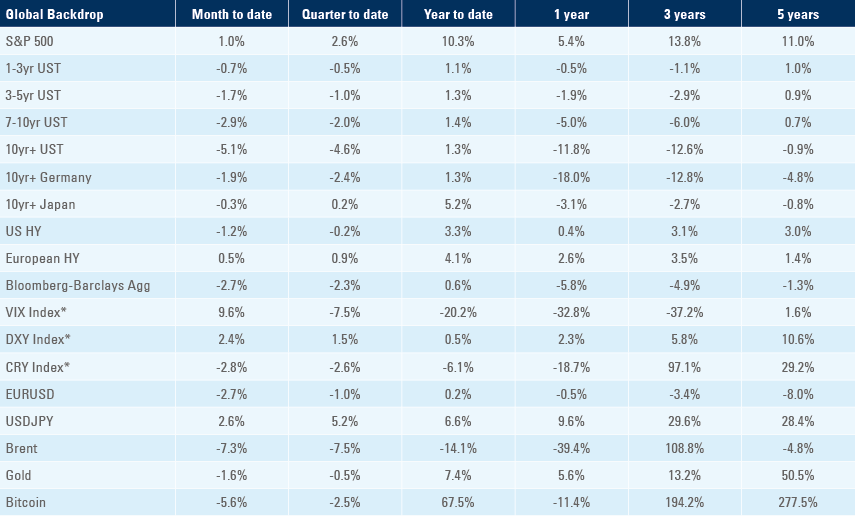

The ceiling can’t hold US: a deal on raising the debt ceiling helps lift market sentiment

Higher than expected earnings in the artificial intelligence (AI) sector, plus the prospects of an end to the debt ceiling stand-off lifted a subset of equity markets last week. However, firmer economic data and inflation numbers pushed bond yields higher. In Türkiye, the people re-elected President Erdogan for a third term, despite his chequered economic track record. In China, bond market stress reached the local government sector, calling for a more aggressive policy response. In South Africa, real yields reach record levels as the central bank shifted focus to its financial stability objective.

Global macro

In the United States (US), negotiations to end the debt ceiling stand-off made great progress as President Joe Biden and House Speaker Kevin McCarthy agreed the outline of a deal over the weekend. The timeline had become more pressing after US Treasury Secretary Yellen announced 5 June as the likely -called ‘x-date’, when the Treasury would have to start prioritising spending. Last week Fitch Ratings placed the AAA rating of US sovereign debt on ‘rating watch negative’, noting the “brinkmanship” over the negotiations, and a second downgrade – after the shock 2011 move by S&P – would have serious implications for certain portfolios. That said, there is no coupon on US Treasury securities due until 15 June, so there is more time to avert a technical default.

Approval of the deal by Congress is not assured, but appears likely at the time of writing. The deal does not entail significant fiscal spending cuts, in contrast to the 2011 compromise, and should therefore be quite positive for asset prices in the short term. On the other hand, it means the US government must start borrowing heavily to replenish its depleted Treasury General Account (TGA) at the Federal Reserve (Fed). This is expected to lead to over USD 700bn in T-Bill supply over the next three months and about USD1.25trn for the rest of the year (June-December). The market impact of this jump in T-Bill supply is uncertain: there are concerns that it will suck liquidity out of the system and increase market volatility. However, a lot of this supply can be absorbed by US money market funds drawing down their large ‘reverse repo’ (RRP) balances at the Fed, whose yield is currently lower than T-bills’ yield.

As ever, the Fed’s monetary policy remains in focus. Minutes from the most recent Federal Open Markets Committee (FOMC) meeting were more hawkish than suggested by Chair Jerome Powell’s remarks, with several participants willing to keep on increasing the Fed Funds rate, while the Chair had suggested taking a wait-and-see approach. Odds are evenly poised: the market is now pricing a 60% probability of a hike at June’s FOMC meeting, and a 95% probability of a hike by the end of July. Afterwards, following some slightly firmer price data, the market has been taking out the probability of rate cuts in the second half of the year.

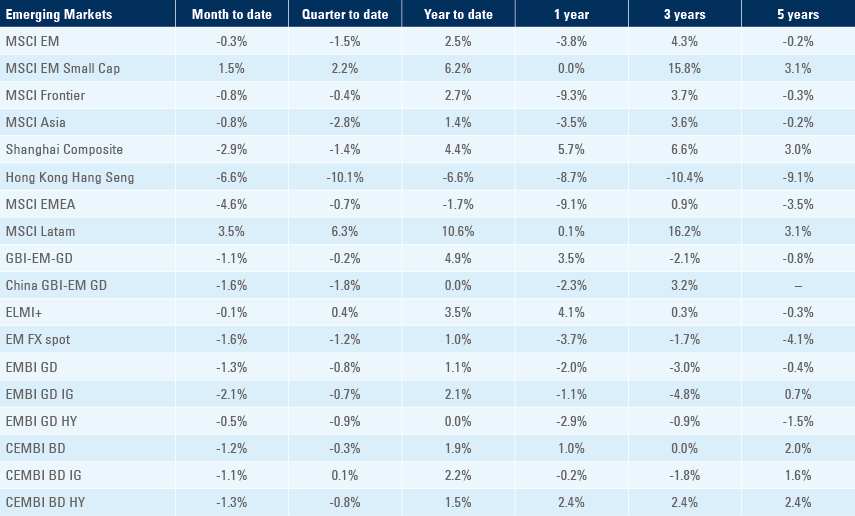

Emerging Markets

Türkiye: President Recep Tayyip Erdogan was re-elected for a third mandate, grabbing 52.2% of the total votes in the run-off of the presidential elections. Kemal Kilicdaroglu, leader of the opposition Republican People’s Party called it "the most unfair election in years" but did not dispute the outcome. There are increasing rumours about market-friendly former finance minister Mehmet Simsek taking a role in the new administration, which would be positive, but it is unclear how much clout he would have anyway. Following his election triumph, President Erdogan said that now his administration had lowered interest rates, next up is lowering inflation. This does not suggest he has much time for more orthodox economic policies. Türkiye's Lira was allowed to trade weaker in the aftermath of the election, taking some pressure off the balance of payments, and external debt securities were trading stronger.

China: China equities were hit last week by concerns over the build-up of public sector debt at Local Government Funding Vehicles (LGFV). The total amount of LGFV bonds outstanding could amount to as much as 60% gross domestic product (GDP), and there have been growing concerns about default risk in this sector. LGFV debt is owned by local banks and funds, and was once deemed too sensitive to fail, but there has been a growing number of restructuring events amid a significant shortfall in local government revenues since the stop in land bank sales a couple of years ago. The view from onshore analysts in Beijing is that the risk around LGFVs can be contained and solved by provincial government without central government transfers. The debt is large but manageable, and the weaker LGFVs are known and can be subsumed by state-owned enterprises or on bank balance sheets. More support could be provided by the central government via Chinese government bond (CGB) issuance. CGB yields (i.e., issuance costs) are low due to excess liquidity. A policy cut of 20 basis points (bps) is priced in, but the Governor of the People’s Bank of China has been reluctant to cut lending rates and instead favours cuts to its required reserve ratio (RRR) to free up more liquidity.

South Africa: Consumer price index (CPI) inflation declined to 0.4% month-on-month (mom) in April from 1.0% mom in March, and the year-on-year (yoy) rate dropped 30bps to 6.8% (consensus 7.0%), while core CPI rose 10bps to 5.3% yoy (consensus 5.4%). Producer price index (PPI) inflation was unchanged in April and the yoy rate was down 200bps to 8.6% (consensus 9.0%). The South Africa Reserve Bank (SARB) hiked its polity rate by 50bps to 8.25%, in line with consensus. The inflation expectations for 2023 and 2024 stand at 5.9% and 4.8%, respectively, so South Africa’s ex-ante real rates are above 4.0%, among the highest for Emerging Markets (EM), and much higher than South Africa’s historical norm. The tight monetary policy stance may not be the ideal response to a supply shock, and is likely to exacerbate the weakness in demand, but it can help support financial stability in our view. The SARB explained that “given upside inflation risks, larger domestic and external financing needs, and power cuts, further currency weakness appears likely”. Nevertheless, we believe these levels of interest rates on the local markets are starting to become attractive. Among other positive attributes, we note the private sector in South Africa is already investing heavily in renewable energy, and that the country still has a solid net international investment position.

Snippets

Asia

- Indonesia: Bank Indonesia kept its policy rate unchanged at 5.75%, in line with consensus, as the current account surplus narrowed to USD 3.0bn on Q1 2023 from USD 4.2bn in Q4 2022.

- Malaysia: The yoy rate of CPI inflation declined 10bps to 3.3%, in line with consensus.

- Philippines: The budget balance moved to a PHP 66.8bn surplus in April from PHP 210.3bn deficit in March, the best monthly result in 30 years, allowing the year-to-date deficit to decline to PHP 204.1bn from PHP 311.9bn over the same period in 2022, as revenues rose by 11.2% yoy and expenditures rose only 1.3% yoy.

- South Korea: The central bank kept its policy rate at 3.5%, in line with consensus, with policy tightening influencing growth and inflation. Household credit declined to KRW 1.85trn in Q1 2023 from KRW 1.87trn in Q4 2023, and is now back to the same level of Q4 2021. The yoy rate of PPI inflation declined another 190 bps to 1.6% in April. Despite tighter credit conditions, consumer confidence increased 2.9 points to 98 in May, standing close to the average of 100.6 since the inception of the series in July 2008.

- Taiwan: The unemployment rate was unchanged at 3.6%. Export orders declined 18.1% yoy in April (consensus -13.8%) from -25.7% in March and industrial production plunged 22.9% (consensus -13.0%) after -16.0% over the same period.

- Thailand: Car sales declined to 59.5k in April from 80k in March, in line with the seasonal pattern.

- Vietnam: The central bank cut its refinancing and overnight lending policy rates by 50bps to 5.0% and 5.5% respectively, while keeping the discount rate unchanged at 3.5%. The yoy rate of industrial production declined 40bps to 0.1%, but retail sales were unchanged at 11.5% yoy in May. The trade surplus increased to USD 2.2bn in May from USD 1.5bn in April as imports declined by a yoy rate of 18.4% (-20.5% in April) and exports declined by 5.9% yoy (-17.1% in April).

Latin America

- Argentina: The fiscal deficit widened to ARS 331trn in April from ARS 258trn in March, the worst result in history, as the country is, once again, negotiating with the International Monetary Fund (IMF) for new funding to avoid running out of foreign currency ahead of a presidential election in October. Any new IMF disbursements will be limited and contingent on a faster convergence between the official foreign exchange (FX) rate of 236 and the parallel rate implied by foreign to local stocks parity at 492.

The economic activity index increased 0.1% mom in March after 0.5% in February (revised from 0.0%) bringing the yoy rate up 90bps to 1.3%. - Brazil: Economic activity surprised positively in May, as the Citibank Surprise Index rose to 26.1 on the 26 May from -22.9 on the first day of the month. CPI inflation declined to 0.5% mom in the first 15 days of May from 0.6% mom over the same period in April, bringing the yoy rate down 10bps to 4.1% over the same period, 10bps below consensus.

Foreign direct investment declined to USD 3.3bn in April from USD 7.6bn in March, and the current account moved to a USD 1.7bn deficit from a USD 0.1bn surplus over the same period. - Chile: PPI moved to -0.4% mom in April from 0.7% mom in March; the yoy rate dropped further to -4.3% as prices increases retraced quickly after staying above 25% between March 2021 and April 2022. Bringing inflation back to the 2016 to 2019 trend line would require PPI inflation to drop another 15.0% from today’s levels, or 16.5% deflation in December 2023.

- Colombia: Industrial confidence declined by almost 10 points to -5.9 in April as retail confidence dropped 6 points to 11.1 over the same period.

- Mexico: CPI declined 0.3% mom in the first two weeks of May after rising 0.2% mom over the same period in April. The yoy rate of CPI inflation dropped 30bps to 6.0% and core CPI declined 10bps to 7.5%, both lower than consensus by circa 10bps.

The trade balance moved to a USD 1.5bn deficit in April after a USD 1.2bn surplus in March and the current account deficit widened to USD 14.2bn in Q1 2023 from USD 2.6bn surplus in Q4 2022. This was the largest deficit on record due to a jump in profit outflows (USD 14.6bn). Some of the profits were reinvested, however, as Mexico recorded USDD 18.4bn in foreign direct investment inflows. - Peru: Real GDP contracted by 0.4% in yoy terms in Q1 2023, in line with consensus, but down from 1.7% yoy in Q4 2022.

Central Asia, Middle East, and Africa

- Nigeria: The central bank hiked its policy rate by 50bps to 18.5%, in line with consensus. Real GDP growth expanded by 2.3% in Q1 2023, down from 3.5% in Q4 2022 and below 2.9% consensus.

Central and Eastern Europe

- Czechia: Consumer confidence declined 4 points to -20.3 and business confidence declined 3.2 points to 6.9 in May.

- Hungary: The National Bank of Hungary kept its deposit rate unchanged at 13.0% but cut the top end of the rate corridor by 100bps to 19.5%. The top-end of the rate corridor has a higher impact on the HUF than bond yields, as it has an impact on easing credit conditions, while bond yields trade close to the deposit rate. The unemployment rate dropped another 10bps to 3.9% (consensus 4.1%); consumer confidence plunged 5 points to -48.5 and business confidence increased 3-points to -4.7 in May.

- Poland: Economic activity posted the largest positive surprise in the region, with the Citibank Surprise Index rising to 11.1 last week from -110.3 on 1 May. The unemployment rate declined 20bps to 5.2%. The yoy rate of retail sales declined 140bps to 3.4% in April, but was 90bps above consensus. PPI inflation dropped 0.7% mom in April from -0.6% in March, bringing the yoy rate down 350bps to 6.8%. Central Bank Governor Adam Glapinski said he hoped inflation would continue to decline, and easing policy rates would become a possibility as soon as Q4 2023.

Developed Markets

United States: US economic activity was surprisingly positive again last week, which alongside very bullish results from Nvidia drove AI-related stocks (including cloud computing) sharply higher. Meanwhile, signs of a possible debt ceiling deal between the White House and the Republican Speaker of the House led to a strong outperformance by US assets. The following economic data were released:

- The yoy rate of core Personal Consumption Expenditure (PCE) deflator rose by 0.1 to 4.7% yoy in April (4.6% consensus); Q1 2023 core PCE was revised higher by 0.1 to 5.0% yoy.

- New home sales rose to 683k, but the rebound from the lows in Q4 2022 was concentrated in the South, driven by dip-buyers. The shallow and localised rebound in home sales is also likely to end when liquidity tightens and unemployment moves higher, in our opinion.

- Initial jobless claims were at 229k (consensus was 245k) while claims from the previous week were revised down from 242k to 225k. Continuing claims declined only 5k to 1.794m, in line with consensus.

- Durable goods orders rose 1.1% mom in April (consensus -1.0%) but were led by lumpy transportation and defence spending as durable goods ex-transportation declined 0.2% mom (-0.1% consensus). Personal spending rose 0.8% mom (consensus 0.5%) in April, twice the pace of personal income at 0.4% mom (in line with consensus).

- The University of Michigan sentiment indicator improved by 1.5 points to 59.2, the ‘future expectations’ gauge remaining below current conditions, while one-year inflation expectations dropped by 0.3 to 4.2%.

- The manufacturing sector purchasing managers’ index (PMI) survey dropped 1.7 points to 48.5 and the services PMI rose 1.5 point to 55.1. The Fed’s regional surveys of economic activity increased but remained at levels consistent with a recessionary environment.

United Kingdom: UK inflation proved surprising resilient with yoy core CPI rising 60bps to 6.8% yoy (consensus 6.2%). Headline CPI inflation declined 140bps to 8.7% yoy (consensus 8.2%), while retail price index (RPI) inflation dropped 210bps to 11.4% (consensus 11.1%). Higher inflation in the UK led front-end rates higher, with the market implicitly pricing in another four rate hikes by the Bank of England, taking the policy rate up to 5.5% in November as two-year Gilts widened by 53bps to 4.49%. The UK front-end rates drove global yields wider last week, with two-year US Treasuries rising 25bps to 4.56% and two-year German Bunds rising 13bps to 2.88%.

Eurozone: Eurozone manufacturing PMI declined 1.2 to 44.6 (consensus 46.0) in May while services PMI declined only 0.3 to 55.9 (consensus 55.5) as consumer confidence was unchanged at -17.4, below consensus at -16.8 over the same period. The German manufacturing PMI dropped 1.6 points to 42.9 and the IFO Business Climate dropped 1.7 points to 91.7, with the current assessment down 0.3 to 94.8 and expectations down 3.1 points to 88.6. Spain’s PPI inflation declined 2.0% mom in April after dropping 2.5% in March, bringing the yoy rate of deflation down 310bps to -4.5%. The Eurozone current account surplus increased to EUR 31.2bn in March from EUR 24.5bn in February, as the Italian current account balance moved to a EUR 3.7bn surplus from a EUR 0.9bn deficit in February.

New Zealand: The Reserve Bank of New Zealand raised its benchmark rate by 25bps to the highest in more than 14 years to 5.5%, in line with expectations, but signalled it may be done with tightening.

Japan: Both CPI and CPI ex-food declined 30bps to 3.2% yoy in the city of Tokyo, but CPI ex-food and energy rose 10bps to 3.9%, in line with consensus. The composite PMI rose 2.0 points in May to 54.9 as manufacturing increased 1.3 to 50.8 and services rose 0.9 to 54.9 over the same period.