- Brent crude breached USD 100/bbl as Middle East conflict escalated further.

- Iran elects Mojtaba Khamenei as new Supreme Leader.

- US payrolls printed -92k, well below consensus of +55k.

- China’s 15th Five-Year Plan doubles down on productivity, no pivot toward consumption.

- Fitch cut Indonesia’s outlook to negative, in line with Moody’s.

- Argentina’s sweeping labour reforms ratified by Senate.

- Poland cuts rates by 25bps to 3.75%, despite Middle East inflation risks.

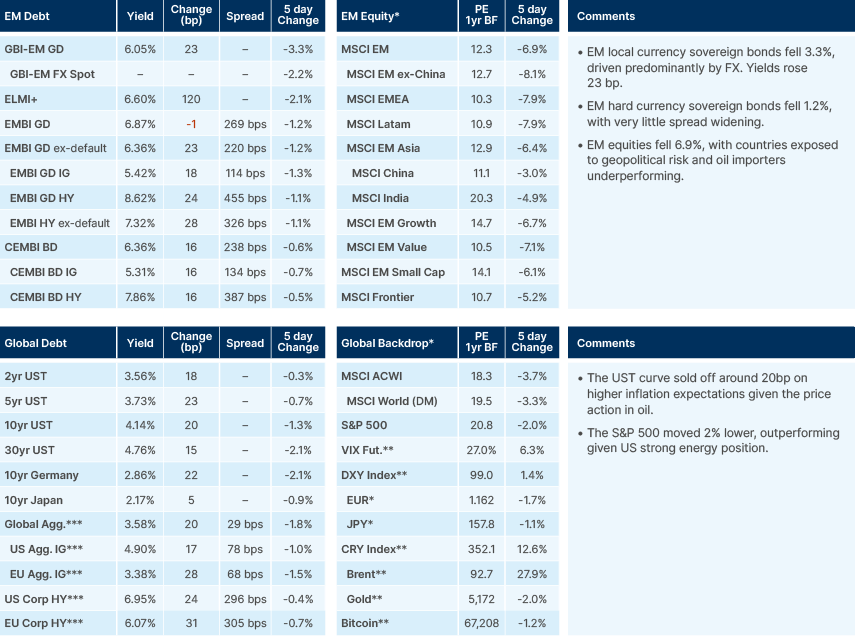

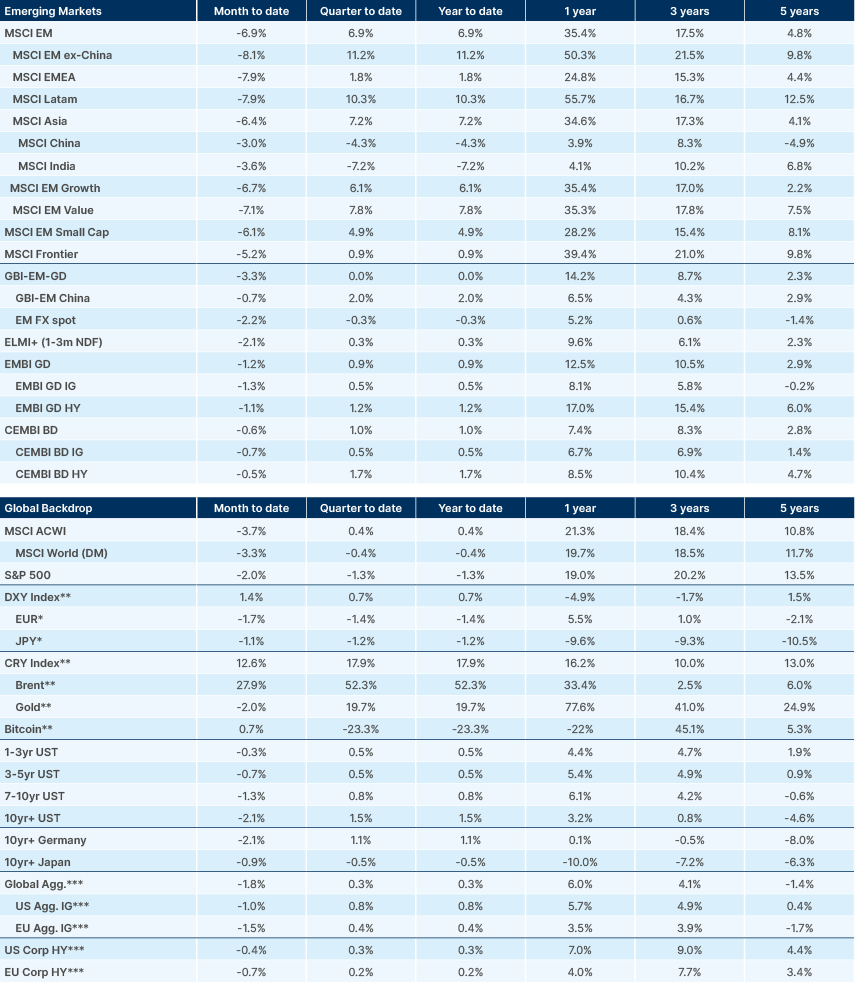

Last week performance and comments

Global Macro

Brent crude rose above USD 100 per barrel this week for the first time since early 2022, driven by continued escalation of the Middle East conflict. Over the weekend, Iran’s Assembly of Experts elected Mojtaba Khamenei, the late Supreme Leader’s son, as his successor. Mojtaba Khamenei has no prior government experience and is not well known publicly, though he is understood to have strong ties to the Islamic Revolutionary Guard Corps (IRGC), having served with the unit during the Iran–Iraq war in the 1980s. The IRGC were likely instrumental in his selection. US President Donald Trump described him as a “lightweight” and called his leadership “unacceptable”, saying the US wants “someone that will bring harmony and peace to Iran.”

Despite a stated commitment from the Iranian President to cease offensive strikes on non-military assets in the Gulf, Iran has continued to target energy infrastructure in the region and has now begun striking water desalination plants along the Persian Gulf coastline. This reflects the limited authority the Iranian President has over military operations, which sit under the Supreme Leader and the IRGC. In the near term, escalation looks more likely than de-escalation. Markets have begun to differentiate between winners and losers from a potentially prolonged period of elevated oil prices, following relatively broad selling of risk assets last week. Assets that had outperformed year-to-date generally saw the sharpest pullbacks, including emerging market (EM) equities (particularly ex-China) and EM local currency bonds. In contrast, the S&P 500 is down just 2%, partly reflecting the US’s status as a net energy exporter and its relative insulation from higher oil prices. That said, the limited drawdown in US equities also suggests markets have not yet experienced a full-scale volatility shock, and we would continue to counsel a defensive posture.

G7 countries are set to release strategic petroleum reserves, with Japan and South Korea also likely to draw down stockpiles, which may provide some near-term price stability. However, for energy markets and the broader global economy, the key source of pressure is not necessarily crude prices alone but the cost of refined products, gasoline, diesel and critical inputs such as fertiliser, where pass-through to end consumers and supply chains is more direct and harder to offset through reserve releases.

EM carry trades have come under significant pressure since the escalation in the Middle East. According to Bank of America Merryl Lynch (BAML)estimates, Türkiye and Egypt have seen the brunt of outflows thus far. While other EM carry trades also saw de-risking, the scale appears to have been smaller relative to the total position outstanding in the Brazilian real and Mexican peso. Notably, investors have been quicker to discuss the possibility of re-entering Brazil on weakness than other markets, reflecting its relative insulation as a commodity exporter and the near-term prospect of monetary easing.

More broadly, the dependence on imported energy that has weighed on core Europe, Egypt and Türkiye has also pressured Central and Eastern European markets. The pattern across markets is as expected, net energy importers with large external financing needs are most vulnerable, while commodity exporters and countries with credible macro frameworks have seen more orderly price action.

EU gas storage levels have fallen to critical levels and are now only marginally above those seen in 2022, prior to the sharp spike in prices that summer. As at 18 February, aggregate EU storage stood at just 32%, roughly half the five-year average for this date. Among the larger economies, Germany was at 21.6%, France at 22.5%, the Netherlands at just 13.1% and Italy at 49.7%. EU-wide storage is now approaching 30%, with the Netherlands close to 10%.

While these levels are concerning and warrant close monitoring, it is important to note that this is not yet a repeat of the 2022 energy crisis. Natural gas prices have doubled, but in 2022 they increased ten-fold. Since then, European governments and utilities have diversified supply, liquified natural gas (LNG) import capacity has expanded materially, and demand-side flexibility has improved. That said, a sustained Middle East-driven disruption to LNG shipping, particularly through the Strait of Hormuz, would meaningfully alter the supply outlook heading into the restocking season. The risk is not imminent, but it is non-trivial if the conflict persists through the summer months.

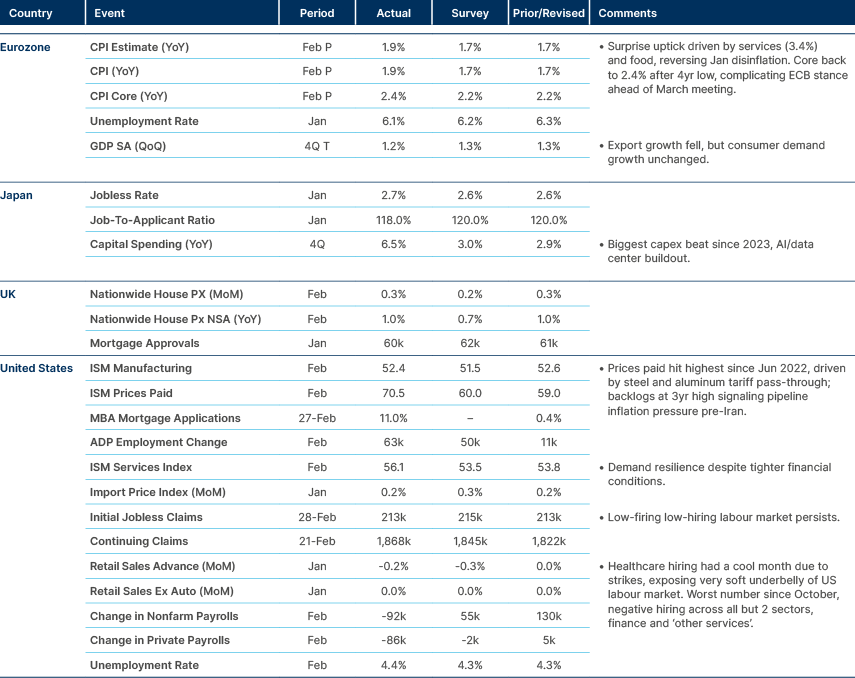

Friday’s US non-farm payrolls report was notably weak, printing at -92,000 against a consensus expectation of +55,000. The six-month moving average has now fallen to -1,000. Private payrolls declined 86,000 and the prior two months saw net downward revisions of 69,000. Healthcare sector strikes accounted for a portion of the headline miss, but the underlying trend points to further softening in the labour market. The data are consistent with a cooling economy and reinforce expectations that the US Federal Reserve (Fed) will be in a position to cut rates in the coming months, though the inflationary impulse from higher energy prices complicates the near-term picture.

China’s latest Five-Year Plan contained little to no emphasis on rebalancing the economy toward consumption. Instead, the focus remains firmly on productivity gains and supply-side upgrading. The Ministry of Finance signalled a highly disciplined approach to fiscal spending, stating there would be no “penny” allocated to any project without a demonstrably high return on equity. For EM investors, the implication is that the hoped-for demand-side stimulus remains unlikely, and China’s growth contribution to the rest of the emerging world will continue to come primarily through trade competitiveness rather than import demand.

Emerging Markets

Asia

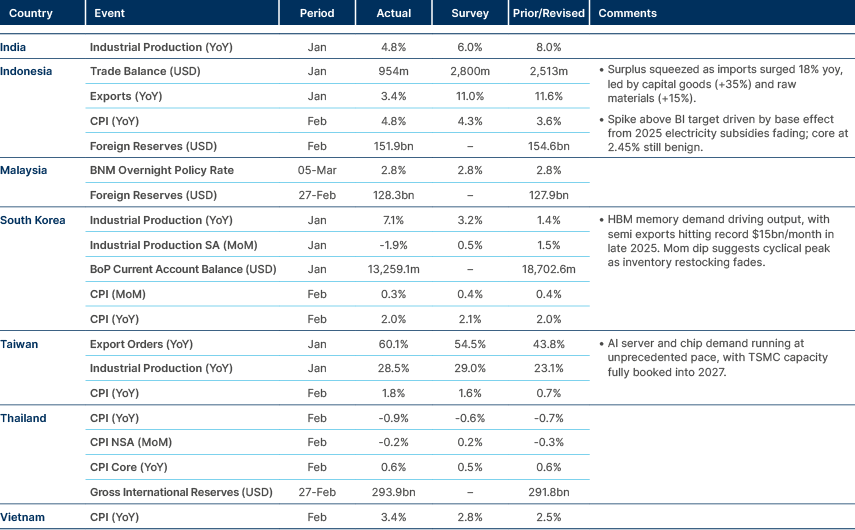

Inflation remains subdued in Asia ahead of Iran shock.

India: The US granted India a temporary 30-day waiver allowing refiners to complete purchases of Russian crude loaded before 5 March. The exemption provides near-term supply relief as global oil markets tighten amid the escalation in West Asia. India imports roughly 90% of its crude requirements, consuming around 5.5m barrels per day (mbpd). Russian shipments had already fallen to 1.0mbpd in February from close to 2.0mbpd in mid-2024, as sanctions risks intensified. Washington signalled it expects India to increase purchases of US crude as part of broader energy cooperation. A sustained conflict around the Strait of Hormuz, through which roughly half of India’s crude and over half of its LNG passes, poses material risks to the current account deficit, inflation and fiscal management via higher subsidy costs.

Indonesia: Fitch cut Indonesia’s outlook to negative from stable, keeping the ‘BBB’ rating, mirroring Moody’s earlier action. The revision reflects growing policy uncertainty, centralisation of decision-making and concerns over fiscal slippage. Fitch expects the fiscal deficit to reach 2.9% of GDP in 2026, above the government’s 2.7% target, but still within the 3% legal ceiling. The agency projects Bank Indonesia will cut rates by a cumulative 50 basis points (bps) to 4.25% this year, though it flagged risks to the Bank Indonesia’s inflation targeting mandate, as the central bank increasingly focuses on GDP growth and Rupiah stability. Governor Perry Warjiyo maintained his GDP growth forecast of 4.9–5.7% and noted that forex reserves cover 6.1 months of imports. Separately, the Finance Minister assured that the budget can absorb oil prices up to USD 92/bbl, with fiscal space to react, though Indonesia’s status as a net oil importer means higher prices will pressure the trade surplus.

South Korea: Authorities secured more than 8m additional barrels of Middle Eastern crude through emergency measures. The UAE committed 6m barrels from a port that does not require Strait of Hormuz transit, plus 2m from a joint reserve stored domestically. A further 2m barrels of Kuwaiti oil were also procured. The Middle East supplies over 70% of Korea’s crude and 20% of its natural gas. Current reserves cover over 200 days. The semiconductor industry raised concerns that a prolonged conflict could disrupt supplies of critical inputs: South Korea is 97% dependent on Israeli imports of bromine gas, used in chip fabrication, while nearly two-thirds of helium, essential for cooling, is sourced from Qatar. Higher LNG prices also threaten electricity costs given gas accounts for 25–30% of Korea’s power mix. SK Hynix said its helium inventories are sufficient and it does not expect disruptions. Samsung declined to comment.

Latin America

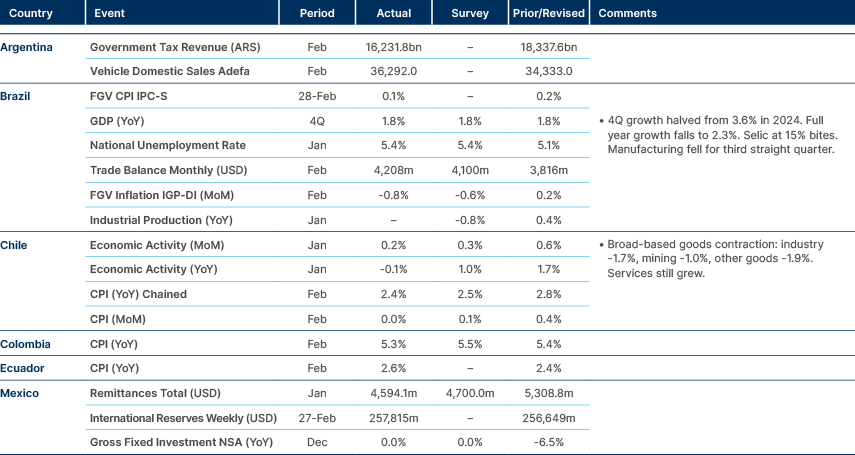

Argentina: The Senate ratified the government’s sweeping labour reform, clearing it for presidential signature. The bill’s 190-plus articles aim to increase labour market flexibility, reduce costs and litigation, and curb union power. Key measures include dynamic wage components in collective agreements, extended working-hour flexibility, a new unemployment insurance fund, and restrictions on strike rights. Two proposals were dropped: a 3pp corporate income tax cut was withdrawn after provincial resistance, and a 1pp reduction in social security contributions was removed. The final vote passed 42–28 without significant protests.

President Javier Milei opened the congressional session pledging a reform package every month for nine months, covering customs, taxes, the electoral system, judicial reform and education, though concrete details were scarce. Separately, Economy Minister Luis Caputo dismissed calls to issue a global bond, arguing sovereign spreads, currently above 500bps, are elevated due to political risk rather than lack of market access. He said fundamentals warrant spreads of 250–300bps and that the government is pursuing alternative financing at lower cost. Argentina’s FXreserve accumulation is running above target, with FX purchases at roughly 30% of market volume versus a 5% initial goal.

Brazil: GDP grew 1.8% yoy in Q4, matching consensus and the Q3 pace. On a seasonally-adjusted basis, output edged up 0.1% qoq. Full-year growth slowed to 2.3% from 3.4% in 2024, in line with government and Central Bank of Brazil (BCB) forecasts, as monetary tightening weighed. Agriculture was the standout, expanding 11.7% in 2025 after a record harvest, while investment fell 3.1% yoy in Q4, its first decline since Q4 2023. Exports grew 14.2% yoy in Q4, suggesting some success in market diversification despite US tariffs. For 2026, the BCB forecasts growth slowing to 1.6%, while the government targets 2.3%.

Finance Minister Fernando Haddad said the Middle East conflict is unlikely to derail a Selic cut in March, though its longer-term impact will depend on how the situation evolves. The Monetary Policy Committee (Copom) is widely expected to begin its easing cycle with a 50bp cut on 17–18 March, taking the Selic to 14.50%. Treasury Secretary Rogerio Ceron indicated any geopolitical spillover would more likely affect expectations for the length of the cycle rather than the initial move.

Colombia: Historic Pact Senator Iván Cepeda has extended his lead ahead of the 2026 presidential election. The CNC/Cambio poll puts him at 35.4% in the first round, up from 28.2% in January, with Abelardo de la Espriella at 16.7%. In all runoff scenarios, Cepeda wins with over 50%. The larger AtlasIntel/Semana survey shows a tighter race in round one (39.8% vs 35.6%), with De la Espriella edging Cepeda by 39.1% to 38.9% in a runoff, though that gap has narrowed. Polymarket assigns Cepeda a 63% probability of winning the first round and 53% for the presidency.

Central government net debt edged down to 58.5% of GDP in 2025, a 0.5pp decline, while gross debt rose 3.1pp to 64.4%. The divergence stems from a 3.6pp increase in liquid assets driven largely by collateral requirements for the Total Return Swap structured in September 2025. The Finance Ministry executed aggressive liability management operations, reducing nominal debt by COP 25.7trn through bond swaps and buybacks. However, analysts note the primary deficit was the highest in two decades and that the strategy effectively postpones interest costs to future years. The technical reporting standards (TRS) position remains opaque, with questions about whether it was hedged against CHF appreciation.

Mexico: Banxico is expected to cut its policy rate by 25bps to 6.75% at the 26 March meeting. Analyst consensus has shifted forward from May following a dovish quarterly report presentation, where Governor Victoria Rodríguez minimised lingering inflation pressures and the board indicated no second-order effects from the late-2025 tax hike. A 4–1 vote is anticipated, with Deputy Governor Jonathan Heath as the sole dissenter. Consumer price index (CPI) inflation stood at 3.9% yoy at February H1, with food, beverages and tobacco accelerating to 6.3%. The market consensus still expects only 50bps of total easing in 2026, with a terminal rate of 6.50%, though the board’s dovish tilt may allow cuts beyond that.

The government began formal bilateral USMCA revision talks with the US, with the first round set for 16 March, ahead of planned trilateral discussions including Canada. The decision to proceed without Canada initially is noteworthy given both Mexican and Canadian insistence on preserving the trilateral format. Goals include cutting import dependency on non-regional sources, strengthening rules of origin and securing supply chains.

The public sector posted a MXN 59.4bn primary surplus in January, down from MXN 103.7bn a year earlier. Revenues grew 10.2% yoy in real terms, with tax revenues up 11.5% and oil revenues up 11.8%. Spending jumped 12.3% yoy, driven by current expenditure, despite sharp falls in financial costs and capital spending. President Claudia Sheinbaum’s approval rating rose to 72% in February, boosted by the operation in which CJNG cartel leader El Mencho was killed.

Central and Eastern Europe

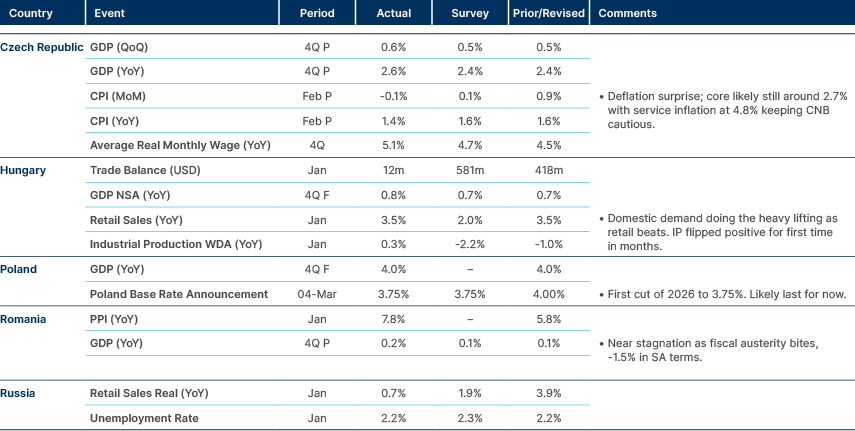

Activity in Czech and Hungary well supported. Poland cut as expected.

Czech Republic: Industry Minister Karel Havlíček signalled the government is prepared to intervene in the energy market with a price support scheme more generous than that of 2022–2023, should gas prices spike further. He offered no specifics, but indicated the government is in contact with energy suppliers and will not allow household energy bills to soar. On the regulatory front, Havlíček said the government is working to revise ETS1, targeting emission allowances at around EUR 30/tonne, down from the current level above EUR 80. Plans to buy out the remaining 30% minority stake in CEZ are being finalised, with the goal of using the fully state-owned utility to regulate energy prices. The buyout is expected in 2027. The fiscal implications of a large price support scheme are notable, given this administration has no plans for significant consolidation afterwards.

Kazakhstan: The National Bank of Kazakhstan (NBK) held its base rate at 18%, citing elevated monthly price growth despite a slight moderation in annual terms. The central bank revised its year-end inflation forecast to 9.5–11.5% from 9.5–12.5%, seeing limited pressure from the VAT hike and noting tighter monetary conditions, lower credit growth and exchange rate dynamics as disinflationary factors. The GDP growth forecast was unchanged at 3.5–4.5%, with the Brent price assumption revised up to USD 66.3/bbl from USD 60. The NBK sees no scope for easing at present, but flagged possible rate cuts in H2. The next rate-setting meeting is 24 April. Separately, Kazakhstan’s debut panda bond sale could take place as early as April, according to Bloomberg, with an expected volume of USD 300–400m. The government also plans USD 1.5bn in eurobond issuance this summer, though Middle East tensions could affect the timeline.

Poland: The MPC cut its reference rate by 25bps to 3.75%, bringing the cumulative easing since May 2025 to 200bps. The move came despite inflation risks from the US–Israel strikes on Iran, which weakened the Zloty and pushed up gas and fuel prices. The updated central bank (NBP) projection showed inflation mid-points of 2.25% for 2026 and 2.40% for 2027, both below the 2.5% target, with a new 2028 forecast of 2.45%. GDP growth projections were raised to 3.90% for 2026 and 2.90% for 2027. The data cutoff of 19 February meant the conflict’s impact was not formally incorporated, but the MPC judged the outlook benign enough to proceed. A “marked” slowdown in January wage growth likely helped. Nearly all members have signalled cutting to 3.50% by end-H1, though the inflation basket reweighting on 13 March and the trajectory of the Middle East conflict could delay further moves.

Romania: The Treasury plans to raise at least RON 8bn through local bond auctions in March, comprising 13 regular placements and one T-bill issue. Overall borrowing by end-February covered 22.6% of gross financing needs, which are estimated at RON 265–275bn for 2026, driven by a projected 6.2%-of-GDP budget deficit and a peak in maturing debt. Around 60% of needs will be sourced domestically. The external funding target stands at EUR 21bn, with EUR 10bn from foreign bond issuance. January saw the highest monthly local borrowing on record at nearly RON 15.2bn, as the Treasury continued to benefit from falling borrowing costs.

Middle East and Africa

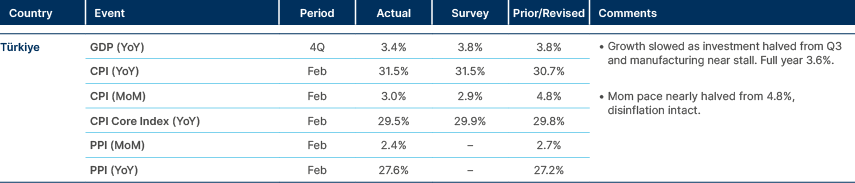

Softer growth in Türkiye.

Angola: Sonangol is negotiating a USD 4.8bn loan from Chinese lenders to close the funding gap on the 200,000bpd Lobito refinery, with a delegation set to visit Beijing in April. Crucially, the financing will not be backed by oil shipments, marking a shift from the resource-backed lending model Angola used heavily with China before 2017. Construction is roughly one-quarter complete, with commercial operation targeted for 2027. Lobito would become Angola’s largest refining facility, more than triple the capacity of the Luanda and Cabinda plants. Despite being Africa’s second-largest oil producer, Angola currently imports 80% of its fuel needs.

Egypt: The US–Israeli military operation against Iran has created acute risks for Egypt’s fragile economic recovery. The Suez Canal, already weakened by Houthi disruptions, faces a further chilling effect if Strait of Hormuz obstruction drives up Red Sea insurance premiums. As a net importer of refined petroleum and a major wheat importer, Egypt is exposed to both higher energy costs and rising food prices via disrupted global shipping. Capital flight from Egyptian treasury bills could force the Central Bank of Egypt to pause or reverse its easing cycle. Tourism, which had been on a strong upward trajectory, is expected to decline. Cairo may need to seek further emergency credit lines from international institutions and Gulf partners.

Saudi Arabia: Aramco is rerouting crude exports to the Red Sea via the East–West Pipeline to bypass the Strait of Hormuz, though capacity is limited to around 5mbpd, temporarily boostable to 7m, against average exports of 7.2mbpd in Q1. A more immediate problem is storage: four of six tanks at Ras Tanura are full, and Ju’aymah is also near capacity, giving roughly 20 days before production shutdowns would be required. Egypt has offered to facilitate onward transport via the Sumed pipeline to the Mediterranean, which has 2.5mbpd capacity. Iran’s retaliatory strikes hit energy infrastructure near Ras Tanura and targeted every Gulf state. While elevated oil prices might appear positive for Saudi revenues, the net benefit is limited once risk premia, higher shipping costs and increased defence spending are factored in. The government will likely delay some giga-projects, though these are mainly PIF-financed. More broadly, the conflict has exposed the vulnerability of Vision 2030’s assumptions around regional security, potentially deterring foreign investment and skilled expat workers.

Sub-Saharan Africa: An International Monetary Fund (IMF) paper found that SSA governments have shifted markedly toward domestic borrowing since Eurobond markets closed between spring 2022 and January 2024. The median yield on newly-issued domestic debt reached 8.8% in 2024. While local currency issuance reduces direct FX risk, it has compressed maturities and deepened sovereign bank linkages. Ghana’s average domestic debt maturity fell below three months following its 2023 restructuring. A typical SSA government now spends roughly one-seventh of revenue on interest payments alone. The IMF paper frames the shift as structural evolution rather than policy error, but warns that where it is driven by constrained external access, shorter maturities and tighter bank–sovereign loops could increase vulnerability to future shocks.

Türkiye: Headline CPI inflation accelerated to 31.5% yoy in February from 30.7%, ending a 21-month disinflation streak. Monthly inflation of 3.0% was driven by a 6.9% mom spike in food and an 8.7% mom surge in telecom prices. Energy inflation remained moderate at 2.0% mom for now, but Middle East-related oil price increases will feed through in coming months. Cumulative inflation in the first two months reached 8%, already consuming half of the Central Bank of Türkiye (CBT)’s 16% year-end target. Achieving that target would require monthly inflation to average roughly 0.7% for the rest of the year, which looks implausible. Core CPI inflation eased to 29.5% yoy, below headline.

The CBT is expected to hold its policy rate at 37% at the 12 March meeting. The central bank has suspended one-week repo auctions, effectively tightening liquidity by forcing funding at the 40% overnight lending rate. It also announced Lira-settled forward FX selling to limit exchange rate volatility. Brent crude has risen roughly 20% since the conflict began, trading around USD 80, well above the CBT’s recently revised assumption of USD 60.9. A 10% oil price rise is estimated to add 1.1pp to CPI inflation. Türkiye’s 2025 energy deficit was roughly USD 47.2bn, with Brent at USD 68; higher prices will widen the current account materially. Finance Minister Mehmet Şimşek said authorities are working to contain energy pass-through and may revive the sliding-scale fuel tax system to stabilise pump prices.

Developed Markets

US payrolls much weaker than expected.

Germany: The Baden-Wuertemberg state elections saw Chancellor Friedrich Mertz’s Christian Democrats (CDU) lose to the Greens, with the far-right AfD increasing support.

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.