- The US and Israel struck Iran on Saturday morning, killing Supreme Leader Khamenei.

- Oil prices spiked c. 10%, but most asset price reaction has been surprisingly muted for now.

- The Chinese New Year holiday reported record travel numbers, but consumption was moderate.

- Korean investors have recently started buying their own stocks.

- Argentina’s Senate passed labour market reform as growth surprises upwards.

- Inflation surprised to the upside in Brazil, Mexico and the US.

- The IMF completed the fifth and sixth reviews of its economic reform programme with Egypt.

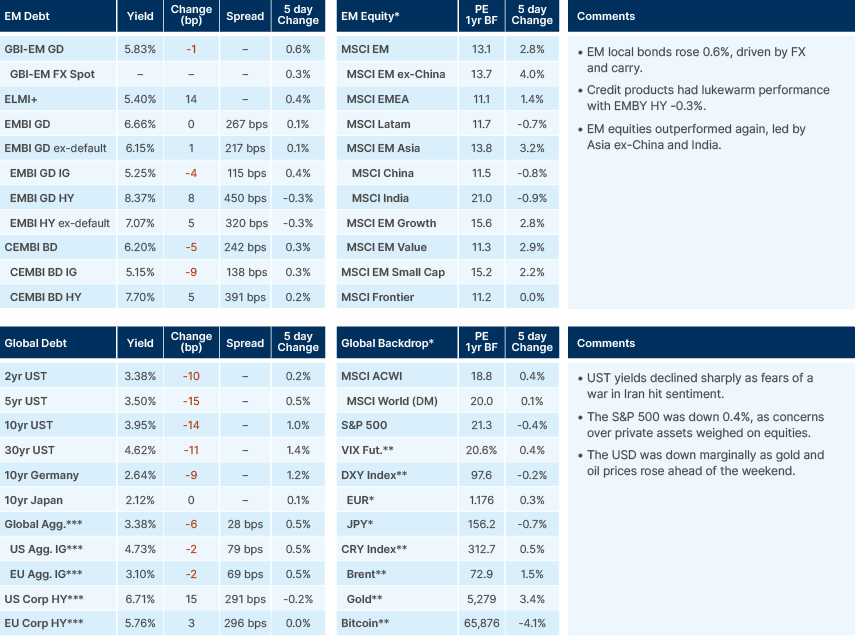

Last week performance and comments

Global Macro

The sentence "there are decades where nothing happens; and there are weeks where decades happen" (often incorrectly attributed to Lenin), is probably the most accurate description of 2026. The US-Israel coordinated airstrike on Iran, and the killing of Ayatollah Ali Khamenei, is by far the most consequential event in the Middle East since the Iranian Revolution of 1978, in our view. Despite the attacks on the United Arab Emirates (including Dubai), Qatar, Bahrain, and Kuwait, the response from Iran so far has been underwhelming. This could either mean Iran is focusing on strategic targets (military bases) or that it has limited resources available. Time will tell. As always there are more questions than answers, and many scenarios to be entertained amid the fog of war.

The most important question for markets is for how long the Strait of Hormuz will be closed. About 20m barrels of oil transit the strait daily, representing c. 20% of global oil supply, with 84% destined for Asia. This means a prolonged Hormuz closure would drive a global recession via a classic stagflation shock. The world's spare oil capacity sits in Gulf states and physically only c. 6.5-8.0m barrels per day (bpd) can bypass the strait. The Iranian Revolutionary Guard (IRGC) has been sending radio messages for commercial vessels not to cross the area, but the number of incidents has been limited at the time of writing. Crucially, insurance companies have said any vessel crossing the Strait is effectively uninsured. That alone will restrict traffic to Iranian ships and its allies, at least until a solution is found. During the 1990 Gulf War, for example, the US Treasury offered insurance cover for ships transiting the area.

In terms of Iranian politics, President Masoud Pezeshkian announced the formation of a Temporary Leadership Council operating under Article 111 of the Constitution. The Council is composed of Pezeshkian, judiciary chief Gholam-Hossein Mohseni-Ejei and Guardian Council member Alireza Arafi, a powerful hardliner and potential succession candidate himself. After decades of immense repression, including the nationwide protests just a few weeks ago, many Iranians would likely welcome a shift from an Islamic-led Supreme Leader system towards a presidential model.

Nevertheless, the base case scenario is for the current regime to remain in place. The ability to change this seems to be dependent on whether the IRGC can prevent disruption from within its own ranks and contain further protests. Another key figure is top security official Ali Larijani, who was not killed alongside Khamenei and other security leaders. Sources suggest he has approached officials from the Government of Oman about restarting talks with the US, although Larijani has denied this.

Iran’s attacks in the Gulf seem to be a way of inflicting pain on US allies, increasing the pressure on the US leadership. Evidently, President Donald Trump is under pressure himself, facing criticism from within his base and from the opposition, having campaigned to end overseas wars. Nevertheless, Trump does not seem to face hard constraints in the short term. The mid-term elections are some six months away, giving him time to withstand even a sharp spike in oil prices, provided it reverses within weeks. Congress is set to vote this week on a war powers resolution aimed at halting the operation, although the move would be largely symbolic as Trump is expected to veto it. Overriding a veto would require a two-thirds majority in both chambers of Congress.

Market reaction has been lukewarm, likely because oil infrastructure assets were not targeted by either side. At 6:30am London time, S&P futures were at 6,780 (-1.5%), Euro Stoxx futures 5,995 (-2.5%), while MSCI EM futures were holding up at around 1,561 (-2.7%). Oil briefly touched USD 82 and is now trading at just below USD 80. Investors have learned to buy into spikes in geopolitical risks as they tend to fade and selling assets during a drawdown can be costly. Indeed, the S&P 500 has tended to remain relatively resilient during most major geopolitical episodes since the 1980s.

Even so, the historical context matters. US stocks fell by more than 10% during the Gulf War, which began on 2 August 1990, as the economy was sliding into recession due to the Savings & Loans Crisis, and the Japanese stock market bubble had just burst in December 1989. The other events were the Venezuelan oil workers strike in December 2002, during a fragile recovery following the 9/11 attacks. At that point, the S&P 500 was already down around 40% from its peak after the Enron and WorldCom scandals crushed investor confidence. The oil workers strike hit c. 15% of US imports (1.5m bpd) as Venezuelan output collapsed from 3m bpd to just 200,000 within two weeks. The other major shock was the Russian invasion of Ukraine on 24 February 2022, which triggered a spike in both energy and food prices, which contributed to a further sell off in US Treasuries.

The US and Israel vs. Iran conflict comes at a time when investors are overweight in US equities, with valuations close to record levels. Credit spreads remain tight due to low odds of a global recession, aided by the AI-driven investment cycle. Nevertheless, whereas the US has the most crowded asset allocation position and expensive valuations, the fact that the US is a net exporter of energy should make it a relative beneficiary while oil prices remain elevated. The more vulnerable markets to a short-term oil shock could be the major oil importers over the last 18-24 months, including Europe, Japan, China, Taiwan, and South Korea.

We would expect any oil price spike from here to be temporary. There seems to be little appetite in the US, and perhaps a lack of ability in Israel, to put ‘boots on the ground’ in Iran. It is hard to say exactly what is the strategic endgame for the US, if one exists, beyond the hope of a transition to a more friendly regime. But this is also speculation. There is a possibility that Israeli intelligence may be more deeply embedded in key Iranian organisations than is currently assumed. This should become clearer in the coming days or weeks.

In the absence of a prolonged closure of Hormuz, we believe the impact on emerging market (EM) assets is likely to be relatively muted. Oil importers, including much of Asia, Egypt, Morocco, and Türkiye are the most vulnerable, alongside the Gulf Cooperation Council countries which have exposed assets. Latin America and oil exporters from Africa are likely to be relatively beneficiaries, offering a counterbalance.

On the monetary policy front, last week Bank of Japan Governor Kazuo Ueda and other policymakers struck a hawkish tone, keeping the door open to a possible April rate hike. In the US, St. Louis Federal Reserve (Fed) President Alberto G. Musalem said inflation is moving toward 2% and the labour market remains stable, with policy rates near neutral and growth at or above potential. Kansas City Fed President Jeffrey Schmid added that inflation progress is ongoing, while the labour market remains in a solid position. UK inflation expectations fell sharply in February, easing pressure on the Bank of England. The decline strengthens the case for earlier rate cuts, as inflation is likely to get close to 2% in Q2 2026.

Geopolitics

US Secretary of State Marco Rubio said the US and China had reached a degree of “strategic stability” despite ongoing disagreements and may explore talks on a nuclear pact. The comments signal room for dialogue ahead of Trump’s China visit in April. In Ukraine, reconstruction needs are estimated at USD 588bn over the next decade, nearly three times the country’s GDP, with transport, energy and housing most affected. The US abstained from a United Nations General Assembly vote on a resolution supporting a "lasting peace in Ukraine". Ukraine’s EU accession has no defined timeline, and Hungary continues to block a EUR 90bn EU loan. Meanwhile, Russia has continued its large-scale strikes on energy and urban infrastructure.

Commodities

This morning, oil prices rose nearly 10%, reaching a peak in Asia of USD 82.5 before slowing down in early European trading hours to just below USD 80. Slightly after 12pm UK time, a headline reporting that QatarEnergy halted liquified natural gas production following an attack on one of its facilities pushed the Dutch natural gas first future contract up 50% to EUR 47.30, the highest level since February 2025.

Emerging Markets

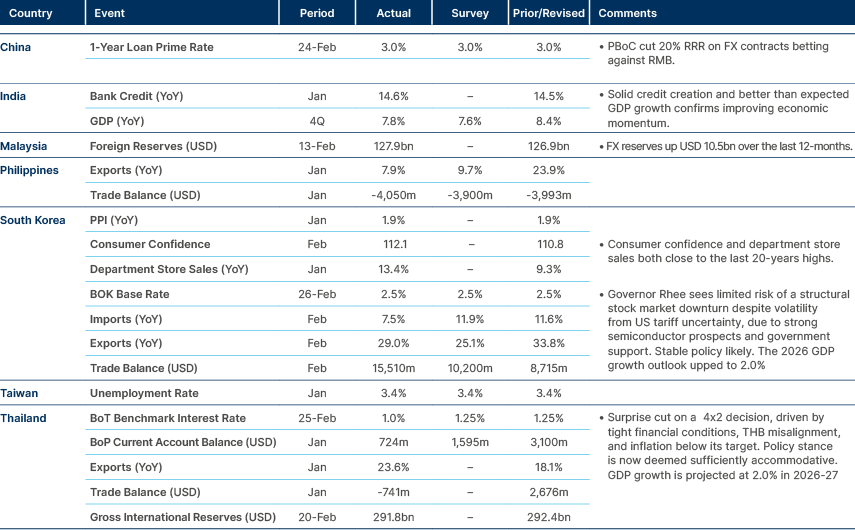

Asia

China cuts RRR to stop RMB strengthening. India data solid, but no cigar (Sensex -6.4% YTD).

China: The seasonal peak in cross-regional passenger flow during Chinese New Year (2.46bn people between 15-22 February) did not translate into strong leisure consumption. Meanwhile, new home sales in the top 30 cities were seasonally weak. However, retail (+5.7%) and services revenues showed strength, with outbound travel continuing to normalise.

In trade news, Beijing introduced a multi-tier export control regime targeting 40 Japanese entities, imposing outright bans on dual-use export to high-risk firms and stricter approvals for others. China’s trade surplus in high complexity products continues to expand, with the surge in net exports since the pandemic driven by high-tech goods. Over the past 20 years, China has shifted from being a net seller of low-complexity goods, such as live animals, food, and precious metals, to a major buyer.

South Korea: Despite the Kospi index doubling in value over the past year, retail investors only recently joined the rally. Growth was driven by President Lee Jae-myung’s market reforms and tax incentives for repatriating overseas capital. However, Korean retail demand for overseas equities remains strong. Buying increased significantly in January and February following a brief lull in December. Overall, the monthly run rate of buying overseas assets this year has been high relative to 2025. While margin loan balances rose, they declined as a percentage of total market cap due to regulatory caps and suspended broker lending. Consequently, retail buyers have turned to leveraged ETFs, which now accounts for c. 20% of all ETF trading on the Korea Exchange.

Vietnam: Mortgage rates surged to 9.6%-13.5%, erasing their traditional discount to private lenders. Private banks’ floating rates now range from 11%-15%, signalling limited room for easing amid rising funding costs.

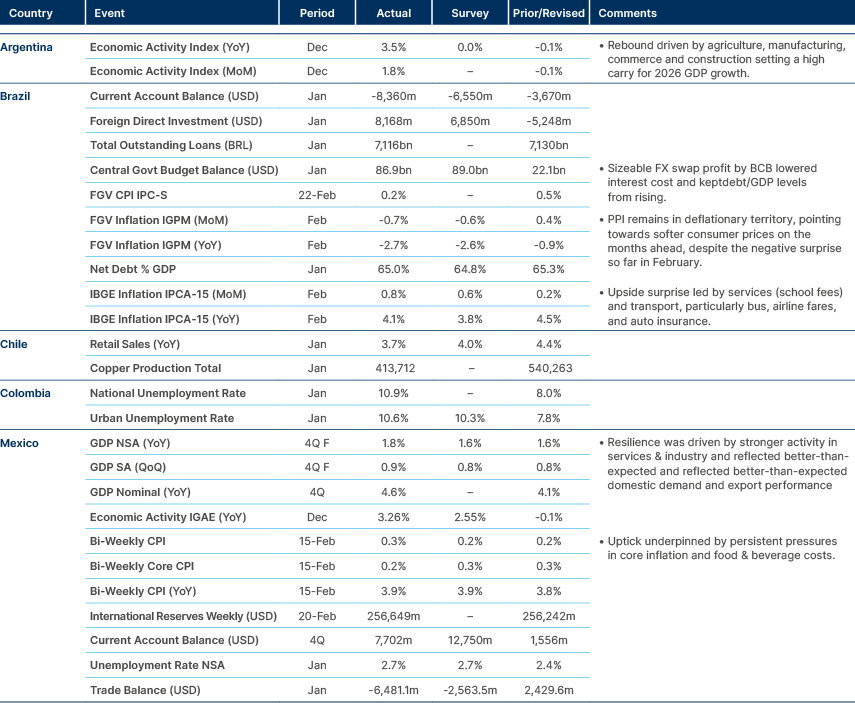

Latin America

Big spike in Brazil’s CPI. Inflation also above consensus in Mexico.

Argentina: The Senate passed the final version of the labour market reform with 42 votes in favour, 28 against, and 2 abstentions. Backed by La Libertad Avanza (LLA)/PRO, Unión Cívica Radical (UCR) and allied blocs, the legislation introduced sweeping changes to around 200 articles of the labour code, including reforms to severance pay, more working-hour flexibility, longer probation periods and limits on collective bargaining and strikes. Peronism opposed the bill. The final version excluded a controversial provision reducing compensation for workers on medical leave.

The balance of power in the Senate is shifting in President Javier Milei’s favour, as three Peronist senators are set to leave the Peronist/PJ bloc, weakening the hard opposition’s cohesion. In addition, Senator Luis Juez has formally joined LLA, taking its Senate representation to 21 seats, improving the government’s ability to build reform-supporting coalitions.

In economic data, activity in December surged 1.8% mom, the strongest monthly gain since July 2024. This brings annual GDP growth to an average of 4.4% yoy.

Brazil: An Atlas Intel poll from last week showed Lula is now statistically tied with Flávio Bolsonaro at 46.2% and 46.3%, respectively marking Flávio’s steady gains. Moreover, Lula’s approval has slipped (46.6%), and his rejection rate (48.2%) now exceeds Flávio’s (46.4%). Other polls point to the same direction.

Chile: The US has revoked the visas of three Chilean government officials who were working with Chinese firms on a proposed submarine fibreoptic cable project linking Chile and Hong Kong during the administration of Gabriel Borich. Ministers said the plans were only preliminary, but documents suggest the government was advancing the project in secret, deepening US-Chile tensions.

Colombia: President Gustavo Petro warned of “immense electoral danger” ahead of 2026 elections, citing alleging risks tied to vote-tabulation software and insufficient oversight that he said could threaten the integrity of the process. Petro provided no concrete evidence to support the claims. The National Registry responded that electoral software is subject to an international audit conducted by the Centre for Electoral Assistance and Promotion.

Floods in the north of the country prompted authorities to declare a 30-day state of emergency to mobilise resources and expedite response efforts. Last week, the government announced a temporary tax on corporate net worth for legal entities with net assets above 200,000 UVT, equivalent to COP 10.5bn or USD 2.78m. The general rate is set at 0.5%, with higher rates, including 1.6% for the financial and mining-energy sectors, to help finance recovery from recent flooding and climate-related impacts.

Mexico: President Claudia Sheinbaum unveiled an electoral reform package that would cut party funding and election costs by 25%, reduce the Senate from 128 to 96 seats, and require all legislators to be directly elected. These changes would weaken party leadership control over plurinominal lists.

As presented, the proposal may be hard to pass since it would hit some of Morena’s coalition partners, and the party does not have enough votes to approve the package on its own. The proposal appears focused on cost cutting, oversight and anti-nepotism measures, rather than expanding executive control over electoral institutions.

The killing of drug lord “El Mencho” is seen as a win for Sheinbaum. The operation was coordinated with US intelligence, which is positive, although Trump publicly took credit. Despite the initial spike in violence, the move is likely to put Mexico’s organised crime groups ‘on notice’ and force them onto the defensive. Even so, the coming months will be critical in assessing the security impact.

Peru: Recent polls show Rafael López Aliaga leads Peru’s presidential race, with support broadly unchanged at 14.6%. Keiko Fujimori remains second at 10.3% (up from 8.1%). Undecided votes fell sharply, indicating preferences are consolidating, though the race remains fragmented and open.

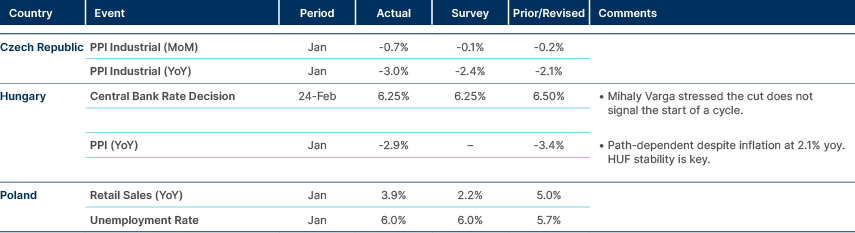

Central and Eastern Europe

Soft PPI inflation in both Czechia and Hungary. Hawkish cut in Hungary.

Middle East and Africa

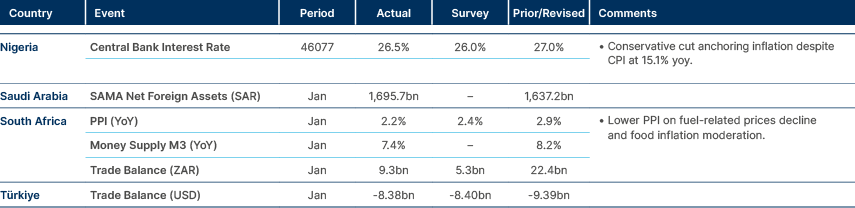

South Africa inflation moderates. Nigeria cuts rates by less than expected.

Egypt: The International Monetary Fund (IMF) completed its fifth and sixth Extended Fund Facility (EFF) reviews and first Resilience and Sustainability Facility (RSF) review, allowing for the immediate disbursement of USD 2.3bn and bringing total EFF disbursements to USD 5.2bn. The IMF praised Egypt’s improved macroeconomic stability and fiscal discipline, but urged the accelerated implementation of structural reforms, especially divestments and effective debt management.

Nigeria: Nigeria’s Monetary Policy Committee (MPC) cut the benchmark rate by 50bps to 26.5% as inflation moderated to 15.1% in January. Central Bank of Nigeria Governor Olayemi Cardoso noted inflation moderation was a result of earlier monetary tightening, exchange rate stability, strong capital inflows and balance of payments improvements.

Saudi Arabia: The trade surplus narrowed to a seven-month low in December (SAR 13bn) as lower oil volumes and price hit export revenues, while imports continued rising on strong domestic demand. Oil still accounts for c. 70% of exports, although non-oil exports machinery, electrical equipment and chemicals, have been rising.

South Africa: The budget kept deficits broadly unchanged (4.5% of GDP in FY25/26). Debt/GDP is set to peak at 78.9% of GDP this year before declining on rising primary surpluses. Lower issuance on the long end of the curve is expected to lead to a bull flattening. Growth was slightly upgraded, a principles-based fiscal anchor is due in 2026. The budget raises the odds of a potential S&P upgrade to ‘BB+’, supporting further asset price outperformance.

Zambia: Inflation fell sharply to 6.5% yoy in February and is now back within the 6-8% target band for the first time since 2019. Disinflation was driven by slower food prices, a stronger kwacha and lower fuel costs, creating room for further rate cuts after the MPC trimmed rates to 13.5%.

Developed Markets

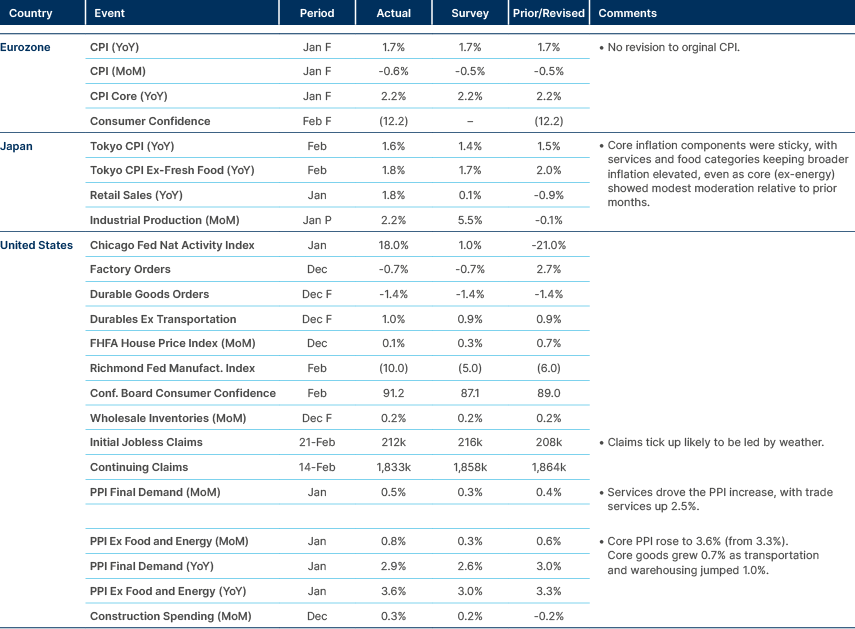

Higher PPI inflation in the US after several months of inflation decline.

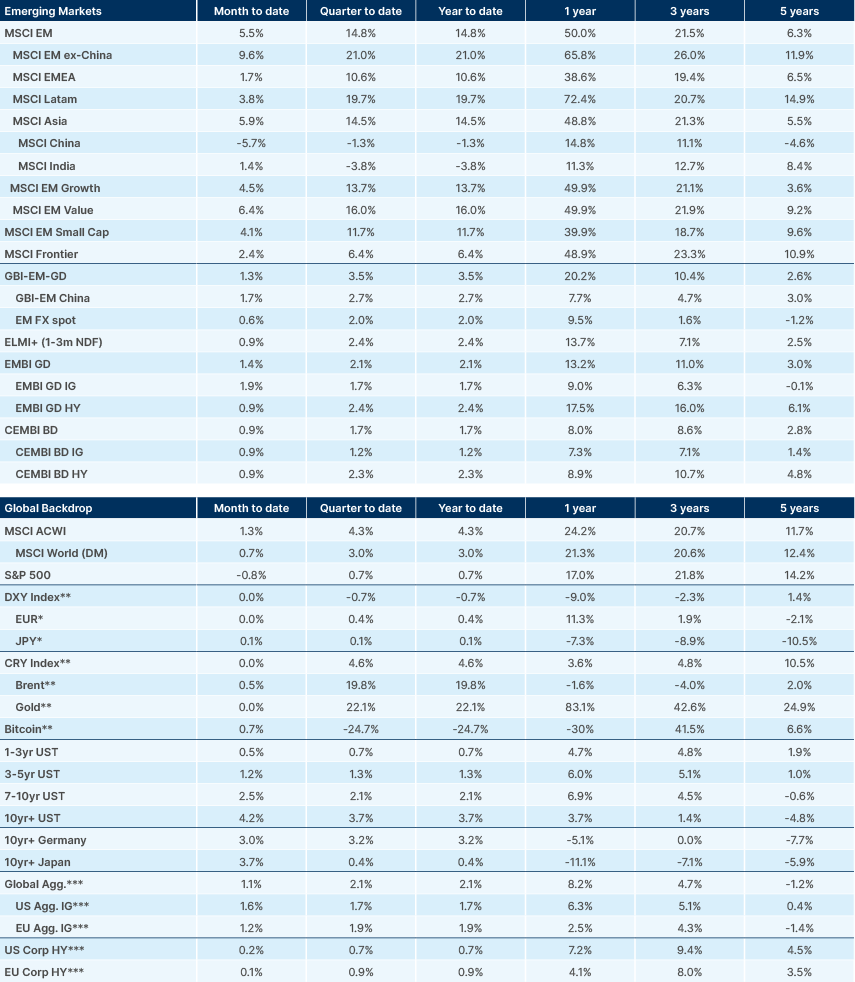

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.