecutive week to 4.91%, although the 2028 print paused its rise at 3.64%, which may indicate analysts are responding to the central bank (Copom)'s hawkish guidance. The Iran shock has trimmed the cycle's magnitude rather than its direction, and Focus has the Selic at 13.00% by end-2026 versus 12.25% in January.

On the political front, Flávio Bolsonaro said his contact with jailed former Banco Master owner Daniel Vorcaro related to private film sponsorship rather than favour-trading. The denial followed Intercept Brasil publishing the exchange after Flávio had earlier denied any contact, which is the part that damages his standing regardless of substance. Other right-wing names being floated include Ronaldo Caiado and Romeu Zema, both polling below 5%. The net effect is a lift for President Lula ahead of October.

Colombia: Democratic Centre candidate Paloma Valencia's Polymarket odds collapsed from above 45% to 18.6%, with Abelardo de la Espriella now leading at 44% and Ivan Cepeda at 39%. Polymarket liquidity in non-US markets is thin, so this reads as investor sentiment rather than voter intent, but the collapse reflects unforced errors that the candidate has shown no sign of correcting.

Valencia's insistence on appointing former president Alvaro Uribe as defence minister is electorally damaging given his association with corruption scandals and the false positives case. A recent debate she staged using AI without real opponents was sharply criticised. Her populist economic proposals also sit awkwardly with her fiscal consolidation positioning, including a roughly 30% electricity tariff cut by presidential decree with no clear funding path, and a SOAT exemption (mandatory traffic accident insurance) for sub-250cc motorcycles after she had previously criticised Gustavo Petro for similar measures. The right has fragmented, and de la Espriella now appears to be consolidating support as the orthodox far-right challenger against Cepeda.

In other news, on Friday two members of the right-wing presidential campaign were killed in a rural part of Cubarral, south of Bogota. The campaign has been marked by violence, which is also the key concern for Colombians. Last year a Senator and pre-candidate for President Miguel Uribe Turbay was murdered in Bogotá.

Mexico: S&P revised the sovereign outlook from stable to negative while affirming the ‘BBB’ foreign-currency and ‘BBB+’ local currency ratings. It cited weakening fiscal flexibility, with general government debt likely to rise faster than expected on weak growth, spending rigidity and the contingent liabilities of state owned energy companies PEMEX and CFE. The International Monetary Fund April fiscal monitor raised the 2026 net debt projection by 1.3% of GDP, reinforcing the trajectory. The downgrade window is usually 12-18 months, but could be up to 24 months absent meaningful consolidation, while pragmatism on US-Mexico-Canada Agreement is S&P's base case.

President Claudia Sheinbaum has been more open to private investment than her predecessor, but implementation has been disappointingly slow according to S&P. The government has raised tax revenues on imports from China, but a broader tax reform is currently off the table. The combination of welfare-spending rigidity, persistent PEMEX support and one-off fuel-subsidy costs will likely force the issue in the second half of her term after the mid-2027 midterms. No meaningful reform can be expected in 2026 or H1 2027 given the political calendar.

Peru: The authorities confirmed Roberto Sánchez (Together for Peru, left) received 12% of the votes and will go to the second runoff against Keiko Fujimori, who leads with 17.1%. Rafael López Aliaga (Popular Renewal, right) finished in third with 11.9%, a gap of just 21,200 votes.

The count has progressed slowly amid allegations of irregularities, with technical and logistical delays forcing an extended second voting day on 13 April. Aliaga has demanded an international audit and has refused to recognise results without a full review on fraud grounds. Sánchez is strong in the interior, Aliaga in Lima, and pending special electoral jury (JEE) adjudications on contested tally sheets could still change the outcome.

Central and Eastern Europe

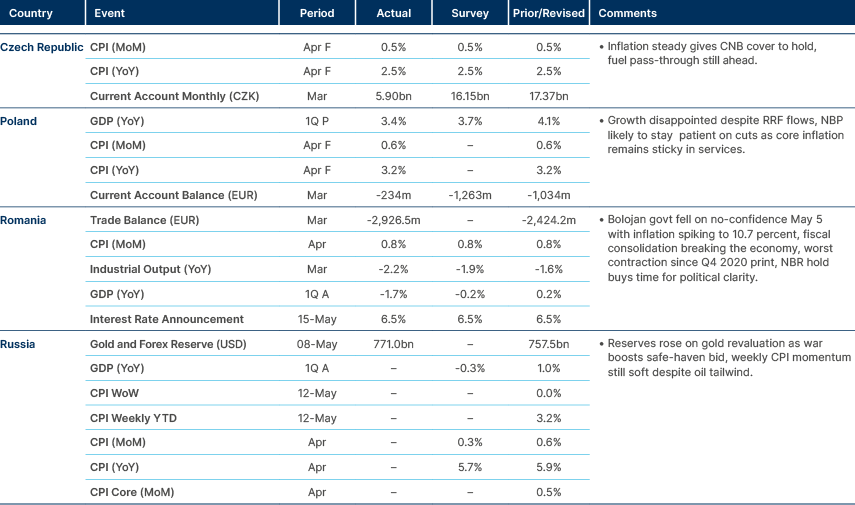

Romanian GDP growth worst since Q4 2020.

Hungary: Tisza extended its lead over Fidesz to 40% in the latest poll by 21 Research Centre, scoring 60% of all voters against 20% for Fidesz, and 71% versus 21% among decided voters certain to vote. The pollster argues the swing exceeds the typical winner-attraction effect that follows decisive election results.

Finance Minister-designate András Kármán told parliament the revised 2026 budget will be presented by the end of summer and the 2027 draft by end-October, breaking the previous spring-summer practice. He flagged HUF 2,400bn of potential interest savings over four years from lower yields, alongside procurement-review room. Kármán also committed to Euro adoption by 2030 at the latest, the gradual phase-out of special taxes, and a 1% wealth tax on a narrow segment.

Poland: Monetary Policy Council (MPC) member Ludwik Kotecki told financial news agency PAP Biznes that the council could discuss rate hikes as early as the July sitting if the Iran conflict drags on and oil pass-through broadens. Stabilisation remains Kotecki’s base case, with no cuts before mid-2027. He explicitly invoked the 2021 mistake of reacting too late to inflationary threats. The MPC dislikes guiding expectations and prefers to move first and explain afterwards, so a July surprise cannot be ruled out.

Fellow MPC member Henryk Wnorowski struck a similar tone in Reuters: current restrictiveness is appropriate, but the council has become more hawkish, with hikes now more likely than cuts. CPI inflation sits just below 3.5% yoy, at the top of the band, with limited margin. The March rate cut, taken after the US/Iran war had already begun, raises the bar for any quick reversal since the move would in retrospect look ill-conceived. The MPC will wait at least until the July CPI and GDP projections, but any signs of higher core inflation will materially increase the probability of a hike.

Ukraine: Russia launched what appeared to be its heaviest aerial strikes of the year overnight, switching from drones to missiles. Kyiv was hit, with at least one civilian killed and 30-plus wounded, and part of a residential block was destroyed. Ukraine’s state-owned transporter Ukrzaliznytsya reported 23 hits across bridges, locomotives and carriages, while Naftogaz facilities were struck in Kharkiv and Zhytomyr. The large escalation came after Ukraine drone attacks led to casualties in Moscow and is at odds with Putin’s rhetoric that the War could be near its end.

The political dimension matters in this case: Slovakia closed border crossings after Uzhhorod, capital of Transcarpathia, was hit by drones for the first time in the war, and Hungary summoned the Russian ambassador over strikes on ethnic-Hungarian areas. By targeting Transcarpathia, Moscow demonstrated that no area of Ukraine is now considered safe, the strategic signal it appears to have wanted to send into the EU's frontline states. Moscow and Kyiv have gradually lost hope on the US delivering a cease fire and peace agreement seeing the EU as the key interlocutor for such purposes.

Middle East and Africa

South Africa's unemployment remains very high.

Sub Saharan Africa: France’s President Emmanuel Macron announced a EUR 23bn investment package for Africa at the Nairobi summit, split between EUR 14bn from French entities and EUR 9bn from African investors, targeting energy transition, AI and digital, maritime and agriculture, with 250k jobs claimed across Africa and France.

Macron positioned France as an alternative partner to China and the US in industrialisation, logistics and green energy. Alas, large pledges have historically translated slowly into tangible infrastructure, and African economies need significantly higher capital than the package implies.

Egypt: The IMF’s Managing Director Kristalina Georgieva commended Egypt's reform commitment and pro-active Iran-crisis stance, meeting President Abdel Fattah El-Sisi on the sidelines of the Africa-France summit in Nairobi. The two also discussed energy and food security implications of the regional conflict for import-dependent emerging market countries.

An IMF mission arrives in Cairo on 15 June for the combined seventh and eighth extended fund facility (EFF) reviews. The previous review flagged primary surplus delivery was on track, but divestment and maturity lengthening as stalled. Approval would unlock USD 3.3bn across the EFF and resilience and sustainability facility (RSF) facilities, and the tone going in looks constructive.

Nigeria: S&P upgraded Nigeria’s sovereign rating from ‘B-’ to ‘B’, the first upgrade since 2012, driven by exchange rate liberalisation and higher oil output. Debt is projected at around 36% of GDP, and the deficit is expected to average 3.5% of GDP over 2026-2029. Further upgrades are possible if fiscal performance improves.

This is a meaningful endorsement of the Tinubu-era reform agenda and validates the painful FX adjustment that preceded it. The action should be supportive for Nigerian Eurobond spreads at the margin, though local-currency dynamics will continue to be driven by oil-price realisations and the Central Bank of Nigeria's evolving FX framework rather than by the rating itself.

Saudi Arabia: Crude production fell another 11.4% mom to 6.9mbpd in April, after a 23.2% mom drop in March, but secondary sources had actual output at just 6.3mbpd. The Kingdom supplied more than it pumped, drawing on the February's 0.8mbpd contingency build that has now worked through. Aramco's CEO said Red Sea lifting capacity reached 5.0mbpd in May, well above the roughly 3.5m average through March-April, and the East-West pipeline is now at 7.0mbpd. Arab Light moderated 12% mom to USD 107/barrel after the 77% jump at war onset.

Crude exports to China are set to collapse to a record-low 330kbpd in June against a 2025 average of 1.39mbpd. Sinopec, Sinochem and Rongsheng all cut June liftings, and Aramco's reduction of its Asia premium to USD 15.50/bbl from USD 19.50 was smaller than the market wanted. Premium pricing is now the binding constraint on Saudi flow to its largest historic customer, part of the Kingdom's optimisation strategy given strong realisations elsewhere.

South Africa: Patrice Motsepe credited public-private partnerships for restoring mining competitiveness at the Africa Forward Summit in Nairobi. With President Cyril Ramaphosa weakened by a fresh scandal, African National Congress (ANC) factions are reportedly consolidating behind Motsepe as a market-friendly succession candidate against Deputy President Paul Mashatile and Secretary General Fikile Mbalula. Motsepe distanced himself from a campaign website, but the speculation is active.

The rail, port and pipeline company Transnet reported a strong operational recovery at its eight commercial ports, with throughput up 4.2% to around 304m tonnes in 2025/26, the strongest growth since 2011/12. Vessel arrivals rose 9% yoy, automotive cargo led at +13.3%, containers +7.1% on a 22% jump in citrus exports, and dry bulk +4.2% on chrome, magnetite and manganese demand. This is the first credible evidence the Transnet reform programme is delivering, removing a long-standing drag on the mining export story.

United Arab Emirates: UAE Banks Federation Chair Abdul Aziz Al Ghurair pushed back on capital flight narratives, framing flows as risk recalibration rather than panic. The defence rests on strong capital adequacy, proactive communication from the Central Bank and diversified non-oil exposure. The Financial Institution Resilience Package is backed by reserves over AED 1trn (USD 272bn), and a US-UAE dollar swap line under discussion.

Zambia: Global copper company First Quantum Minerals (FQM) reaffirmed Zambia's centrality to its long-term strategy in its 2025 sustainability report, with Kansanshi S3 reaching commercial production in 2025. Group economic contribution totalled USD 4.1bn (USD 1.1bn tax and royalties, USD 564m wages, USD 2.4bn procurement).

FQM remains the dominant single copper producer at around 396kt or 44.5% of 2025 national output, with Kansanshi at 181kt and Sentinel/Trident at 189kt. National output was 890,346 tonnes, short of the 1m-tonne target. Power-supply reliability was flagged as the binding operational risk, which underscores the broader importance of electricity-sector stability for any copper-sector expansion narrative.

Developed Markets

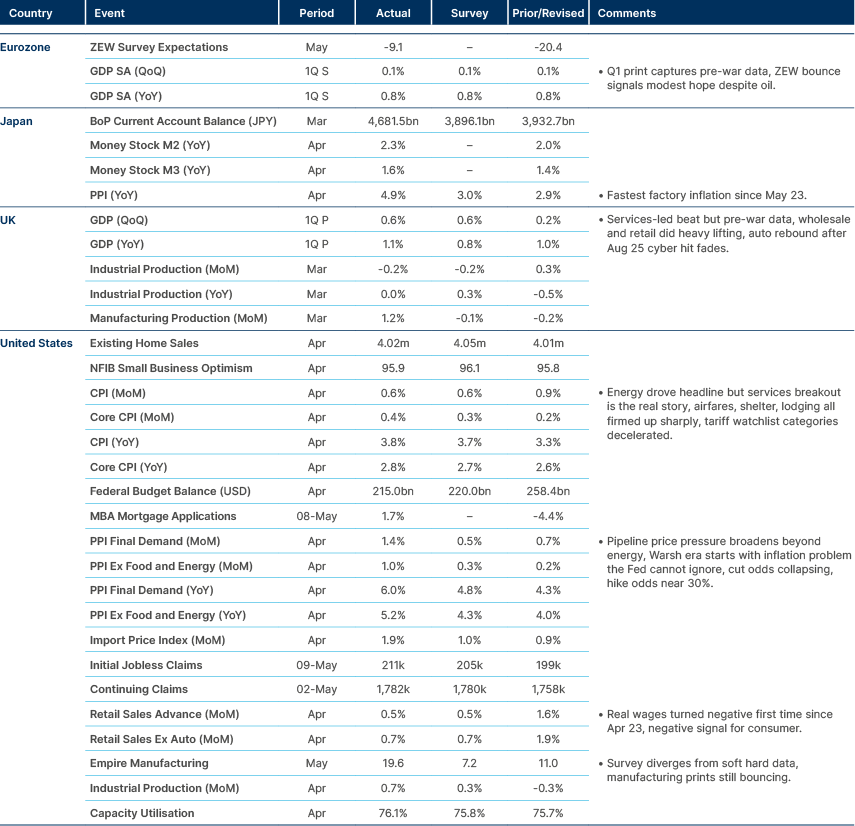

US CPI higher than expected, energy driven but services also up.

United Kingdom: A by-election was triggered in Makerfield near Manchester, after the incumbent MP stood down to pave the way for Mayor of Greater Manchester Andy Burnham to win the seat and return to Westminster. The strategy is not riskless as Reform UK swept the surrounding local areas in recent elections, so the result is worth watching closely.

Prime Minister Keir Starmer continues to resist calls to stand down. If Burnham succeeds in returning and the Starmer position erodes, Burnham would be the most likely successor, though markets would prefer Wes Streeting on a centrist-fiscal basis. The trajectory of internal Labour Party positioning currently points more clearly toward Burnham, which is relevant for Gilt term-premium pricing alongside the global rates backdrop.

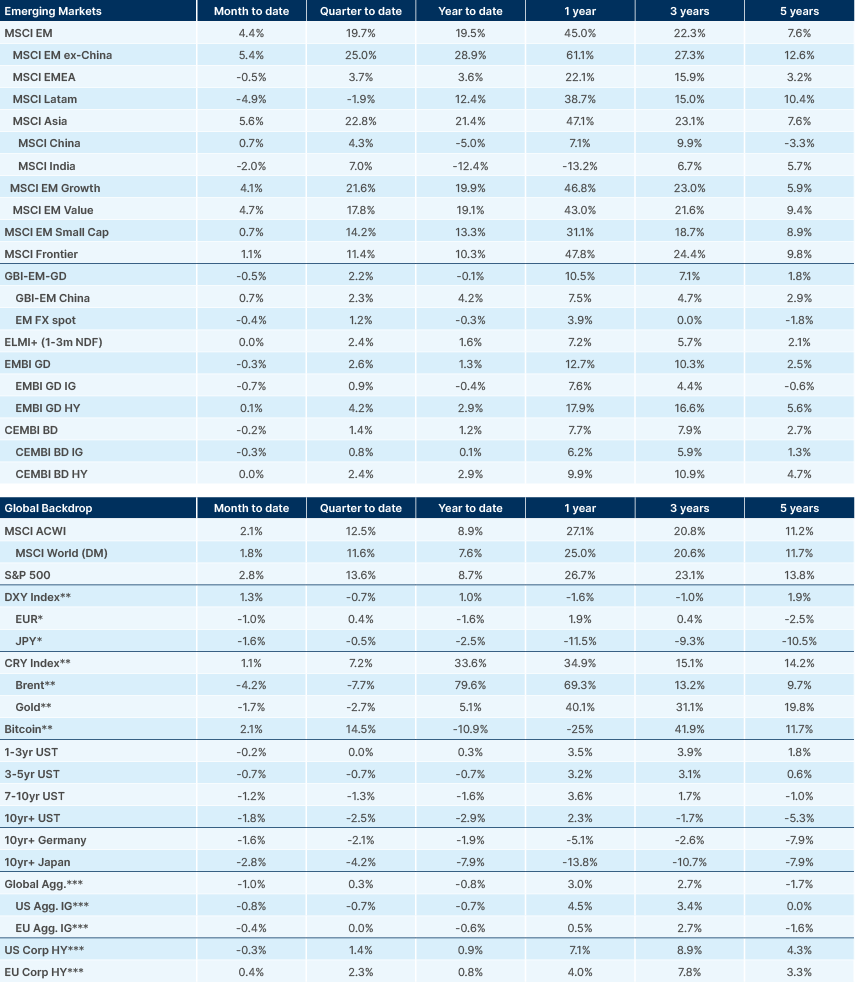

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. See - See https://www.whitehouse.gov/fact-sheets/2026/05/fact-sheet-president-donald-j-trump-secures-historic-deals-with-china-delivering-for-american-workers-farmers-and-industry