Protests in Sri Lanka, Peru and Pakistan send warning signal to governments

Protests in Sri Lanka, Peru and Pakistan have local features but common causes in economic disaffection; In Brazil, Lula confirms his strategic move to the centre ahead of the presidential election; China’s strategy to contain Covid is under strain; Lebanon’s government reaches a staff-level agreement with the IMF ahead of the May general election; Faced with an inflation problem, India’s RBI abandons its accommodative policy bias, while Poland’s NBP charts a more hawkish course.

Emerging markets

Brazil: Brazil’s presidential race continues to provide a steady stream of headlines and the current leading candidate, Lula, continues to grab the centre. First, Lula confirmed that Geraldo Alckmin, a PSDB (centre-left) lawmaker and former governor of Sao Paulo, could be his running mate. However, according to Lula this was subject to the PSDB leadership approving the agreement, and the PT party (Lula’s party) would then analyse the proposal. Second, Lula as president of the PT party made further overtures towards the centre. He suggested that, once in power, he would keep the president of the Central Bank, Roberto Campos Neto, in his post until at least 2024 when his term expires.

In terms of economic news, although the BRL continues to perform strongly, inflationary pressures remain: consumer prices rose 1.62% mom in March (estimate +1.35%) versus +1.01% in February. As a result, CPI rose 11.30%yoy (estimate +11.00%) versus +10.54% in February. Food and beverage prices (2.42% mom) and transportation prices (3.02% mom) were among the items responsible for the surge.

China: On March 27, Shanghai announced a phased lockdown until April 5 in order to carry out mass testing and contain local flare-ups of Covid cases. Then last week, amid a sharp increase in the number of cases, the local authorities extended the lockdown to cover all 26mn people in the metropolis, and tightened the restrictions. Despite the measures, the number of cases continues to rise in most areas of Shanghai, so there appears to be no prospect of the measures being lifted in the near future. The measures required to achieve zero Covid are sometimes drastic and are increasingly met with strong resistance by residents requiring access to food and medical services. The Shanghai metropolis alone represents over 4% of the country’s economic output. The drop in demand from the lockdown is hard to gauge, although shipping services into the city harbour have been stacking up.

The latest China Caixin Services PMI for March dropped to 42 from 50.2, the steepest monthly contraction since February 2020. There have been renewed indications of supportive policy intentions. If nothing else: last week, in its latest meeting memo, China’s State Council announced that they will step up efforts to “flexibly use a variety of monetary tools at an appropriate time to support the real economy.” In efforts to support their local real estate markets, last week five more cities lowered their official housing purchase limits (minimum down payment).

India: The Reserve Bank of India (RBI) undertook a meaningful change in policy stance at its MPC meeting last week. Although the MPC made a unanimous decision to keep both its repo rate (at 4%) and reverse repo rate (at 3.35%) steady, it introduced a new policy rate called the standing deposit facility (SDF), set at 3.75%. This will effectively be the new policy floor – which is now set 40 bps above the old reverse repo policy floor. Importantly, the MPC statement moved away from emphasis on policy accommodation, and the governor confirmed that the RBI is now prioritising inflation over growth, an admission that will satisfy holders of INR assets.

Lebanon: Following high-level meetings with IMF staff in Beirut, the Lebanese authorities and the IMF team reached a staff-level agreement on comprehensive economic policies that could be supported by a USD 3bn, 46-month Extended Fund Arrangement (EFF). This is a positive announcement, which appropriately comes before the long-delayed general elections scheduled on May 15th. However, the deal comes with a long list of pre-conditions, and approval by IMF management and the Executive Board can only come after the timely implementation of all prior actions and confirmation of international partners’ financial support. Among the main conditions to the agreement are the following items: (i) Parliamentary approval of the 2022 Budget, which was finally agreed by the Cabinet last month; (ii) Parliamentary approval of a reformed bank secrecy law to bring it in line with international standards, which has been a controversial topic; and (iii) Cabinet approval of a medium-term fiscal and debt restructuring strategy. This is but a foretaste of the sort of political commitment required of the new political leadership that will emerge from the elections, but the stakes are high for the Lebanese political class.

After the news of the IMF agreement, Lebanese Central Bank Governor Riad Salameh revealed that Lebanon had 286 tonnes of gold reserves valued at USD 17.5 billion at the end of February. Salameh said the reserves represent the second-largest gold reserves held by a country in the Arab region. He also claimed that the Lebanese foreign reserves reached USD 12.75 billion at the end of February. These numbers have not been confirmed by the IMF.

Just prior to the announcement of the deal with the IMF, Lebanon made global headlines when Deputy Prime Minister Saadeh Al-Shami, a respected technocrat not known for incendiary comments, stated that “the Lebanese State, and the Lebanese Central Bank (Banque du Liban – BdL) are in bankruptcy.” Lebanon’s financial difficulties are well known, so the most remarkable aspect of the statement was probably not the admission in itself but the strong reactions it received from the stakeholders that stand to lose the most in a financial and debt restructuring. Al-Shami’s statement foresaw the possibility of just this sort of grand bargain, and was no doubt intended to signal to all the stakeholders (the banks, the central bank, the creditors and indeed the depositors), that everyone will have to contribute.

Pakistan: Pakistan’s Supreme Court, in a unanimous vote, declared unconstitutional a parliamentary move that cancelled a scheduled no-confidence vote against Prime Minister Imran Khan a few days before. The Supreme Court reinstated the vote, which took place last Friday and resulted in Parliament ousting Khan by a narrow 2-vote majority. Parliament reconvenes on April 11 to pick his replacement, most likely resulting in opposition leader Shehbaz Sharif becoming the next Prime Minister.

Khan’s premiership had been facing an increasingly challenging economic situation, with rising food and energy prices, that led him to reinstate energy price subsidies last month - reneging on an important commitment to the IMF. Khan’s relations with the US have become increasingly strained since Biden’s election and the US withdrawal from Afghanistan. Khan notably raised a few eyebrows by meeting with President Putin after Russia invasion of Ukraine. He progressively lost the support of the army, which he had enjoyed since his rise to power. Shehbaz Sharif is the younger brother of three-time PM Nawaz Sharif. He has vowed to re-establish better relations with the US, and he is seen as enjoying good relations with the army. The two men will vie again for the premiership at the next general election, which must be held before August 2023.

Importantly, while the political crisis was unfolding last week, Pakistan’s central bank raised interest rates by 250 basis points to 12.25%, following an emergency meeting.

Peru: Political instability continues to plague Peru, which has gone through four Cabinet changes since President Castillo’s election last year. The situation deteriorated last week with the start of large-scale protests, motivated by popular demands for political and economic changes in response to rising inflationary pressure. Headline inflation increased to 6.82% yoy in March (from 6.15% yoy in the previous month), pushed by high food inflation and energy prices. While not high by regional standards, it is a high level for Peru, where inflation has averaged 2.8% since 2000. The central bank believes that inflation will be back within the inflation tolerance band before Q3 2023, but nevertheless decided to hike rates by 50bp, to 4.50%, at the last Monetary Policy Committee meeting. Policy makers continue to highlight that they can do more, if necessary, to bring inflation back to its 1-3% tolerance band.

Sri Lanka: Sri Lanka has been beset by violent protests in recent days as a deepening economic crisis sent huge crowds into the streets to demand the departure of President Gotabaya Rajapaska under the slogan ‘Go Home Gota.’ The President briefly declared a state of emergency last week, before having to backtrack following the resignation of his Cabinet and many members of his parliamentary group. President Rajapaksa used his powers on Wednesday to set up a new panel of fiscal experts and bureaucrats to advise him on the debt crisis and economic matters. On Thursday, he swore in Weerasinghe, a career central banker, to head the monetary authority. The next day, Weerasinghe increased the standing lending facility rate to 14.5% from 7.5%, and the central bank governor said: “I am here to implement independent policy making. There is no political interference in my regime, I have made it very clear to the authorities.” Although many issues remain, not least of which is social unrest, the recent economic policy decisions have precipitated a belated decision to ask for assistance from the IMF, which is medium-term positive. Discussions with the IMF are scheduled and will continue in Washington. The central bank’s policy rate increase constitutes a ‘downpayment,’ a sign of commitment to an economic stabilisation programme.

Poland: The National Bank (NBP) hiked its policy rate by 100bps to 4.5%, a bigger step than the 50bps hike expected by the market. The NBP also hiked its deposit and lending rates commensurately. This more hawkish policy stance is in sharp contrast to last year’s gradual approach and was not motivated by the risk of financial instability like last month’s 75 bps – indeed, the EURPLN exchange rate is now stronger than prior to Ukraine’s invasion. Rather, it was explained by the central bank’s view that inflation will remain above target throughout its forecast horizon. The market expects further policy rate increases and already prices in a terminal rate of over 6%.

Snippets

- Chile: Exports rose 22.2% from the same month a year ago and 24.5% from February to USD 9.5 billion. It was the highest figure since 2013, according to the central bank, as mining shipments reached USD 5.5 billion, an all-time monthly high. Imports to Chile jumped 19.2% yoy in March to USD 8.2 billion. The monthly trade surplus of USD 1.3 billion in March pushed the 12-month trade surplus to USD 8.8billion. In keeping with a theme seen everywhere else, March mom CPI inflation was higher than expected at 1.9% (1.2% expected). This took the yoy CPI up sharply to 9.4% form 7.8%.

- Colombia: CPI inflation rose by 1.00% mom in March, slightly above expectations, taking headline yoy CPI inflation up to 8.53% (5.31% ex-food). Food was once again the main upside driver, rising 2.84% mom, while non-food mom inflation was at 0.59%.

- Costa Rica: Rodrigo Chaves (PPSD) defeated Jose Marias Figueres (PLN) in the presidential election, with 52.8% of the votes vs. 47.2%. Chaves has hawkish views on fiscal policy, which bodes well for the continuity of the IMF program. For instance, last week Chaves reiterated that he strongly opposes a bill designed to cut the fuel excise tax, responsible for 0.6% of GDP in government revenues.

- Kenya: Kenya’s budget for the FY22/23 budget year ending in June 2023 is targeting a fiscal deficit of 6.2% of GDP, down from 8.1% in FY2021-22.

- Mexico: Headline CPI inflation accelerated to 7.45% yoy from 7.28% in February. Core yoy inflation reached a 21-year high of 6.78%, up from 6.59% in February.

- Philippines: The Philippines March CPI rose 4.0% yoy vs. 3.4% expected.

- Romania: National Bank of Romania (NBR) hiked the policy rate by 50bp to 3% as expected and struck a relatively dovish tone in its monetary policy statement.

- Russia: The CBR surprised with a large 300bp key rate cut, justified by a change in the relative balance of risks between inflation (easing), growth (uncertain) and financial stability (preserved by capital controls). It has been widely reported that, despite heavy international financial sanctions against Russia, the rouble (RUB) has recovered all of its losses and has traded below 80 (per USD). This is the result of an increasing current account surplus, which may reach 15% of GDP this year, strict capital controls and frankly the impact of US sanctions that make it unattractive to hold US dollars. This may lead the CBR to ease capital controls, unless an unexpected event such as a decision by the EU to ban imports of Russian oil and gas were to occur.

- South Korea: The yoy rate of CPI rose to 4.1% in March from 3.7% in February

- Turkey: March CPI came in at 5.5% mom (energy's direct contribution was at 1.2pp), and reached 61.1% yoy, showing broad-based deterioration across all goods and services sub-groups. On a monthly basis PPI reached 115%, up from 105% in the previous month, signalling intense ongoing inflationary pressure. The CBRT has not reacted to this recent increase in inflationary pressure, and seems to have become complacent owing to the Lira’s relative stability that has come from increased local and foreign demand for FX-protected TRY deposits.

Global backdrop

United States: The minutes from the March 16 FOMC meeting confirmed market expectations that the Fed will start reducing its balance sheet in May and will ramp up over three months to relatively high “caps” of USD 95bn in monthly balance sheet size decline. Although most of this decline will come from maturing Treasuries and MBS securities, T-bills holdings will also be steadily reduced over time.

Nevertheless, many FOMC members are worried that the genie of rising inflation expectations is out the bottle, and that they have to start putting a lid on demand. Although some forward-looking indicators of economic activity in the US are pointing to a slowdown (starting with the shape of the yield curve, but also deteriorating consumer confidence survey data), the starting level for rates is too low and monetary policy works with long lags. Fed speakers have been increasingly blunt in ‘signalling’ their intention to act, but the Fed needs results and needs them fast. This was again on display last week when Deputy Chair Lael Brainard opened a conference address by quoting legendary Fed chair Paul Volcker: “The dual mandate isn't an either-or proposition,” This suggests that Ms. Brainard would not mind if unemployment went up – for a change.

But instead, the US job market remains red hot. The shortage of workers is apparent in the latest jobless claims number which came in at 166K new claimants; this is the second lowest number ever - with the lowest recorded back in 1968 at 162K. Continuing claims are also at 53-year lows but remain 50% greater than the June 1969 record low of 1 million.

The US Mortgage Bankers Association (MBA) said the average contract rate on a 30-year fixed mortgage rose 10 basis points to 4.9%, its highest level since 2018, an increase of 1.07 percentage points in the last eight weeks, its swiftest rise since 2003. Higher rates do seem to translate into lower demand: on a 12-week moving average basis, the MBA mortgage index and mortgage refinancing series are at their lowest levels since late 2016.

This week the focus will be on the US March CPI report on Tuesday. The mean forecasts put the mom increase at 1.2% and the yoy increase up to 8.4% (from 7.9% in February). Core inflation is also expected to increase to 6.6% from 6.4%. Many economists expect headline and core CPI to peak in March and start declining in the spring.

Europe: France’s first round of its presidential election took place last weekend amid a growing tide of support for both right wing (Ms Le Pen) and left wing (Mr. Melenchon) populist challengers, and waning support for the staunchly pro-Europe, liberal incumbent President Macron. As expected, President Macron came in first, with a slightly better than expected 28% of the vote and Ms. Le Pen came in second with 23% of the vote. Both will go into a rematch of the last election’s run-off in 2017. Melenchon once again came third with c. 21% of the vote. However, with the complete collapse of the traditional centre-right and centre-left parties (the candidate for ‘Les Republicains’, the political family of ex-President Sarkozy, only got 5% of the votes), Melenchon has become the kingmaker. Many of his voters come from segments of the electorate that have been antagonised by Macron’s policy preferences, so President Macron cannot count on their support. However, Melenchon himself was perfectly clear, and repeated three times, that no vote should go to Le Pen. This will give Macron supporters, and many worried pro-EU voters everywhere, some comfort ahead of the run-off on April 24th.

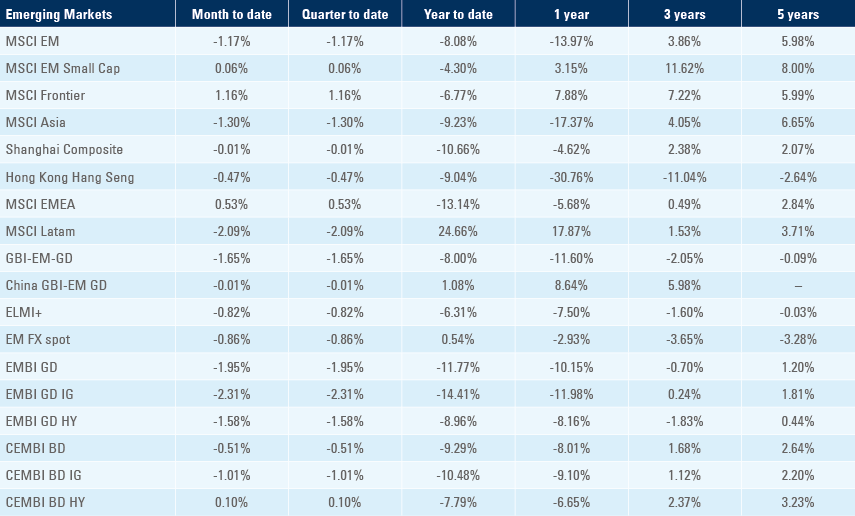

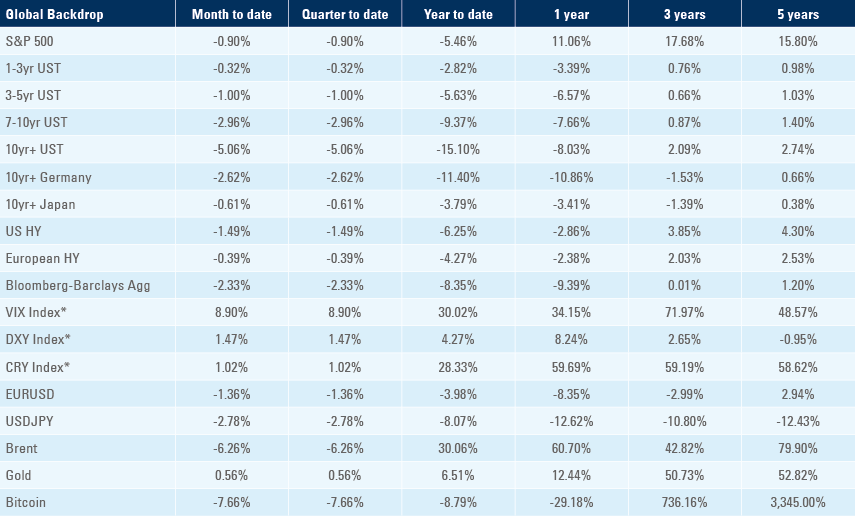

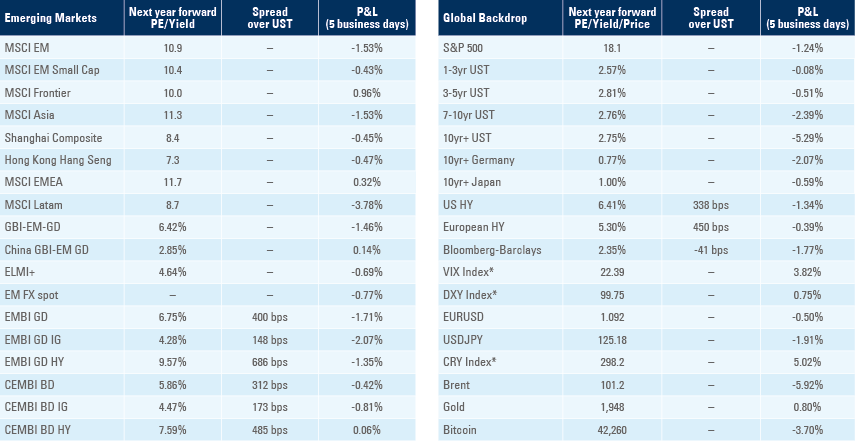

Benchmark performance