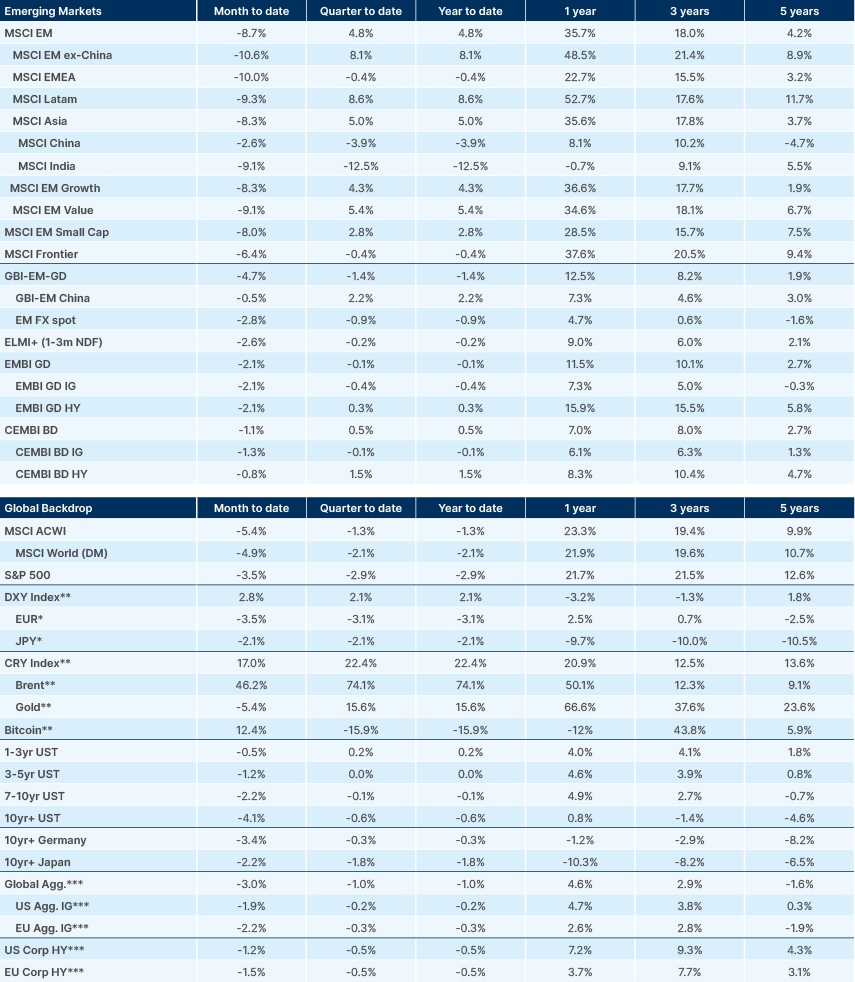

- Brent crude briefly spiked above USD 119 before settling around USD 98 as the Strait of Hormuz remained effectively closed.

- Saudi Arabia cut oil production in March as Hormuz closure depleted storage capacity.

- South Korea has effective oil reserves of just 68 days, including refined product exports.

- Brazil retail sales beat consensus at 2.8% yoy, returning to series peak.

- Banco Master scandal intensifies as Supreme Court Justice Alexandre de Moraes is implicated ahead of October Senate elections.

- Mexico electoral reform fails after Sheinbaum cannot secure two thirds majority.

- Polish fuel CPI forecast raised to 8.0% year on year in March, adding up to 0.8 percentage points to headline inflation by year-end.

- Egypt recorded single-day foreign fund outflows of USD 1.13bn, the highest of the current crisis.

- Gabon formally requested IMF programme after Fitch held its sovereign rating at ‘CCC-’.

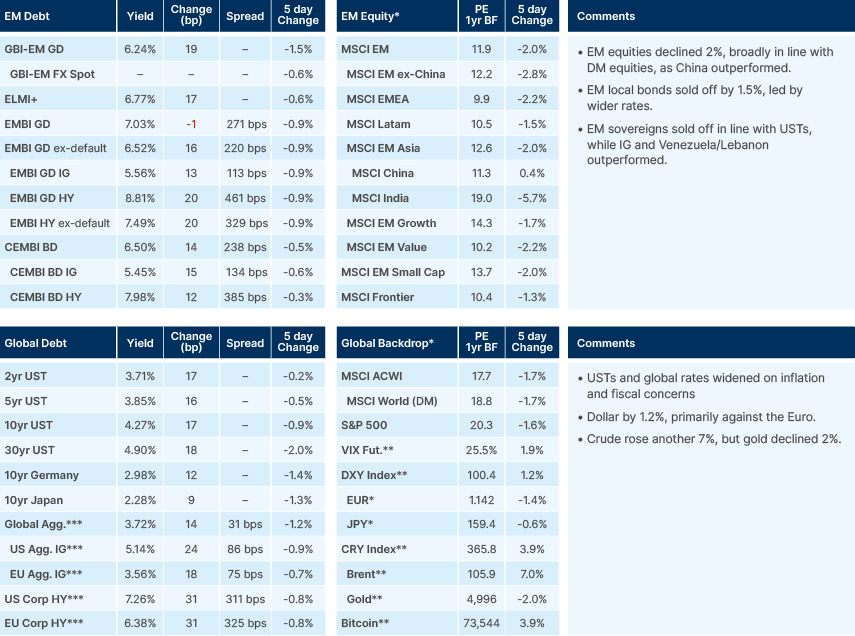

Last week performance and comments

Global Macro

Brent crude spiked to USD 106 per barrel (bbl) this morning as weekend developments pointed toward further escalation in the war between the US/Israel and Iran. Iran’s new Supreme Leader Mojtaba Khamenei's first message via interlocutors called for the Strait of Hormuz to remain shut and warned of additional fronts being opened should the US continue to escalate the conflict. Khamenei has not been seen publicly since the conflict began — Israeli intelligence believes he is wounded and in hiding.

The United Arab Emirates (UAE) was targeted again over the weekend: Fujairah Port (significant as it bypasses the Strait on the Gulf of Oman side) was hit for the second time and Dubai International Airport was hit again this morning by drone attacks. UK Defence Secretary John Healey cautioned Iran may have begun mining the Strait, albeit we know that Chinese tankers are still transiting and recently Indian tankers were allowed to sail as well. US Energy Secretary Chris Wright indicated escort convoys could begin by the end of March.

Asset prices saw some relief earlier last week after the International Energy Agency (IEA) announced a joint effort to coordinate the largest release of strategic reserves ever. However, oil prices rose again as it became clearer this is a mitigant with an uncertain timing due to operational realities. The commodity team of Goldman Sachs now estimates 21 days of full Hormuz disruption with gradual normalisation from 21 March, a reflection of the industry’s adapting to a new reality. In this scenario, cumulative production losses total c. 400 million barrels (mb), but IEA-coordinated releases (254mb actual plus 31mb Russian draws) dampen the inventory hit. Under the base case, Brent stabilises at USD 71 by Q4, or at USD 76 on a scenario of 30 days of disruption, and USD 93 average at 60 days. The US Strategic Petroleum Reserve (SPR) release is structured as a spot-sale/futures-purchase swap, a mechanism that may support further coordinated releases globally if widely adopted.

The US struck Kharg Island military assets over the weekend, though oil loading continues. More consequentially, US President Donald Trump demanded Gulf allies and China share responsibility for Strait security — a signal that the US is no longer willing to be the sole guarantor of Gulf navigation. If there is global cooperation to re-open and keep the Strait open, it would likely effectively change the dynamic of the US acting as the guarantor of free trade worldwide. It would also alter the implicit petro-dollar agreement under which Saudi Arabia sells oil in dollars and recycles its surplus into the US.

Diplomacy between the US/Israel and Iran remains opaque. Trump says the terms are not good enough, while Abbas Araghi, Iran’s Foreign Minister, says he sees no reason to talk. The US has air superiority and can inflict severe damage. However, quick off-ramp has become less clear, as Iran’s ‘pain’ threshold may be significantly higher than expected given its existential framing of the conflict. While Iranian drone attacks are a “nuisance” in Trump’s words, compared with US aerial bombing, Iran retains the ability to control passage through the Strait of Hormuz and to attack oil infrastructure in the Gulf. This means Iran’s ability to negatively impact the current US administration is considerable.

Thus, the risk is that, from a game theory perspective, the war appears to be shifting from a ‘coercive bargaining’ situation to a ‘war of attrition,’ situation, a scenario that often lasts longer than people anticipate (and market’s price). At the same time, a third game theory dynamic at play is the ‘two level game’, where Trump’s domestic political constraints give him a strong reason to end the war sooner, given its unpopularity. This is the ‘TACO’ (Trump Always Chickens Out) scenario. However, ending the war and stabilising energy prices (key for Trump’s popularity), now means reopening the Strait of Hormuz. In the current state of play, that requires either Iranian cooperation, or escalation from the US and allies to combat Iran’s ability to restrict passage through the Strait. The slowing pace of Iranian strikes, together with concessions to countries such as India, Pakistan and China to navigate through the Strait, points to a regime that may be more willing to end this conflict than the rhetoric suggests, in our view.

Asset prices are sending conflicting signals. Rates markets are pricing higher-for-longer oil prices feeding into inflation, whereas equities appear to be pricing a faster TACO. The divergence is notable and will need to resolve one way or the other. In our view, the US Federal Reserve (Fed) is still likely to cut rates two to four times in 2026 to early 2027. The ongoing softening of the labour market is being exacerbated by the supply shock from oil prices. This morning, Reuters reported Meta is planning layoffs that could affect up to 20% of its workforce. Oracle and Amazon are also considering further cuts as the software industry comes under pressure. Most importantly, Trump must reopen the Strait of Hormuz by the end of next month, with escort convoys, if necessary, to avoid a disaster in the mid-term elections. The fact that he is talking about bringing NATO and other countries (even China) onboard highlights this. The combination of energy supply disruption, tightening private credit conditions, and a weakening labour market argues for a defensive posture.

Private debt stress is broadening. UK mortgage lender MFS collapsed after a USD 1.5bn fraud, after similar failures at US lenders First Brands and Tricolor. Last week, Deutsche Bank’s share price fell 6% after it reported a USD 30bn exposure disclosure (5% of loan book) to business development companies (BDCs) alongside a USD 1bn litigation risk. US banks had lent around USD 300bn to private credit vehicles as of June 2025, with Wells Fargo the largest lender at USD 57bn, as per Moody's. Loan fund outflows rose to USD 2.5bn, the largest since April 2025. Redemptions are accelerating, with more funds imposing gates. Because private market valuations lag public markets, monthly redemption caps effectively reward investors who submit larger requests early. The sector also carries meaningful exposure to software companies, where artificial intelligence (AI) disruption risk is non-trivial.

That said, in our view this does not represent a systemic risk,. Corporate credit to GDP has been declining, rather than increasing, as private credit has largely replaced banks and leveraged loans without adding net leverage. BDCs and private credit funds operate under explicit leverage constraints, with most at or below 2x debt/equity. Bank exposure is back-leverage: indirect, senior, and small relative to balance sheets, which makes this fundamentally different from the period before the global financial crisis. Gating is a design feature intended to prevent fire sales, not a sign of structural failure.

Emerging Markets

Asia

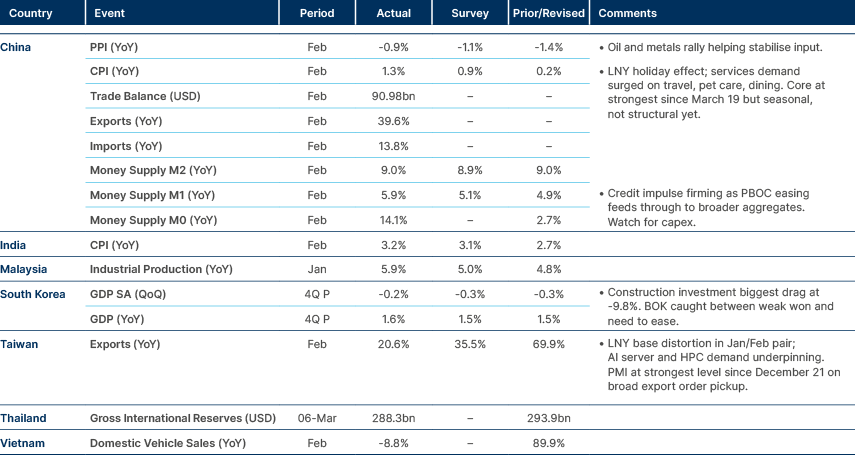

China: Activity data for the first two months of the year were better than expected. Industrial production accelerated to 6.3% yoy, up from 5.2% in December, as 35 of 41 sectors posted expansion, led by electronic equipment (14.2%) and transport (13.7%). More importantly, fixed asset investment (FAI) rose 1.8% yoy after contracting on a yoy basis for the last two quarters, as infrastructure investment jumped 9.8% yoy, a sharp turnaround from 16% yoy decline in December. Manufacturing FAI also improved, rising 3.1% yoy from -10.6% prior. The rebound is most likely due to the lagged effects of policy support from Q4 2025, including financing tools that directly channelled funding into infrastructure. Retail sales improved to 2.8% yoy in January to February, from 0.9% in December. The extended Lunar New Year holiday helped, as tobacco and liquor sales surged 19.1% yoy, while household appliances rose +3.3% yoy and furniture +8.8% yoy, all exited a long period of yoy contraction, easing concerns of fading of subsidy effects. On the negative side, auto sales declined 7.3% yoy, down from -5.0% in December. Altogether, the data suggest the Chinese economy has started the year on better footing, thanks to policy support.

Malaysia: Zeekr, XPeng and MG Motor plan to begin local assembly in Malaysia this year, capitalising on the full tax exemption for locally-assembled electric vehicles (EVs) that runs through to end-2027, following the expiry of import exemptions on fully-built vehicles from January 2026. Separately, Petronas flagged a mixed impact from the Iran war — higher upstream revenues largely offset by downstream cost pressures. The company noted Malaysia is a net crude oil importer for domestic refining, though it remains a net energy exporter when liquified natural gas (LNG) is included. The net financial impact depends heavily on the duration of the disruption.

Pakistan: The government unveiled sweeping austerity measures in response to rising global oil prices: a 50% cut in fuel allowances for government vehicles, grounding of 60% of the fleet, a four-day working week, work-from-home for non-essential staff, school closures through 31 March, a 25% salary cut for MPs and full salary waivers for ministers, and a PKR 22bn reduction in the Q4 non-development budget. A PKR 390bn contingency fund is available as backstop. The measures follow a 17–19.6% fuel price hike on 6 March.

South Korea: Samsung Electronics and SK Corp announced combined treasury stock cancellations worth KRW 21.1trn (Samsung KRW 15.6trn, SK KRW 5.16trn), consistent with the recently passed Commercial Act mandating cancellation within one year of purchase. Samsung also disclosed record R&D spending of KRW 37.7trn and capex of KRW 52.7trn in 2025.

On energy security, effective oil reserve coverage falls to just 68 days when refined petroleum exports are included, against the headline 208-day IEA estimate based on domestic consumption alone. The government has secured 8m emergency barrels and is exploring priority purchase rights over a further 6.86m barrels held by foreign refiners. Six nuclear reactors will be restarted ahead of schedule to guard against potential power price spikes during peak summer demand, given that prolonged high oil prices could feed through to LNG costs with a 4–5 month lag.

The Bank of Korea confirmed a cautious, neutral policy stance, holding rates at 2.5% for a sixth consecutive meeting. A 1% increase in global inflation is estimated to raise Korean consumer price index (CPI) inflation by 0.2%. The central bank plans to assess the conflict’s full impact before its April meeting.

Vietnam: Retail fuel prices were raised on 10 March under a government resolution permitting adjustments when base prices rise more than 7%. RON95-III increased 7.1% to VND 29,120 per litre, diesel rose 1.6% to VND 30,710 per litre; mazut climbed by 13.1%. Gasoline prices are now 35–40% above pre-conflict levels, with diesel approximately 60% higher. The Price Stabilisation Fund was activated for the first time in over three years, with allocations of VND 4,000–5,000 per litre. Inflationary pressure through transportation and logistics is expected to build over coming months.

Latin America

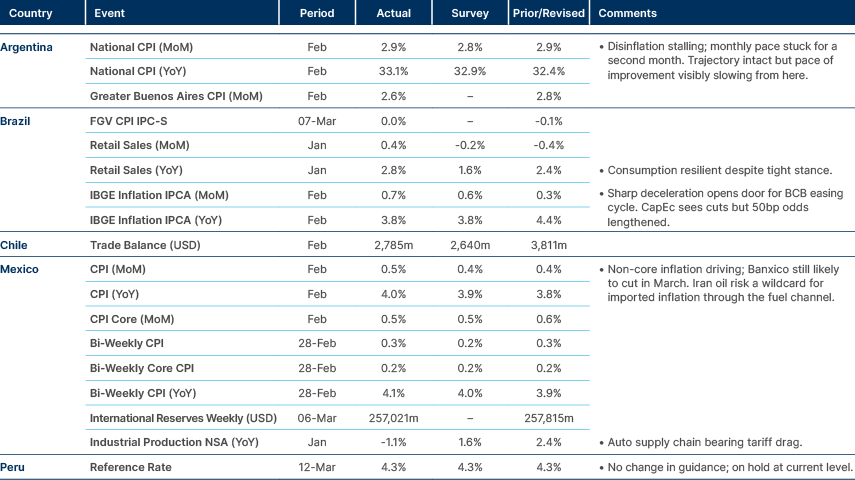

Argentina: Central bank (BCRA) President Santiago Bausili confirmed that remaining FX restrictions are unlikely to be lifted soon, framing them as a containment mechanism against occasional macro imbalances rather than an operational constraint on companies. The residual gap between the official rate (USD/ARS 1,400) and the financial rate (1,460) reflects restrictions on dividend remittances and cross-market operations.

Economy Minister Luis Caputo argued country risk is too high relative to fundamentals and pledged to reduce it by shrinking the stock of global bonds in circulation through asset sales and local debt issuance. Principal repayments of ~USD 1.5bn every six months are seen as manageable. Caputo’s thesis links lower country risk to faster GDP growth, which in turn creates fiscal space for tax cuts and further formalisation, a virtuous cycle that depends on current favourable local conditions holding.

Brazil: Retail sales rose 2.8% yoy in January, beating a 1.6% consensus and returning to their historical series peak. Six of eight monitored categories expanded, led by furniture and white goods (+6.1%) and IT and communications (+5.6%). The result may partly reflect the income tax reform that came into force in 2026, and could support a 25bp Copom easing, though the magnitude remains uncertain.

Finance Minister Fernando Haddad confirmed he will leave his role next week, with his current deputy Dario Durigan expected to take over on an interim basis. No material fiscal shift is anticipated by markets. More consequentially, the Banco Master case continues to escalate following the arrest of ex-CEO Daniel Vorcaro, whose phone data points to extensive political and judicial contacts including, reportedly, Supreme Federal Court (STF) Justice Alexandre de Moraes. The STF’s institutional credibility is being damaged ahead of October’s Senate elections that will renew two-thirds of the Upper Chamber. A right-wing caucus capable of advancing impeachment proceedings against justices is an increasingly plausible outcome in our view, with the trajectory depending on whether a plea bargain implicates opposition or government figures.

Chile: The central bank purchased approximately USD 1bn of gold in February — its first acquisition since 1997 — citing changed correlation dynamics between reserve assets and the growing utility of gold as a portfolio hedge in periods of financial stress. FX reserves rose to a post-Covid high of USD 51bn, supported by the ongoing reserve accumulation programme (up to USD 25m per day, targeting USD 18bn through 2028, with USD 3.3bn purchased since August).

Colombia: Paloma Valencia confirmed Juan Oviedo as her running mate. Oviedo — former Director General of the National Administrative Department of Statistics (DANE) and a centrist with 1.2m primary votes — brings technical credibility and moderate appeal, but lacks executive experience and a political machine. His profile may sit uncomfortably with the conservative Uribist base, potentially driving those voters toward rival candidate Abelardo De la Espriella, who chose ex-Finance Minister Juan Restrepo as his VP pick. The left, coalescing around Iván Cepeda, looks more cohesive than a fragmented right where the Valencia-Oviedo pairing appears partly transactional.

Mexico: The Lower House of Congress rejected President Claudia Sheinbaum’s flagship electoral reform programme by 259 votes to 234, far short of the two-thirds majority required. Sheinbaum later acknowledged that the reform was effectively dead, confirming she would not ask PT and PVEM allies to supply the additional votes needed to reach the threshold. The defeat is a significant governance failure, and cabinet changes are expected, likely including State Minister Rosa Rodríguez. Both coalition allies are likely to pay a cost in the 2027 midterms. Separately, Sheinbaum signed a six-month agreement with fuel retailers to hold regular gasoline at MXN 23.99 per litre, using IEPS tax cuts to offset international oil price spikes. The measure should help Banxico maintain its dovish stance and support further rate cuts in 2026 in our view, though core inflation and minimum wage pressures remain secondary risks.

Panama: At the Shield of the Americas Summit, Trump reiterated his position on blocking foreign influence in the hemisphere and specifically referenced the Panama Canal in the presence of President José Raúl Mulino. No specific actions were announced, but the underlying tension over Chinese influence in Canal operations persists, with Panama having already withdrawn from China’s ‘Belt and Road’ initiative following US pressure.

Peru: Keiko Fujimori (10.7%) has narrowly overtaken López Aliaga (10.0%) in the latest Datum poll ahead of April’s elections, with Aliaga’s drop likely reflecting backlash to his support for former President José Jerí’s censure. César Acuña posted a notable rise to 5.2% from 3.0%. With 38.5% still undecided, the race remains genuinely open.

Central and Eastern Europe

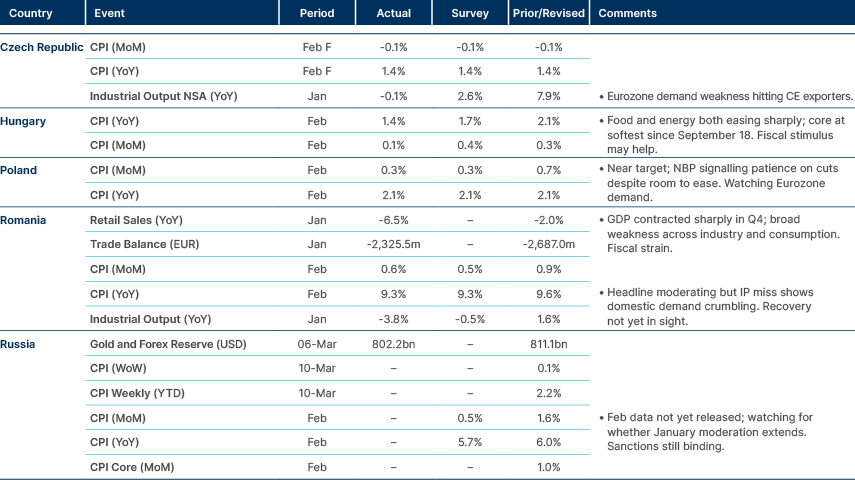

Czech Republic: Czech National Bank (CNB) board member Jan Kubíček struck a firmly hawkish tone, arguing that the current 3.50% policy rate is sufficient to absorb the inflationary impact of the Iran war, which he expects to be transitory and contained within the 2% ±1pp tolerance band. Kubíček dismissed market pricing of two rate hikes as “overdone,” though the European Central Bank (ECB)’s increasingly hawkish signals complicate that assessment. The CNB board remains divided; Kubíček, Eva Zamrazilová and Alěs Michl on the hawkish side, Jan Frait and Jan Procházka more willing to fine-tune, but any rate cut discussions appear to be firmly off the table while the conflict continues. We believe that Iran mining the Strait of Hormuz makes a quick resolution look optimistic.

Kazakhstan: Output rose by 293,000bpd in February to 1.489mbpd, according to OPEC data, coming in below Kazakhstan’s monthly quota of 1.569mbpd and helping offset last year’s overproduction. Despite the Energy Minister’s assurances of compliance, the monthly compensation commitment for H1 2026 averages 581,000bpd — targets missed in both January and February. Full compliance looks unrealistic to us, particularly as elevated oil prices create further incentive to produce.

Poland: National Bank of Poland (NBP) Governor Adam Glapiński floated a plan to realise over PLN 200bn in unrealised gold profits through active reserve management — selling gold for dollars and potentially buying back in two to three years — and transfer 95% to the government as income. The timing is politically charged: the proposal coincides with President Karol Nawrocki’s resistance to signing the EU SAFE implementation bill, and Prime Minister Donald Tusk showed little interest when the plan was presented. With the relevant legislation unlikely to pass and the NBP’s December communication suggesting losses of PLN 100bn in recent years, the whole episode looks more like political positioning than a credible near-term financing mechanism. Glapiński risks renewed parliamentary proceedings as a result.

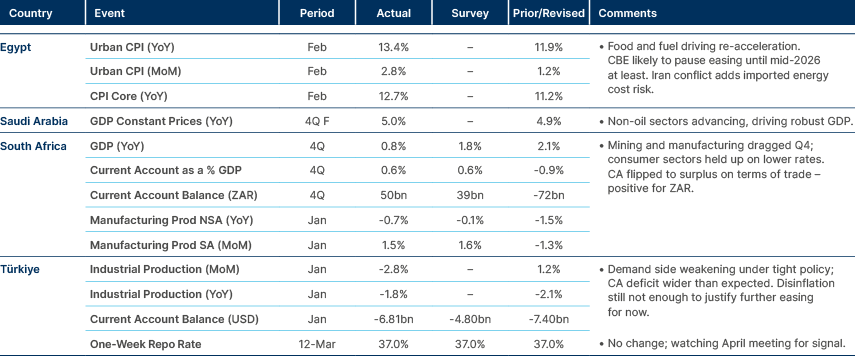

Fuel prices continued to surge in the week to 12 March — Euro95 up 4.5% wow to PLN 6.53 per litre, diesel up 9.3% per litre to PLN 7.64 — with further increases expected the following week. Research publication Emerging Markets Watch (EMW) now forecasts the fuel competent of the CPI inflation index rising 8.0% yoy in March, adding 0.4pp to headline inflation and rising to a 0.6–0.8pp contribution through year-end. Fuel had previously been expected to reduce inflation.

Romania: The Supreme Council of National Defence approved the temporary deployment of US defensive equipment at the Deveselu missile defence site, including air refuelling aircraft, monitoring systems and satellite communications. Parliament ratified the proposal with full ruling coalition support. The move is interpreted as a NATO reassurance measure that deepens bilateral ties with Washington and strengthens Black Sea deterrence, though we believe it may invite more aggressive Russian hybrid pressure in response.

Türkiye: Retail sales volume accelerated to 18.8% yoy in January, beating December’s upwardly revised 16.5%. The headline was driven by non-food categories (+26.4% yoy), with computers and telecoms surging 43.1% yoy — a pattern EMW attributes to front-loading ahead of anticipated further price increases rather than genuine demand strength. Food grew just 9.5% yoy and fuel a mere 0.5%, consistent with households rationing essentials while pulling forward big-ticket purchases.

Ukraine: Hungary seized Oschadbank cash worth over USD 80m from vehicles transporting funds from Austria, later retroactively legislating the action. Budapest framed it as retaliation for Ukraine stopping the Druzhba oil pipeline, while Ukraine attributed the outage to Russian missile damage. Ukrainian President Volodymyr Zelenskyy condemned the seizure as “banditry” and the National Bank of Ukraine conducted emergency USD 73m and EUR 52m cash exchanges for six banks to backstop liquidity. Hungary continues to block the EU’s EUR 90bn loan, with Slovakia potentially joining.

Separately, Zelenskyy publicly criticised Washington’s decision to ease sanctions on Russian oil, warning it could provide Moscow with an additional USD 10bn to fund its war effort. Trump stated the US needed no Ukrainian assistance against Iranian drones.

Middle East and Africa

Egypt: The EGP appreciated 1.5% to 51.99 on Tuesday, despite intensifying capital flight. Foreign funds sold a record USD 1.13bn in T-bills, bonds and equity in a single day, while FX turnover at the interbank market hit a record USD 1.3bn. EMW’s interpretation is that the appreciation likely reflects easing of early-stage panic dollar demand from importers rather than genuine stabilisation. On the fiscal side, the government hiked petrol and diesel prices by approximately 16%, with cooking gas up 38% and compressed natural gas up 30%. The diesel hike to EGP 20.5 per litre carries the broadest inflationary reach given its role in transportation and industrial activity.

Gabon: The government formally requested an International Monetary Fund (IMF) programme during a recent staff visit, with further negotiations expected at Spring meetings. An IMF deal is widely viewed as essential for restoring confidence. Fitch downgraded Gabon to ‘CCC-’ in December 2025, citing high default risk on dollar bonds, while Moody’s projects debt rising to 82.6% of GDP in 2026.

Ghana: The Tema Oil Refinery is preparing to increase production capacity from 28,000bpd to 45,000bpd by integrating a second furnace unit, with a medium-term target of 60,000bpd. The refinery only resumed operations in December 2025 after being idle since 2021. Separately, the EU announced it will sign a security and defence partnership with Ghana — its first on the African continent — focused on counterterrorism.

Nigeria: The Q4 2025 trade surplus narrowed sharply to NGN 1.71trn (USD 1.2bn), a 70.8% drop qoq, as crude oil exports fell by NGN 3.1trn from Q3. Daily production averaged just 1.49mbpd, well below pre-COVID levels of around 2.1mbpd. Non-oil exports rose 10.7% yoy, indicating progress in diversification that remains structurally limited.

On a more constructive note, President Bola Tinubu approved a targeted fiscal incentive package — including an enhanced Production Tax Credit — to unlock the final investment decision on the Bonga Southwest Aparo deepwater project, the first Nigerian deepwater final investment decision (FID) since 2008. The project is expected to attract USD 20bn in foreign direct investment and add approximately 150,000bpd upon completion.

Saudi Arabia: OPEC’s February production figures show the kingdom supplying 10.11mbpd to market, but a footnote reveals actual output was 10.88mbpd — confirming that Riyadh pre-positioned crude ahead of the Iran conflict as a Strait of Hormuz contingency. The effective closure of the Strait subsequently forced a production cut of 2.0–2.5mbpd in March as storage capacity was rapidly exhausted, despite the 5mbpd East-West pipeline offering an alternative export route.

Senegal: Dangote Cement sold a 10% stake in its Senegalese subsidiary to the government, reducing its holding to 90%. Revenue at the unit fell 21.4% in 2025 amid weaker infrastructure demand linked to the country’s political transition. The group expects a recovery as policy conditions stabilise and public investment resumes.

United Arab Emirates: Foreign investors were net sellers of USD 95m on the DFM in the week to 6 March. This was the second consecutive week of outflows following seven consecutive weeks of inflows, as the exchange closed 2–3 March due to the Iran war and sentiment soured following Iranian attacks on the UAE. February had been the strongest month for foreign purchases since records began in 2015, making the reversal all the more notable.

Zambia: The government is targeting a tripling of copper output to 3m tonnes annually by 2031, up from 890,346 tonnes in 2025 — itself 8% yoy growth, but short of the 1m tonne target. The strategy involves courting international investors, including from the US, framed explicitly around the energy transition. Zambia also holds material deposits of cobalt, lithium and rare earths.

Developed Markets

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.