De-escalatory rhetoric vs escalatory action in the Middle East

- Iran conflict enters fifth week with no confirmed de-escalation despite reports of talks.

- After broad risk-off move, differentiation among emerging market (EM) asset performance has increased.

- Iran has granted selective Hormuz passage to seven nations, including China and India.

- South Korean exports surged 50% yoy in early March, driven by semiconductors.

- India announced a sharp reduction in excise duty on petrol and diesel.

- Indonesia to consider mandatory WFH and online schooling to cut fuel consumption by 20%.

- Bolsonaro Jr leads Lula in a runoff poll for the first time with Lula’s rejection rate rising.

- Colombia’s emergency wealth tax to face court challenge ahead of 1 April deadline.

- Central Bank of Türkiye reportedly preparing gold-FX swaps to defend Lira rather than raising rates.

Last week performance and comments

Global Macro

The Iran conflict has entered a fifth week. Although evidence of diplomatic progress is mounting, no definitive de-escalation is in sight. Talks between the US and Iran, both directly and via third-party emissaries (such ars Pakistan, and Türkiye) are ongoing according to the US and its allies. Iran, however, has not confirmed these talks have taken place and continues to defiantly play down the idea they are willing to cede to US conditions. A two-day meeting in Islamabad of Egyptian, Pakistani, Iraqi and Turkish ministers is currently taking place, in a coordinated regional effort to push for a ceasefire between the US and Iran. Historically, deals between the two have happened more quickly when mediated via third parties, so this is an encouraging signal.

US President Donald Trump and his team continue to assert that the war will be over soon, but markets are increasingly taking these statements with more than a pinch of salt. US Secretary of State Marco Rubio said last week he expects it to last two to four weeks longer. Clearly, this will depend on a deal being made. Over the weekend, Trump claimed Iran had agreed to “most of” a 15-point ceasefire proposal. These points are not public, but are widely understood to entail strict curbs on uranium enrichment, limits on missile production and the total reopening of the Strait of Hormuz – all of which are currently, according to Iranian officials, a red line. Nevertheless, Trump’s bullish rhetoric has again helped stabilise capital markets this morning, even as oil prices have moved higher – with Brent crude back around USD 115 a barrel. S&P 500 futures, MSCI EM futures, copper and gold are all up this morning, with bond yields falling, a reversal of the price action of the last week.

However, if the US plan is indeed to “escalate to deescalate,” as the administration has repeatedly said, we are evidently still in the military escalation phase. Israel struck Iranian energy infrastructure over the weekend, including a nuclear energy powerplant, electricity grid infrastructure, and a ‘deep water’ plant, which would likely have been used for uranium enrichment. In response, Iran struck aluminium facilities in the United Arab Emirates (UAE) and Bahrain, causing significant damage and sending aluminium futures 6% higher. Meanwhile, around 3k further US Special Forces are currently arriving in the Middle East, on top of the current presence of 50k US troops. Analysts suggest that this is not enough for a full-scale ground invasion. Nevertheless, the US military seem to be preparing to carry out special operations of some kind on the land (to remove enriched nuclear material), or landing on islands in and around the Strait of Hormuz and the Gulf, if directed. This readiness is a new point of leverage for the US in negotiations, which it may or may not use. Trump said over the weekend that moving to take Kharg Island – an Iranian oil exporting hub – was still on the table, but an initial move may be to take Qeshm Island in the Strait of Hormuz region. Known as Iran’s ‘unsinkable aircraft carrier’, this island is strategically vital as a base of operations for Iran to control passage through the Strait.

A positive development in recent days – which may be the main reason for market stability this Monday – has been Iran’s statement that five “non-hostile” countries may pass the Strait of Hormuz: China, Russia, India, Iraq and Pakistan. On request, this status has now been extended to Malaysia and South Korea. Trump described Iran’s permission for 10 Pakistani ships to pass as “a present” and a signal of goodwill. Trump also reported that another 20 ships have been added. Safe passage would only be allowed after prior coordination with Iran, likely with a cap on the number of ships which could pass daily. Large oil tankers can carry up to 2m barrels each. With around 8m barrels a day currently offline, net of Strategic Petroleum Reserve (SPR) releases, just two further cargo ships passing a day could, in theory, cut the deficit in half, according to Bloomberg Energy and Commodities Analyst Javier Blas, which is meaningful.1 However, a key risk that must be considered is disruption to Red Sea shipping now the Houthis have got more involved in the conflict, firing missiles at Israel over the weekend.

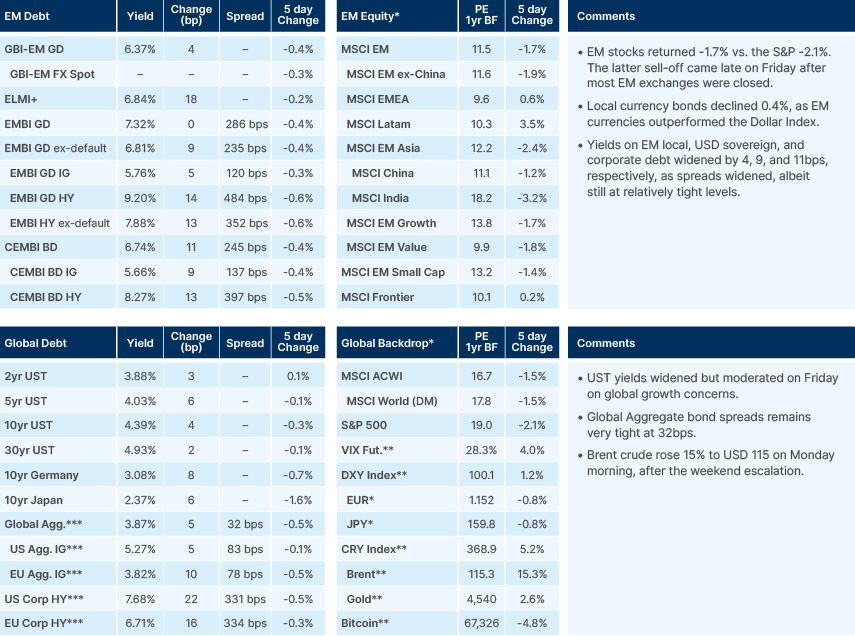

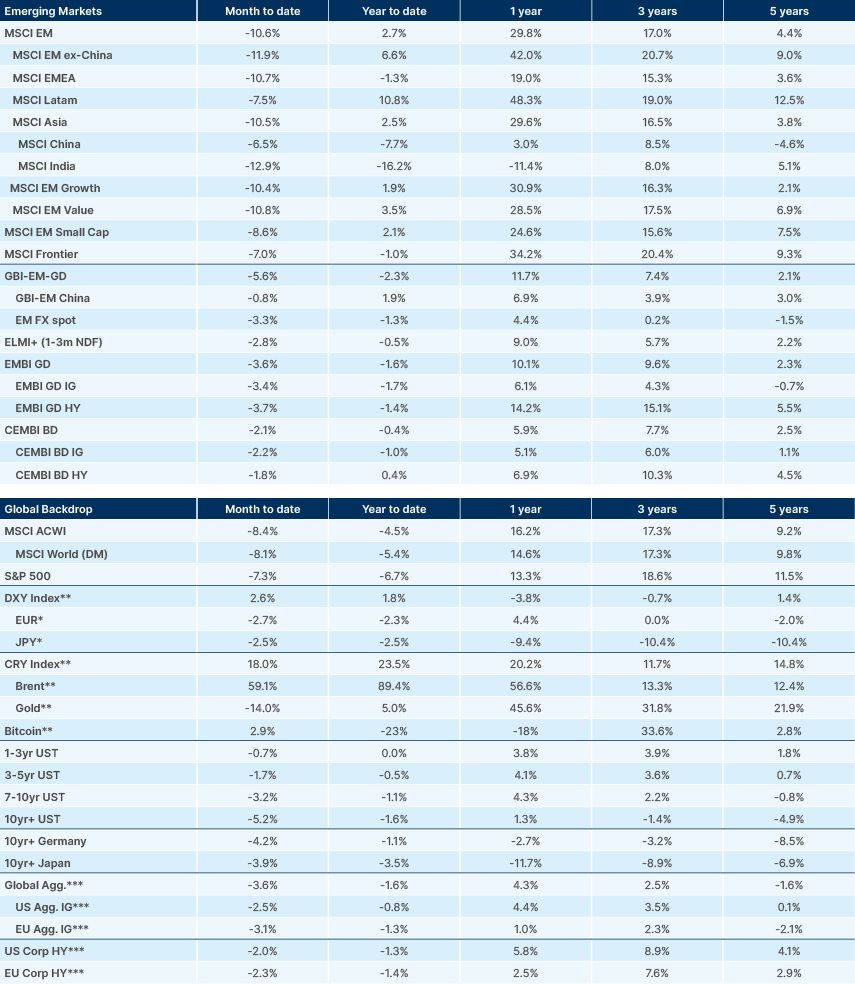

EM asset values declined last week, but the underperformance relative to developed market (DM) assets has now moderated. The MSCI EM Index is down around 10.5% month-to-date (MTD), relative to 8.1% for MSCI World. After an initial broad sell-off, differentiation is increasing among oil importing countries more exposed to high oil prices, such as India, and those less exposed, such as Brazil, Mexico and China. EM local currency bonds are down 5.6% so far this month, due to the combination of dollar strength and higher rates. The EMBI GD is down 3.6%, in line with the Global Aggregate Index. Spread widening has been contained so far, with EMBI GD spreads widening just 27 basis points (bps) MTD and 40bps from its lows to 286bps, even as spreads entered the crisis at historically compressed levels after years of strong technicals and crossover demand.

In our view, the modest reaction is because the current shock is oil specific, not systemic. So far there has been no banking contagion or Dollar funding stress. EM companies entered 2026 with low leverage and high coverage. Under the hood, as with equities, there is expected differentiation among oil importers with weaker balance sheets and oil exporters, for example Egypt +44bps, Türkiye +36bps, and Angola -39bps. But the limited move in index-level spreads tells us two things: first, the market is still pricing a short war consistent with a base case of 30- to 60-day disruption to oil flows, rather than a multiple month scenario. Second, the milder price action highlights the ‘Goldilocks’ global macro environment wherein the current shock happened, with stable growth, falling inflation and positive real interest rates across DM (and some EM countries). This is a far cry from 2022, when inflation was surging, as real policy rates were deeply negative and quantitative easing was in full flow amid enormous post-pandemic fiscal expansion. When this fiscal and monetary excess was met with a supply shock, it forced central banks to hike rates rapidly to deal with runaway inflation. Labour markets were also tight, which led to goods inflation quickly passing through into wages – another dynamic unlikely to take place this year given weaker labour demand in DM and EM alike, as well as strong deflationary impulses still emanating from Chinese exports.

Emerging Markets

Asia

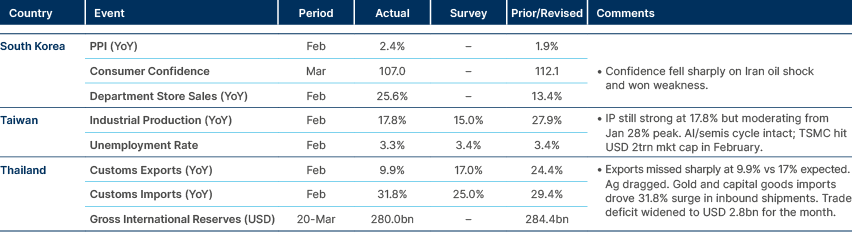

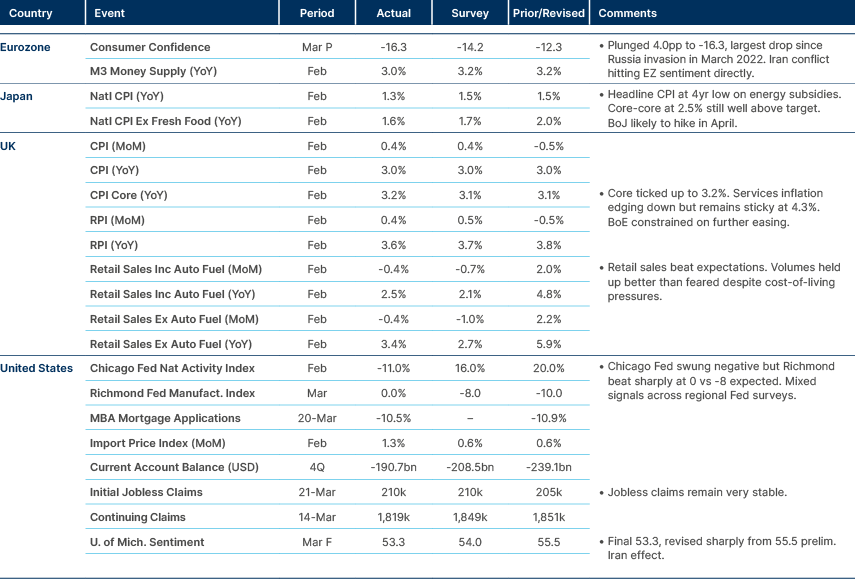

Korea confidence down but remains elevated. Taiwan production surprised higher.

India: Iran listed India among five friendly nations permitted safe passage through the Strait of Hormuz, alongside Russia, China, Iraq, and Pakistan. The move is expected to ease the severe liquified petroleum gas (LPG) crisis triggered by the Hormuz blockade. In FY25, India consumed 31.3m metric tonnes of LPG, of which approximately two-thirds was imported, with around 90% of imports sourced from the Middle East. The Indian government had previously cut LPG supplies to commercial users such as hotels and restaurants to prioritise household consumption.

Separately, the government retained its 4% consumer price index (CPI) inflation target with a +/-2% tolerance band for another five years to March 2031. The decision was taken in consultation with the Reserve Bank of India (RBI) and signals continuity of the flexible inflation-targeting framework adopted in 2016. CPI inflation stood at 3.2% yoy in February, up from 2.8% in January. Higher oil prices and supply disruptions are expected to push inflation above 4% in the coming quarters. The RBI held its repo rate at 5.25% in February after cumulative cuts of 125bps since early 2025. The next policy meeting is scheduled for 6-8 April.

Indonesia: The government is considering mandatory work-from-home one day per week and online schooling to reduce fuel consumption, measures previously used during the COVID-19 pandemic. Economic Minister Airlangga Hartarto said the measures could cut fuel consumption by 20%. Indonesia reportedly has 25-30 days of fuel reserves and is working to procure Russian oil as Hormuz shipments remain disrupted.

Malaysia: Iran allowed passage of Malaysian tankers through the Strait of Hormuz after Prime Minister Anwar Ibrahim spoke directly with Iranian President Masoud Pezeshkian. Malaysia is working to release stranded tankers and repatriate workers. Anwar expressed a firm stance against what he called US and Israeli aggression, while noting the situation had become more complex as Iran's response affects Gulf countries beyond Israel. He warned food supplies will be disrupted and prices will rise, but said Malaysia remained in a relatively better position due to Petronas's energy supply management capability.

Malaysia’s Domestic Trade Minister Armizan Mohd Ali confirmed no shortages of petrol, diesel, or LPG have been reported, with supply more stable than in neighbouring countries. However, the risk of subsidy leakage is increasing as the price gap with neighbours widens due to the conflict. Despite being a net energy exporter, Malaysia imports most of its crude oil and its refineries are calibrated for heavy Middle Eastern grades. The government is exploring alternative crude sources from Australia and Asia Pacific.

Pakistan: The government increased the petroleum levy on high-octane fuel (RON97) by PKR 200/litre to PKR 300/litre, a 200% increase. The higher levy is expected to generate PKR 9bn per month, which will fund subsidies for lower- and middle-income groups. Prime Minister Shehbaz Sharif said the premium fuel is primarily used in expensive vehicles and the move would not affect public transport fares or air travel costs. The government continues to maintain prices on RON95 petrol and high-speed diesel despite rising global oil prices. The fuel levy hike sits within a broader austerity package including 50% cuts to fuel allowances for official vehicles, salary cuts for some officials, and a four-day public sector work week. The government signalled a shift toward targeted subsidies.

South Korea: Exports surged 50.4% yoy to USD 53.3bn in the first 20 days of March. Adjusted for working days, growth was 40.4% yoy. The trade surplus widened sharply to USD 12.1bn from USD 1.1bn a year earlier. Semiconductor exports more than doubled to USD 18.7bn, driven by higher chip prices and strong high bandwidth memory (HBM) demand. Computer peripheral exports tripled to USD 2.2bn, while petroleum products rose 49.0% on war-driven fuel prices. By destination, China (+69%) and the US (+58%) led, while EU exports lagged at 6.6%. Car exports rose a modest 11.1% and ship exports fell 3.9%.

SK Hynix announced the purchase of extreme ultraviolet (EUV) equipment from ASML worth KRW 12trn (USD 8bn), likely covering around 20 scanners delivered over the next two years. The deal would double SK Hynix's EUV capacity and narrow the gap with Samsung Electronics, which holds around 60 machines. It represents approximately 25% of ASML's 2025 projected revenue. Separately, SK Hynix plans to issue USD 8bn in new shares (2.4% of total) for listing as American Depository Receipts (ADRs) in the US, with proceeds earmarked for HBM fab expansion. The issuance effectively reverses the KRW 12.2trn treasury stock cancellation completed last month.

The government nominated Bank for International Settlements (BIS) Monetary and Economic Department Head Shin Hyun-song as the next Bank of Korea Governor, replacing Rhee Chang-yong whose term expires in April. Shin is considered a leading expert in financial stability and macroprudential policy, known for predicting the 2008 Global Financial Crisis at an International Monetary Fund (IMF) meeting in 2006. His appointment signals continuity, but he inherits a difficult mandate of rising oil-driven inflation, a weakening Won, and an unstable property market.

Iran's ambassador offered conditional safe passage through the Strait to South Korean vessels, describing the country as non-hostile, though the Ministry of Foreign Affairs denied any bilateral discussions on vessel coordination. South Korea has 26 vessels stranded at the Strait with 179 Korean crew members. The government predicted no major oil supply disruptions in April, citing secured alternative shipments and planned strategic reserve releases, though it acknowledged imports would fall below usual levels. Dubai crude reached USD 158/bbl.

Latin America

Brazil and Mexico inflation surprised to upside ahead of oil shock.

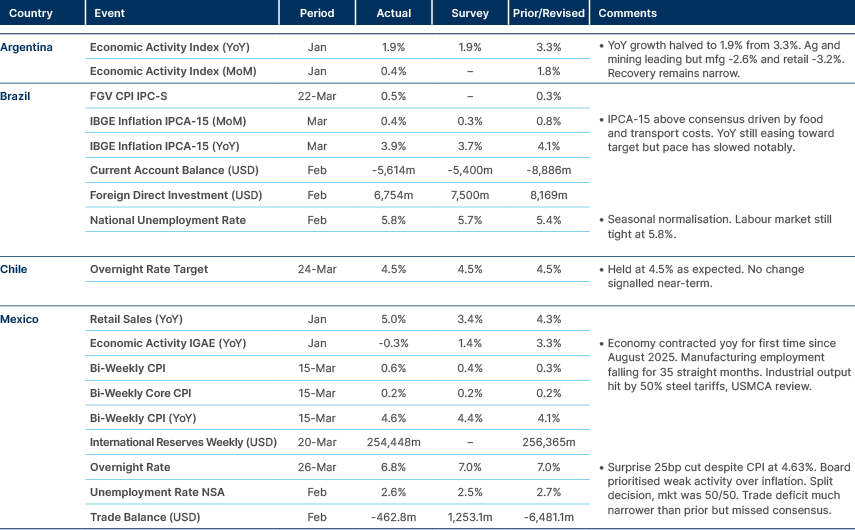

Argentina: Economy Minister Luis Caputo confirmed at a finance event that the government has identified financing sources to cover approximately USD 9bn in upcoming FX bond principal payments due in July 2026 and January 2027. payments will be covered by the primary fiscal surplus. Caputo indicated the financing mix includes FX bond placements in the local market and other alternatives to be revealed in two to three months, while dismissing the option of a global bond issuance at current borrowing costs.

The government has demonstrated a strong ability to procure alternative financing, and there is little doubt at this point that 2027 maturities can be covered without a global bond. However, the key question is how much 2027 will be pre-financed, given the tension between Caputo’s view that spreads are too high and the reality that 2027 is a general election year — and 2025 has already demonstrated how asymmetric electoral risk can close financing windows in Argentina.

Brazil: President Lula continues to lead all first-round scenarios ahead of the October election, but he would likely lose to Flavio Bolsonaro in a potential runoff, according to an 18-23 March Atlas survey. This is the first time since the announcement of Flavio's candidacy that Lula has trailed in a runoff poll. In the second round, Flavio led with 47.6% (up from 46.3% in February) versus Lula's 46.6% (up from 46.2%). Lula's approval fell to 45.6% from 46.6% in February, while his disapproval rose to 53.5% from 51.5%.

The shift follows a sharp rise in Lula's rejection rate to 52.0% (from 48.2% in February), while Flavio's rejection remains broadly stable at 46.1%. This supports the expectation that the election will be a rejection battle. Renan Santos of the right-wing Mission Party appears in third place in most first-round scenarios, drawing stronger support among 16-24 year olds, partly through vocal commentary on the Banco Master case. His supporters would likely move toward Flavio in a runoff. Although the polls point to a more challenging path for Lula's re-election, official campaigning has not yet begun and it is too early to conclude he has lost front-runner status. The outlook points to a highly polarised election with the possibility of an upset.

Colombia: The National Business Council formally requested the Constitutional Court to urgently suspend the emergency wealth tax created through Legislative Decree 173. The tax applies to legal entities with net equity above COP 10.5trn, with the first 50% instalment due on 1 April. Council President Natalia Gutierrez warned that if the Court does not intervene before the deadline, the country could enter unprecedented economic deterioration. She argued the government appears to be using the climate emergency to cover a COP 16.3trn fiscal shortfall, without first exhausting spending austerity. The 1.6% surcharge for financial and extractive sectors is being read in the business community as a selective penalty on capital-intensive activities. The Court's delay in ruling on whether the economic emergency is legal means collection would proceed under high legal uncertainty with mass litigation likely.

In the presidential race, the CNC poll for Cambio magazine shows Iván Cepeda leading the first round at 34.5%, followed by Paloma Valencia at 22.2% and Abelardo de la Espriella at 15.4%. Valencia has consolidated significant momentum since the primaries, rising 18pp. In a runoff, Cepeda and Valencia are in a statistical tie at 43.3% vs 42.9% (3% margin of error), making her the only candidate capable of competing with Cepeda head-to-head. De la Espriella appears to be suffering a trajectory similar to Vicky Davila's, where an initially expected front-runner fades. His refusal to form alliances may be costing him, though the Uribist right (generally over-35, upper-middle-class, Catholic) may still prefer him over Valencia in the first round given her running mate Juan Daniel Oviedo's progressive social positions. The high percentage of undecided voters (8% DK/NA) suggests the race remains open.

Central and Eastern Europe

Hungary kept policy rate at 6.25% as expected.

Ukraine: President Volodymyr Zelenskyy said Russian President Vladimir Putin does not want to end the war, summing up the Ukraine-US talks in Florida. He warned against rewarding the aggressor, suggesting the US side pushed Ukraine to accept Russian conditions, principally the surrender of remaining Donetsk territory. Security Council Secretary Rustem Umerov said US security guarantees and prisoner exchanges were discussed, though both topics have been on the table for months. Zelenskyy admitted the US was focused on the Iran war.

Central Asia, Middle East, and Africa

Türkiye Tourism arrivals below 2025 levels.

Morocco: The adequacy of Morocco's fuel stocks has come under renewed scrutiny. The Ministry of Energy stated in early February that national stocks exceeded 617k tonnes, with over 1m tonnes in transit, covering around 30 days including incoming shipments. However, no new figures have been released since the late February escalation. Total storage capacity stands at approximately 1.56m tonnes (45-60 days of consumption theoretically), but actual stock levels are significantly lower. Industry analysts suggest inventories have at times fallen to around 167k tonnes. Morocco's legal requirement of 60 days of strategic reserves remains unmet.

Saudi Arabia: Aramco lowered crude shipments to Asia for the second consecutive month for April, supplying only Arab Light through the Red Sea port of Yanbu. According to Kpler, Saudi crude exports fell 40% to 4.4 million barrels per day (mbpd) in March from the Q1 average of 7.1mbpd. Following the effective closure of the Hormuz Strait, Aramco has rerouted crude via the 5mbpd East-West pipeline, with capacity temporarily boostable to 7mbpd. Export volumes are expected to recover next month, but both the Saudi oil infrastructure and the Bab el-Mandeb route remain vulnerable to attacks.

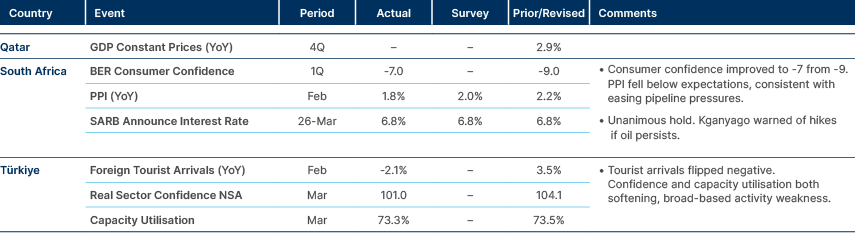

Türkiye: The Central Bank of Türkiye (CBT) was reportedly preparing to deploy gold reserves to support the Lira through gold-FX swap transactions on the London market, according to Bloomberg. JPMorgan economist Fatih Akcelik noted that roughly USD 30bn of Türkiye’s gold reserves are held at the Bank of England, allowing rapid mobilisation without logistical delays. Türkiye’s gold reserves reached approximately USD 135bn as of early March. The CBT's conventional FX reserves stood near USD 48bn as of 12 March, with approximately USD 12bn in non-SDR basket currencies, limiting the readily usable stock.

Developed Markets

UK CPI inflation in line with expectations, Gilt underperformance continues.

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. See https://x.com/JavierBlas/status/2038182738105135318?s=20