- Trump set a 48-hour deadline for Iran to open the Strait of Hormuz, before extending it by five days.

- Fed/ECB/BOJ/BOE all held rates, with hawkish tilts given higher energy prices.

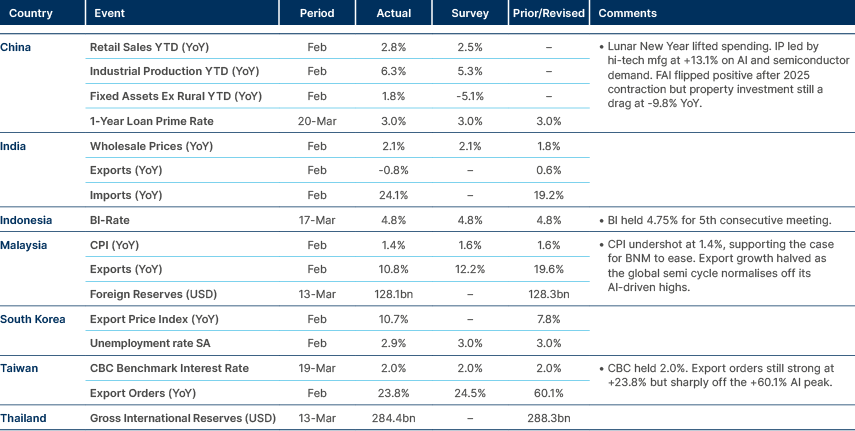

- Korea designated naphtha "economic security item" after 45% w/w price surge.

- Malaysia’s Investment Minister confirmed the Malaysia-US trade deal is nullified.

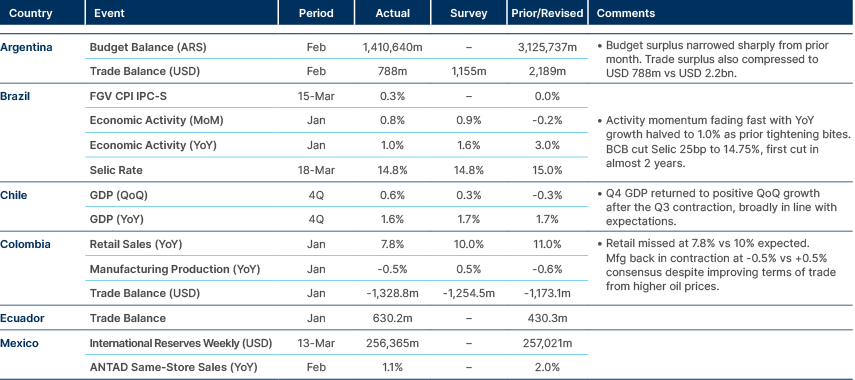

- Argentina says USD 9bn in FX maturities through 2027 already financed.

- Brazil’s Central Bank cut rates by 25bps to 14.75%.

- Chile bypassing Congress on fuel prices via decree.

- Mexico's electoral reform downgraded to budget-only after allied defections.

- Turkey capped fuel prices via equalisation mechanism.

- Iran struck Qatar’s Ras Laffan Industrial City.

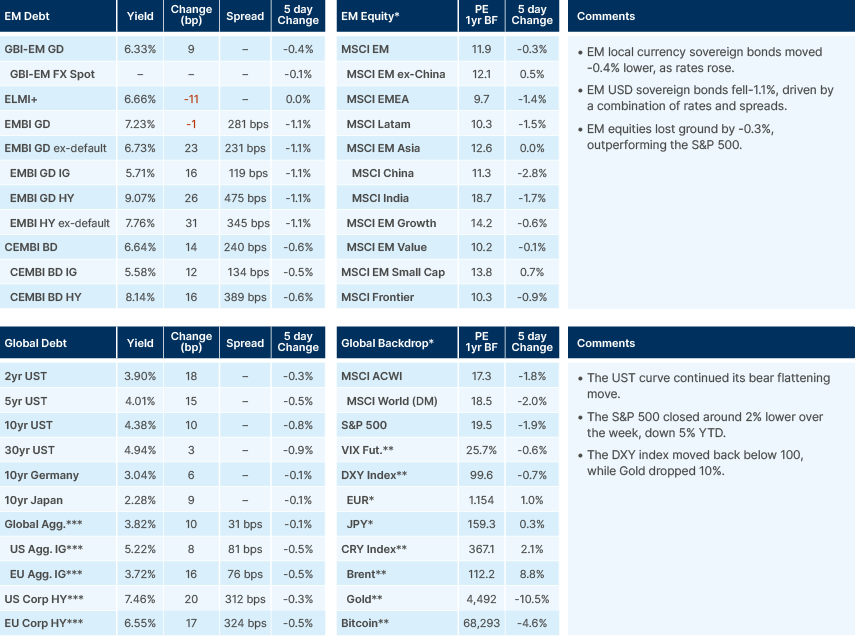

Last week performance and comments

Global Macro

The pattern of rhetorical de-escalation followed by further escalation by the US and Israel remained in place until midnight Saturday (EST), when Trump gave a 48-hour ultimatum for Iran to reopen the Strait fully or he would "obliterate" its power plants. The threat was met with an "eye-for-an-eye" response by Iran, which published a list of energy and water desalination assets that would be targeted in response. That set the market up for a bad opening on Monday, with Brent Crude trading at USD 113, equity markets down and spreads wider. But this morning, Trump posted that he extended the deadline by five days to allow for ongoing "constructive" negotiations between the US and Iran.

Asset prices immediately whipsawed — equities rallied, bond yields fell, and Brent briefly dipped below USD 100 before settling around USD 105. Iranian media quickly denied talks with the US, claiming victory in this game of brinkmanship — consistent with the game of ‘Chicken’ we outlined last week. This is obviously a fast-moving situation, but the US President changing his mind about a serious threat and deadline suggests markets may be approaching levels that activate a "Trump put". It is also possible that Iran is considerably more open to de-escalation than it publicly acknowledges: Iranian strike pace continues to decline, interception rates remain elevated, and the concessions to India, Pakistan, and China on Strait transit all point to a regime looking for an exit.

Iranian attacks on Israel and Gulf states continued over the weekend, with drones intercepted over Saudi Arabia's Eastern Province, a missile intercepted targeting Riyadh, and a missile strike near an Israeli nuclear facility that left hundreds injured. Strikes remained focused on Israel and the UAE. Iran has warned of "zero restraint" if its energy facilities are struck again, and Mojtaba Khamenei demanded reparations and recognition of Iranian rights as preconditions for any negotiation.

The unofficial demands of both sides seem clearer, as per various media reports. The US is seeking (per Axios): no missile programme for five years, zero uranium enrichment, decommissioning of Natanz, Isfahan and Fordow, strict external observation of centrifuge activity, regional arms control treaties with a 1,000-missile cap, and no proxy financing. Iran (per Tasnim) demands guarantee against future attack, closure of US regional military bases, lifting of sanctions and compensation for damage incurred during the war, an end to the war on all regional fronts, a new legal regime for the Strait of Hormuz, and extradition of anti-Iranian media agents. The gap is large with the US effectively demanding Iran dismantle its strategic deterrent, while Iran is demanding control of the Strait of Hormuz and some conditions that are not up to the US (Israel-Lebanon). Neither set is a realistic starting point, but the fact that both sides are defining terms publicly rather than through intermediaries is itself a form of progress, however tentative.

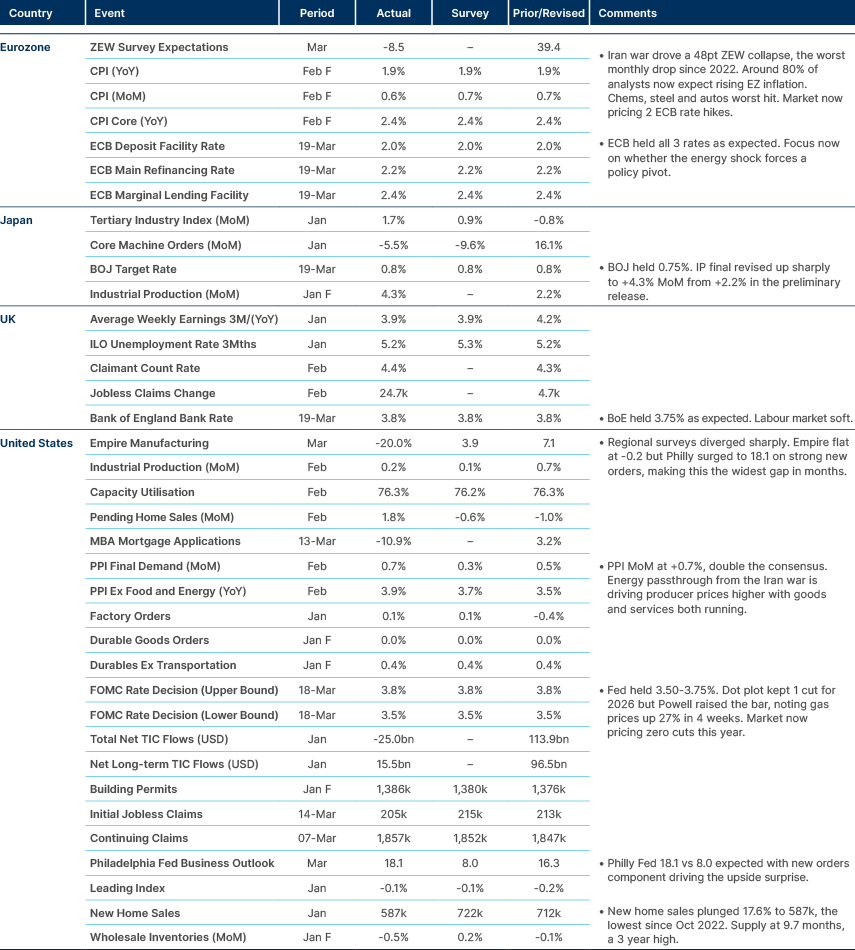

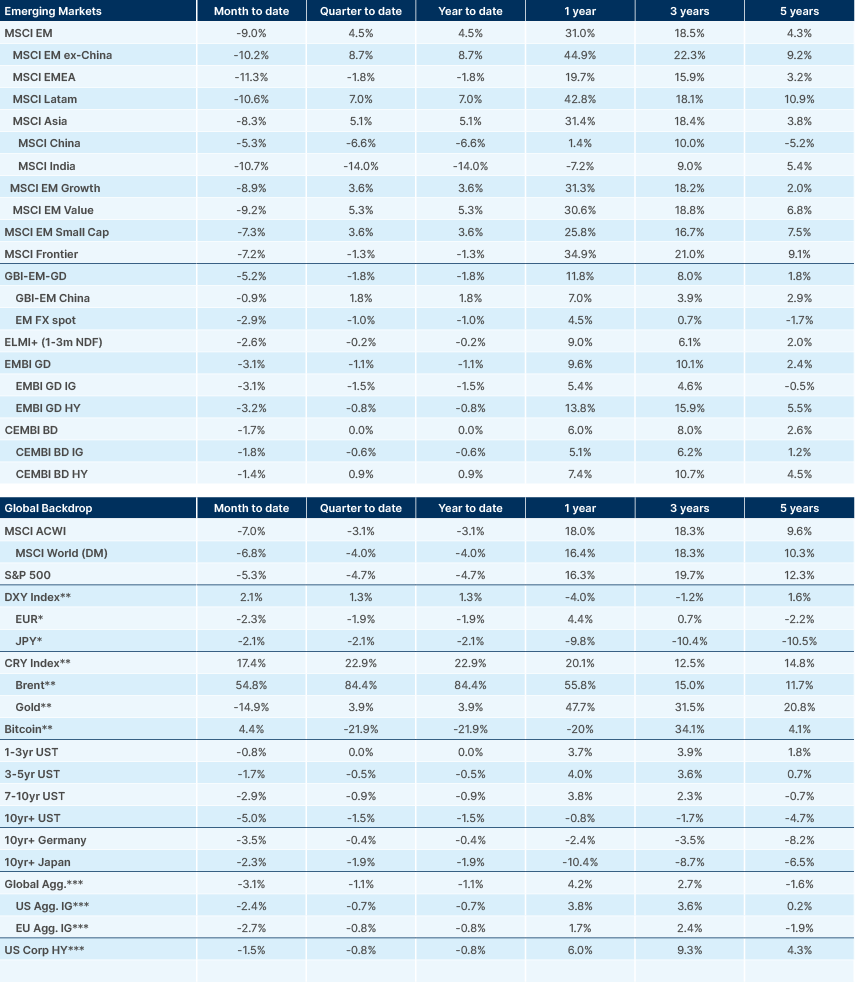

The big four central banks (Fed, ECB, BOJ, BOE) all left rates unchanged this week, but several hawkish dynamics emerging from the meetings led to a major selloff in government bonds. A Bloomberg report after the ECB decision suggested officials saw a possibility of a rate hike at the April meeting, and Bundesbank President Nagel indicated that more restrictive policy could be necessary if the inflation outlook worsened. By Friday, markets were pricing 77bps of ECB hikes this year, up from 47bps at the start of the week. The BOE voted unanimously to hold and dropped previous guidance that rates were likely to keep falling; markets moved to price 84bps of hikes, having priced cuts less than two weeks ago. The Fed still pencilled in one 2026 cut in the dot plot, but increased inflation forecasts, and by the end of the week Fed funds futures had completely priced out 2026 cuts.

The pricing of hikes is partially a function of fast repositioning from investors. The scenario for rates prior to the conflict was one where growth remained supported by AI investing, but the technology would keep weighing on the labour market. Further rate cuts than priced would be necessary, according to this thesis, to avoid wage disinflation turning into weaker growth. The reason why the Fed prices policy unchanged vs ECB and BOE is likely reflecting the Fed’s dual mandate to keep inflation at around target while maximising employment versus the pure inflation target of the other two institutions.

However, we believe rates have significantly more upside than downside from here. A quick de-escalation and oil price normalisation (even if at higher levels than pre-war) would allow for the market to price out hikes and maybe price some cuts in 2H 2026. A scenario of a protracted conflict where oil prices rise further from here would likely drive real wages to negative levels. This would depress demand, increasing the odds of faster layoffs and a more protracted recession, demanding much larger cuts than imagined. Central banks should, in our view, talk hawkishly to anchor inflation expectations, but sit tight to see how this conflict evolves. Inflation expectations measured on 5y5y inflation swap remain contained compared with historical levels, corroborating this scenario.

Emerging Markets

Asia

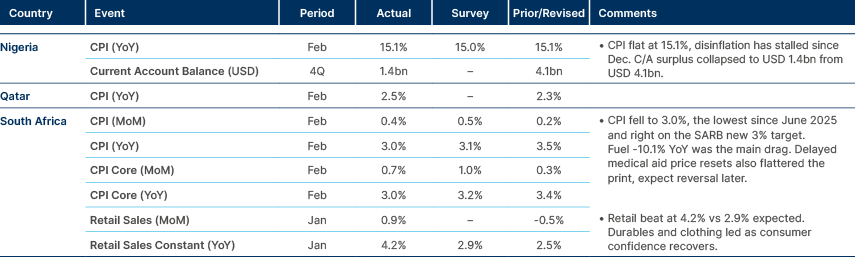

Indonesia: Bank Indonesia held at 4.75% for a sixth consecutive meeting and has dropped all dovish rhetoric, forced by the oil shock. The rupiah breached the psychological 17,000 level post-Iran war before recovering to 16,900–17,000; BI continues triple intervention to maintain currency stability. CPI hit 4.8% y/y in February, breaching the 2.5%±1% target band, though BI attributes this to base effects from 2025 electricity tariff cuts and expects a return to target in March. Core remains anchored. GDP accelerated to 5.4% y/y in Q4 on investment and consumption, and the government is boosting public spending in H1 2026. The key risk is that sustained oil prices could add 1.5–2.5pp to inflation through first- and second-round effects, bringing rate hikes back onto the table.

South Korea: Naphtha was designated a temporary “economic security item”, enabling monitoring, export restrictions, and active sourcing of alternatives. Korea sources 54% of naphtha imports via Hormuz, and prices have surged 45% w/w and 67% YTD. The naphtha supply disruption threatens ethylene production used in plastics, synthetic fibres, rubber, and shipbuilding. The government launched a KRW 1.5tn “Special Support for Middle East Damage” programme with import subsidies, emergency funds, and preferential loans.

BOK minutes from the 26 February meeting (pre-war) showed consensus for holding at 2.5% with a neutral-to-hawkish shift. Cuts are firmly off the table while the conflict continues. Separately, the government approved a USD 350bn US investment law (USD 150bn shipbuilding, USD 200bn strategic sectors) in exchange for reciprocal tariffs at 15%, with provisions to suspend if US tariff policy changes. Local economists warn the supplementary budget could inflame inflation and asset bubbles ahead of local elections.

Malaysia: Investment Minister Johari confirmed the Malaysia-US trade deal is nullified after the Supreme Court struck down Trump’s tariffs. The deal had set 19% tariffs on Malaysian goods in exchange for US export access and unrestricted rare earth access. Johari’s framing suggests the deal is invalid as a legal consequence of the ruling, not a Malaysian withdrawal — a key distinction given Trump’s warning of higher duties for countries that back away. The opposition is calling for a special parliamentary session.

Pakistan: The government announced salary cuts of 5–30% for State-Owned Enterprises (SOE) and autonomous institution employees for two months as part of the ongoing austerity drive. Savings go to the new Prime Minister’s Austerity Fund, used to maintain unchanged petrol and diesel prices. The PKR 389bn contingency fund may also be tapped.

Latin America

Argentina: Economy Minister Caputo confirmed the government has identified financing for approximately USD 9bn in upcoming FX bond principal payments through 2027, via local FX bond placements and undisclosed alternatives to be revealed in two to three months. Global bond issuance remains off the table at current spreads. Interest payments will be covered by the primary surplus. The key question is how much 2027 will be pre-financed, given the tension between Caputo’s view that spreads are too high and the reality that 2027 is an election year — and 2025 has already demonstrated how quickly financing windows can close in Argentina under electoral uncertainty.

Brazil: The Monetary Policy Committee (Copom) cut the Selic rate 25bps to 14.75% on 18 March, the first reduction since May 2024 and the formal start of the easing cycle. The decision was unanimous under Governor Galipolo. Critically, forward guidance was left deliberately open, with no committed pace for further cuts. The BCB flagged the Middle East conflict as the dominant uncertainty and raised its own 2026 inflation projection from 3.4% to 3.9%. The 25bp move (rather than the 50bp markets had expected before the Iran war) reflects the tension between a domestic environment that supports easing — 12-month inflation fell to 3.8% in February, activity is slowing, BRL remains resilient — and the external backdrop has shifted sharply. Markets still expect the Selic to reach 12.25% by year-end, but that path assumed a world without a Gulf war. Next meeting is 28–29 April; a 50bp cut becomes the base case if oil retreats, but a pause is possible if the Hormuz crisis deepens.

Chile: The government plans to pass fuel price mechanism changes by decree, bypassing Congress. The current mechanism’s small weekly adjustment band has created a growing gap with import parity at a high fiscal cost. The executive power can modify key parameters by decree, resetting domestic prices higher and cutting the subsidy. This is strategically sound because it avoids forcing allies to absorb political cost in Congress, but it leaves the government alone owning the price spike.

President Kast also announced a broad “national reconstruction” package comprising a corporate tax cut from 27% to 23%, VAT housing exemption for 12 months, capital repatriation, education spending reform (free tuition capped at under-30s), and deregulation. The opposition criticises the wildfire-relief framing as cover for a pro-business agenda. Legislative strategy, timing, and fiscal cost remain unclear.

Mexico: President Sheinbaum presented a new electoral reform after Congress killed her previous constitutional proposal. The new bill targets secondary laws (simple majority — passage virtually certain) but is considerably thinner in scope: budgetary only, with a 15% cut to the Senate budget, state congress caps, and electoral authority salary limits. The structural reforms from the original — changing plurinominal election rules to reduce party leaders’ power — are absent. Financial inspection provisions remain a concern for competition. The judicial election has been confirmed for 2027 as scheduled, contradicting reports of a delay to 2028. A disappointing downgrade from the original ambition, killed by the president’s own allies.

Central and Eastern Europe

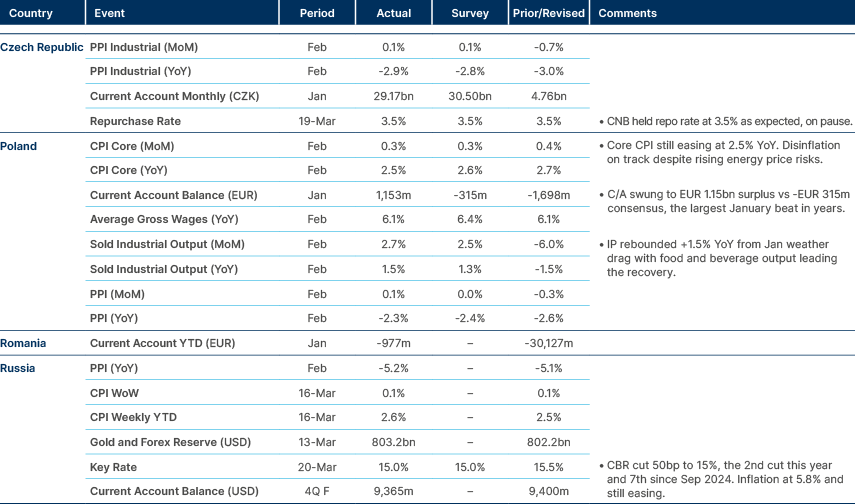

Romania: The OECD published its latest country survey warning Romania must accelerate reforms given its 9.3% of GDP deficit in 2024, which risks placing debt on an unsustainable path. Consolidation packages have been adopted but nothing is specified beyond 2026. The report recommends a broader tax base, spending restraint, performance-based budgeting, digitised tax administration, and market-value property taxation. Low tax compliance, a significant VAT gap, and widespread income under-reporting among low-income groups continue to limit revenue collection.

Ukraine: The next round of US-mediated talks with Russia has been postponed again after Washington rescheduled due to the Middle East conflict and Moscow rejected the proposed US venue. Trump rejected Zelensky’s offer of drone assistance against Iran, saying Zelensky was “far more difficult to make a deal with” than Putin. The diplomatic stalemate is compounded by resource competition: US air defence missiles are now being consumed in the Gulf, weakening Ukraine’s position and potentially forcing territorial concessions in the east.

Middle East and Africa

Egypt: Fitch assessed Egyptian banks as resilient under its baseline scenario (conflict <1 month, oil ~$70/bbl), supported by Net Foreign Assetsat USD 14.5bn as at end of January — the highest since 2012 — and manageable foreign funding at less than 10% of total. However, the pressures are significant: USD 6bn in capital outflows via the EGX since the war began, the EGP down 9% since end February (from 47.03 to 52.26), and interbank USD turnover surging from USD 180mn to USD 1bn per day. Non-resident T-bill holdings of USD 45bn at end September (USD 21bn ex repo) represent a substantial overhang if sentiment deteriorates further.

Morocco: The US is seeking alternative fertiliser sources from Morocco and Venezuela as nitrogen supply via Hormuz has been sharply curtailed, driving prices up more than a third. OCP Group, the state-owned phosphate company, controls over 70% of global phosphate rock reserves and roughly a third of exports, and is expanding into higher-value products. White House adviser Hassett framed the engagement as an “insurance policy” for American farmers.

Qatar: Iran struck Qatar’s Ras Laffan Industrial City on 18 March, causing extensive damage to the Pearl GTL facility. The following morning, further missile attacks hit multiple QatarEnergy Liquefied Natural Gas (LNG) facilities. Ras Laffan supplies approximately 20% of global LNG. Production of LNG, urea, and polymers remains suspended under force majeure, and the North Field Expansion project has been delayed. The strikes were retaliatory following an Israeli attack on Iran’s South Pars field. Qatar expelled Iranian military attachés within 24 hours. Trump warned he would destroy the entire South Pars field if Iran continued attacking Qatar, while signalling Israel would halt further South Pars strikes to prevent additional retaliation.

Turkey: Finance Minister Simsek signalled vigilance as simultaneous Red Sea and Hormuz disruptions tighten global financial conditions. The government convened the financial stability committee immediately; pre-emptive measures limited domestic market stress relative to peers, though bond yields and sovereign risk premia still rose. The CBT introduced lira-settled forward FX sales and the Capital Markets Board curbed speculative equity trading.

The fuel equalisation mechanism caps diesel at TRY 67.10/litre (vs 83.10 without intervention) and gasoline at TRY 62.30 (vs 71.11), but Simsek was candid that the fiscal cost is unsustainable on a permanent basis. Turkey’s regional exposure is substantial: USD 30bn exports, USD 19bn imports, 10mn tourists, and USD 10bn tourism revenue. The disinflation target of below 20% is maintained but the conflict complicates the path materially.

Developed Markets

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.