Petrobras offers investors the opportunity to have their cake and eat it, in a socially responsible manner

Argentina had better fiscal numbers than expected, mostly due to creative accounting and one off factors. The 2022 presidential races start to shape up in Brazil and Colombia. Petrobras’ strategic plan offers to distribute its entire market capitalisation over the next five years. China announced an elderly health care scheme. El Salvador is far from an agreement with the IMF. Mexico unexpectedly changed the central bank nominee at the last minute. The Turkish Lira depreciated again last week.

In the global backdrop, the new variant of the coronavirus is likely to keep volatility elevated over the short term, at least until scientists understand the transmission, severe cases and fatality patterns as well as whether current vaccines offer significant protection against transmission and severe cases. According to scientists, new variants with several mutations tend to be less fatal (as it seems to be the case in omicron). The world is paying the price of DM countries hoarding vaccines instead of coordinating the distributing of vaccines to low income countries.

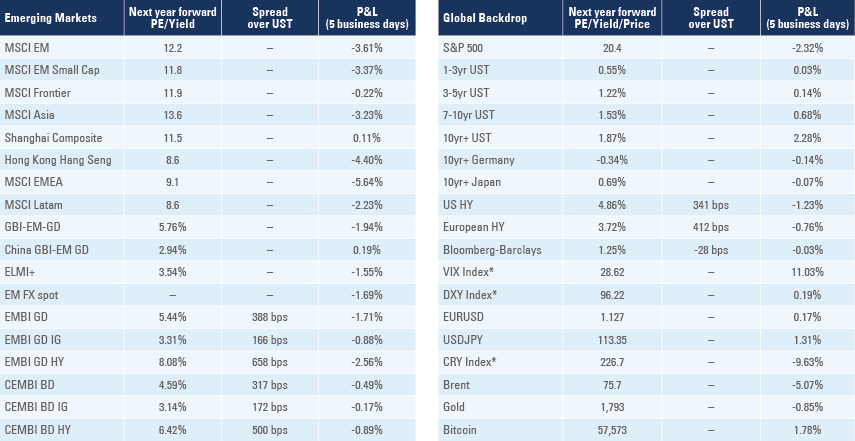

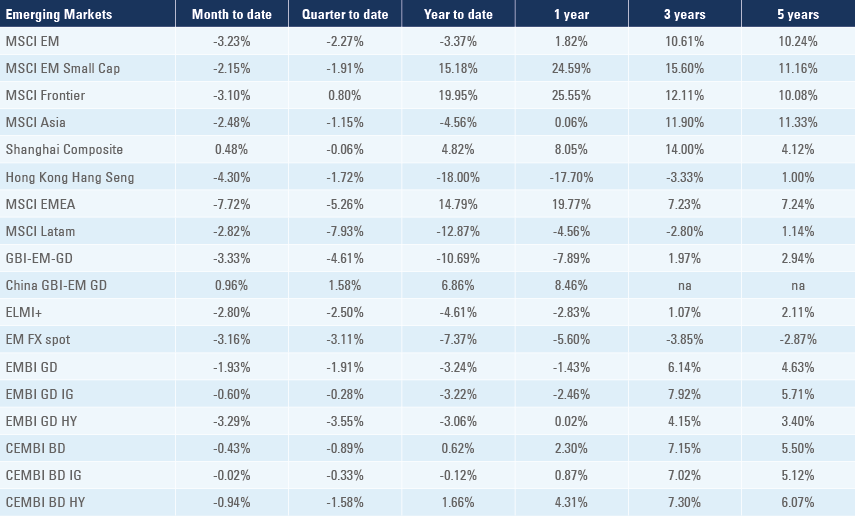

Emerging Markets

Argentina: The economic activity index rose 1.2% in September after increasing 1.1% in August, twice the level of consensus. The trade surplus was marginally down (by USD 0.1bn) to USD 1.6bn in October, higher than consensus as exports dropped USD 0.7bn to USD 6.9bn (but remained at the highest levels since 2021, buoyed by agricultural exports) and imports dropped USD 0.6bn to USD 5.3bn. The fiscal balance moved to an ARS 209bn deficit from ARS 291bn surplus, accumulating 2.2% of GDP deficit in the first 10 months of the year. However, the fiscal deficit was 3.7% of GDP after excluding one-off revenues of taxing wealthy individuals and recording the IMF Special Drawing Rights (SDR) injection as revenues, a small fiscal consolidation from the 6.7% of GDP deficit in the first 10 months of 2020.

Brazil: In political news, a poll by Ipespe for the October 2022 presidential election shows former president Luiz Inacio Lula da Silva with 42% of vote intentions, incumbent Jair Bolsonaro at 25% and former Judge Sergio Moro with 11% of vote intentions. The poll shows Lula winning in both run off simulations taking 52% vs. 32% against Bolsonaro and 51% vs. 34% against Moro. The Governor of Sao Paulo Joao Doria won the primaries of the Social Democrat Party (PSDB). Doria pledged to unify his own party and seek a broad alliance with other political parties to present a viable alternative to the polarisation between Lula and Bolsonaro. In economic news, inflation seems to be plateauing as CPI was unchanged at 1.2% mom, in the first half of November leading to an increase in the yoy rate of 0.4% to 10.7%, broadly in line with consensus. Tax collections improved to BRL 179bn in October from BRL 149bn in September, slightly ahead of consensus. The current account deficit widened to USD 4.5bn in October from USD 1.9bn in September while foreign direct investment (FDI) declined to USD 2.5bn (from USD 4.6bn) over the same period.

In corporate news, Petrobras held an investor day and made several important announcements, including a revised dividend policy. The company already has one of the lowest carbon intensity in the offshore oil and gas industry and will invest USD 2.8bn over the next five years to achieve a 25% reduction in absolute operating emissions by 2030. The company’s break-even oil price (total costs including tax) is forecasted to drop from USD 29 per barrel to USD 20 per barrel as production increases from current 2.7 million barrels of oil per day (b/d) to 3.0m b/d in 2025 and 3.2m b/d in 2026. The company expects to generate USD 150-160bn of free-cash flow which will allow for USD 60-70bn of dividend payments between 2022 and 2026.1 In other words, Petrobras aims to distribute its entire market capitalisation (market cap) in dividends over the next five years. Despite the generous dividend distribution, the company Enterprise Value (market cap plus debt) is only 2.8 times its annual EBITDA2, which is a steep discount to 5.1x EV/EBITDA of its median global peer (GICS3) according to Bloomberg. The company’s price-to-earnings ratio stands at 3.8x against 6.7x of its median global peer.

China: The technology company Baidu received approval to start testing autonomous cars in Beijing. In economic news, the yoy growth rate of industrial profits rose to 24.6% in October from 16.3% yoy in September, remaining close to the highest levels since the beginning of the series in 2007. The National Health Commission (NHC) said half of the regions are planning to launch local pilot schemes increasing the number of elderly care facilities and boosting the number of elderly care professionals providing at-home visits, as well as improving the pricing system. The aim is to improve medical and care services in 2022 with a goal to roll out the scheme nationwide in 2023.

Colombia: The right-wing Centro Democratico (CD) party nominated Oscar Ivan Zuluaga as its presidential candidate. Zuluaga was the Finance Minister under Alvaro Uribe and lost the 2014 presidential election to Juan Manuel Santos, receiving 45% of the valid votes, hence a strong contender to the dispute. Finance Minister Jose Manuel Restrepo said the 2021 fiscal deficit is likely to be lower than expected while the Central Bank Board kept the 2022 inflation target at 3.0% with a +/-1% tolerance band. In economic news, industrial confidence declined 8.2 to 12.2 in October while retail confidence rose 1.4 to 41.7 over the same period.

El Salvador: El Salvador will borrow USD 1bn to fund the creation of a Bitcoin mining facility supported by renewable energy as the president continues to add exposure to Bitcoin after corrections. The IMF said the discussion of a programme with El Salvador has not started and stated the risk of making Bitcoin a legal tender in its latest Article IV report published last week. According to the IMF, Bitcoin’s use as a legal tender entails “significant risks to consumer protection, financial integrity, and financial stability, due to its high price volatility”. Bitcoin use “also gives rise to fiscal contingent liabilities”.

Mexico: Last week President Andrez Manuel Lopez Obrador (AMLO) said former Finance Minister Arturo Herrera is no longer the nominee to become Banco de Mexico (Banxico) governor. AMLO nominated Victoria Rodriguez Ceja, the current Deputy Minister for Expenditures in the Ministry of Finance since 2018. The surprise decision raised eyebrows as Ceja was unknown by the market, raising fears of political interference at the Banxico. In our view, AMLO does not intend to interfere in monetary policy decisions, as he understands high inflation would be unpopular. AMLO has been pushing Banxico to use the recent USD 12bn SDR injection by the IMF to repay external liabilities and asking for Banxico’s profits to be transferred to the Treasury, which is a common practice in other jurisdictions, but not allowed under current rules. Banxico’s next policy decision will be particularly important as the yoy rate of CPI inflation rose to 7.1% in the first two weeks of November, above consensus and the highest levels in 20 years. In other news, economic activity declined 0.4% in September after dropping 1.6% in August bringing the yoy change in economic activity growth to 0.9% from 4.3% yoy over the same period (consensus 2.5%). The trade deficit widened to USD 2.7bn in October from USD 2.4bn in September, also below consensus.

Peru: Another week with plenty of political noise in Lima. Early in the week, Prime Minister Vasquez announced plans for closing four mines (around 7% of gold output) involved in social conflicts, but later in the week the government reached a deal with the companies (including Hochschild`s Inmaculada and Pallancata mines) to keep their mines operating.4 The congress approved the 2022 budget proposed by the government after three days of debate, including higher social spending. At the same time, 29 opposition lawmakers from Congress presented an impeachment motion citing “moral inability” to govern. The motion needs to be voted by 52 of the 130 parliamentarians for impeachment proceedings to begin. The motion is unlikely to pass, at least for now, as both parliament and the population remains highly divided: more than 25% of the Peruvian population favour impeachment, but 31% are against the process, according to a poll by Ipsos.

Turkey: The TRY depreciated more than 10% last Monday as President Erdogan said the country “abandoned old policies based on high borrowing costs and a strong currency in the name of slowing inflation”. Erdogan said Turkey has instead pursued a new set-up that prioritises greater investments, exports and strong job creation. The TRY retraced part of its losses during the week as Turkish banks sold US Dollars and the UAE committed USD 10bn in investments to the country.

Snippets

Chile: PPI inflation rose by 5.3% mom in October after declining 0.2% mom in September, bringing the 12-month moving average to 2.4% mom, the highest levels since 2010.

Czech Republic: Business confidence rose 1.7 to 8.4 in November as consumer confidence dropped 7.5 to -16.0. Economists surveyed by Bloomberg expect CPI inflation at 3.7% in 2021 (from 2.9% in the previous survey) and 4.9% in 2022 (from 2.5%), while GDP growth was down to 2.8% in 2021 (from 3.5%) and 4.4% in 2022 (-0.1%).

Ghana: The Bank of Ghana hiked its policy rate by 100bps to 14.5%, while consensus expected no change policy as the yoy rate of CPI inflation rose to 11.0% in October.

Honduras: The opposition candidate Xiomara Castro declared she won the presidential elections on Sunday. Castro is the wife of former president Manuel Zelaya, in power between 2006 and 2009 before a military coup removed him from power.

Hungary: The National Bank of Hungary increased the one-week deposit rate by 40bps to 2.9% accumulating 110bps increase in the policy rate in November, which helped to support the Forint. In other news, business confidence rose 0.4 to 9.1 while consumer confidence declined 9.9 to -25.1.

Malaysia: The yoy rate of CPI inflation rose 0.7% to 2.9% in October, only 0.1% above consensus.

Mozambique: IMF Representative, Alexis Meyer-Cirkel suggested the fund is close to reaching a financial programme with Mozambique saying, “talks with the government and the materialisation of a financial programme will depend on the dialogue and interest on the government’s side’’.

Nigeria: The Central Bank of Nigeria kept its policy rate unchanged at 11.5%, in line with consensus.

Philippines: The balance of payments moved to a USD 1.1bn surplus in October from a USD 0.4bn deficit in September as the budget deficit narrowed to PHP 64.3bn from PHP 181bn over the same period.

Poland: The yoy rate of retail sales rose to 14.4% in October (12.5% yoy consensus) from 11.1% yoy in September, while sold industrial output declined 1.0% to 7.8% yoy and construction output was down 0.1% to 4.2% yoy (both beating consensus). The yoy rate of PPI inflation rose another 1.5% to 11.8% in October, 0.8% above consensus while the unemployment rate was unchanged at 5.5%.

Romania: A survey of 21 economists by Bloomberg showed consensus CPI increasing to 5.0% both in 2021 and 2022 (from 4.0% and 3.3% respectively) while GDP growth declined 0.3% to 6.7% in 2021 and was unchanged at 4.7% in 2022.

Russia: The yoy rate of industrial production rose 0.3% to 7.1% in October, significantly above consensus. The yoy rate of PPI inflation rose another 1.2% to 27.5% in October, in line with consensus.

South Africa: The yoy rate of PPI inflation rose 0.3% to 8.1% in October, broadly in line with consensus.

South Korea: The Bank of Korea (BoK) hiked its policy rate by 25bps to 1.0%, in line with consensus.

Taiwan: The yoy rate of industrial production declined 0.3% to 11.3% in October, slightly below consensus.

Zambia: The Bank of Zambia hiked its policy rate by 50bps to 9.0% in November (consensus unchanged) as the yoy rate of CPI inflation rose to 21.1% in October, significantly above the 6-8% target range. An improvement in the energy supply after a normalisation of the level of the hydroelectric reservoirs, combined with the strong appreciation of the Kwacha since the election of President Hakainde Hichilema and further hikes in policy rates, is likely to bring inflation back to single digit levels, in our view.

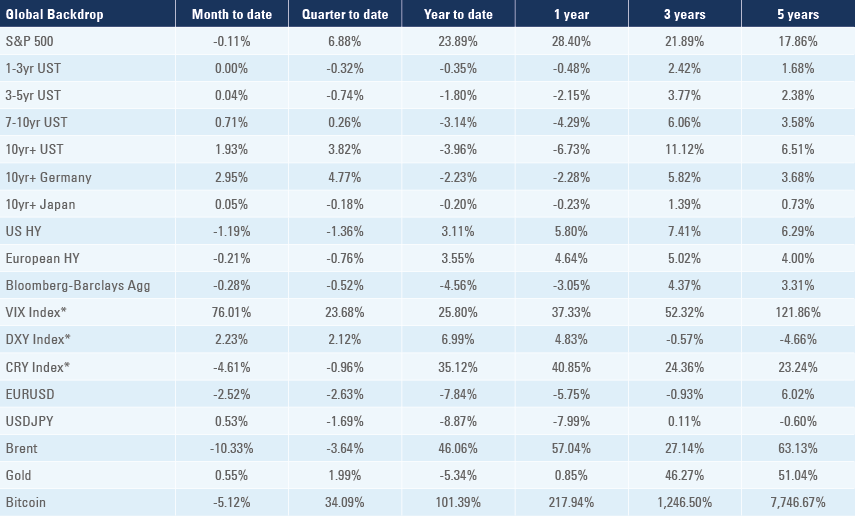

Global backdrop

Covid-19: A new coronavirus variant named omicron (B.1.1.529) with a long list of mutations, was identified in Botswana and South Africa last Thursday with cases identified in several other countries, including the UK, Germany, Italy, Belgium and Australia. Israel closed its international borders while several countries announced travel restrictions to passengers from African countries. Switzerland announced a 10-day quarantine to travellers from countries where the new variant was identified.

Early data from cases in South Africa suggests the omicron variant spreads even faster than the delta variant. Albeit variants with several mutations tend to be less deadly, there is still not enough evidence to assess whether the new variant presents a bigger threat to life or whether the existing vaccines are effective to prevent cases and severe symptoms.

New variants were expected because of the global failure at vaccinating the lower middle-income and low-income countries, which allowed the virus to spread freely, increasing the odds of mutations. The new variant is also likely to keep China’s zero tolerance policy for longer: a study by Peking University said China would face a “colossal outbreak” of covid-19 on a scale beyond anything experienced elsewhere if it were to reopen its borders in a similar manner to the US. In other news, Merck downgraded its estimate for reductions in hospitalisation and deaths from its antiviral pill from 48% in the interim analysis to 30% in the final analysis last week.

Commodities: Commodity prices declined 4.9% last week led by energy prices as Brent and WTI first futures declined 7.8% and 13.1% to USD 72.7 and USD 68.2 respectively, after the strong impact of the covid-19 new variant in global activity. The main risk for energy prices is lower demand for aviation kerosene if countries decide to close borders. On the other hand, OPEC+ is likely to cut production, should oil prices decline further. But the virus does not change the global energy shortage, which is likely to keep prices supported over the medium term, in our view.

United States (US): President Joe Biden has reappointed Jerome Powell (favoured by Republicans and centrist Democrats Congressmen represented by Manchin) as the Chairman of the Federal Reserve (Fed) for another term, while nominating Lael Brainard (favourite candidate in the eyes of progressive Democrats) as the Vice Chairman. The minutes of the November Federal Open Market Committee (FOMC) highlighted several participants were keen to have an accelerated pace of asset purchasing tapering. Since the meeting, inflation surprised to the upside and the job market become tighter. Last week, initial jobless claims declined to 199k in the week of 20 November from 270k in the previous week, the lowest levels since 1969. Continuing claims declined to 2.05m in the week of the 13 November from 2.11m in the previous week, already below Q1 2006 and quickly approaching late cycle levels reached in Q2 1988, Q1 2000 and Q1 2017. Furthermore, the yoy rate of the Core PCE deflator rose 0.4% to 4.1% and the PCE deflator rose 0.6% to 5.0% yoy.

The combination of tight labour markets with higher core inflationary pressures makes it more likely that the Fed will accelerate the pace of tapering in January, looking to stop purchases by Q1 2022 rather than the current guidance of Q2 2022. Faster tapering would allow the Fed to hike policy rates faster as Chairman Jerome Powell had signalled that the Fed would not hike policy rates before ending the expansion of the Fed’s balance sheet. The market was pricing three hikes of 25bps in 2022 starting at the end of Q2 before the coronavirus news brought interest rates down. Atlanta Fed Director Raphael Bostic said he would favour a faster pace of tapering from January even after the new variant news. In other economic news, the US composite PMI declined 1.1 to 56.5 in November due to a disappointing service PMI (57.0 vs 59.0 consensus) while the manufacturing PMI rose 0.7 to 59.1 (in line with consensus). The main contributors to better manufacturing PMI were delivery times which improved 1.5 to 18.3, input prices rose 1.0 to 87.8 and future activity expectation up 3.2 to 73.3. The goods trade deficit narrowed to USD 82.9bn in October, better than USD 97.0bn in September and USD 95.0bn consensus as exports surged to USD 157.5bn in October from USD 142.2bn in September – the highest level on record while imports rose by only USD 1.1bn to USD 240.3bn. The preliminary durable goods orders declined 0.5% in October after declining 0.4% in September.

Europe: Olaf Sholtz’s Social Democratic Party agreed on a coalition with the Green and liberal FDP parties, bringing an important change in terms of social policies across both Germany and Europe as well as more investment in energy transition and the digital economy. The new coalition government in Germany confirmed plans to phase out coal by 2030 as 80% of the country’s energy would be generated through renewables and 2% of land reserved for wind farms. In economic news, the November IFO survey was as expected with current assessment at 99, expectations at 94.2 and business climate at 96.5, all about 1 point lower than the previous month. The Eurozone composite PMI rose 1.6 to 55.8 in November, significantly above the 53.0 consensus.

New Zealand: The Reserve Bank of New Zealand (RBNZ) hiked its policy rate by 25bps to 0.75%, in line with consensus, but slightly below market pricing. The RBNZ increased its estimate of policy rate to around 2.1% by the end of 2022 and 2.6% by the end of 2023 (above its neutral policy rate estimate of 2.0%) as inflationary pressures continue to build next year.

United Kingdom: The Markit composite PMI declined 0.1 to 57.7 in November, slightly above consensus.

Japan: The Markit manufacturing PMI rose 1.0 to 54.2 in November.

Australia: The Markit composite PMI rose 3.2 to 55.0 in November.

1. Assuming the strategic plan assumptions hold (Brent prices moving from USD 72 in 2022 to USD 55 in 2025 & 2026). See https://www.investidorpetrobras.com.br/en/presentations-reports-and-events/presentations/

2. EBITDA stands for earnings before income, tax, depreciation and amortisation.

3. GICS stands for global industry classification standard.

4. See http://www.hochschildmining.com/en/investors/news