US buyback engine sputters: Supply hits an overextended market

- Record US tech issuance lands on over-extended positioning and valuations.

- Market pricing two Fed hikes over the next year, ahead of Warsh's first meeting on 17 June.

- Iran exchange fire with Israel, but the US keeps pressing for an extended ceasefire.

- India announced measures to increase foreign investor ownership of local assets.

- South Korea announced measures to support the Won.

- Argentina hit its IMF reserve-accumulation target seven months early.

- Colombia's first runoff poll puts de la Espriella ahead of Cepeda.

- Peru’s runoff too close to call: quick counts show Sánchez fractionally ahead of Fujimori.

- Fitch held Hungary at 'BBB'/negative and upgraded South Africa to 'BB’.

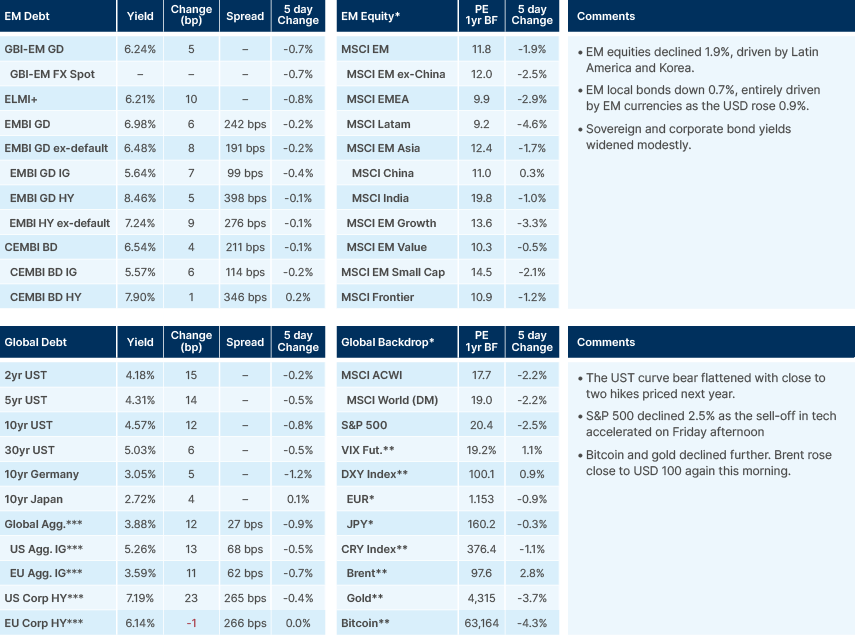

Last week performance and comments

Global Macro

Volatility increased last week after the announcement of large equity offerings tightened liquidity and led to a sell-off in an over-extended market. Google announced a USD 85bn ‘follow-on’ equity offering and Meta announced a potential offering of tens of billions of US Dollars.

The announcements came on the heels of the anticipated Space X IPO of USD 75bn at a USD 1.75–1.80trn valuation range, to be priced this Friday. The prospectus included a galactic USD 28.5trn total addressable market (TAM) of the company’s activities by 2030, mostly by selling AI to enterprises, where the company is way behind its competitors. The TAM is equivalent to 88% of US GDP, or 28% of global GDP ex-China and Russia (markets considered out of reach for Space X as per the prospectus).1

Importantly, Dow Jones kept its inclusion criteria rule for the S&P 500 index unchanged. This means the big incoming IPOs of Space X, Anthropic and OpenAI will only join the index within 6–12 months. The Nasdaq will include the companies within 15 days.

The combined sales of the tech companies can reach USD 300–400bn, close to half of the annual buyback from last year. Technology firms returning cash to shareholders has been a key technical support to the US stock market since 2003. The equity sales may increase significantly if insiders decide to sell most of their vesting shares following the unlock schedule. In the case of Space X, the prospectus mention that, from a c. 4.2% initial floating, there will be 19.55% of shares available for sale after 90 days, rising to 39.3% within 180 days, 47.1% after 340 days, and 97.1% after 365 days.

This technical overhang is hitting the market when there are several signals that allocations to equities are over-extended. Active manager and retail investor positioning is stretched following several months of strong inflows into US equities. The Federal Reserve Conference Board of stock price expectations shows record bullish sentiment. Option markets are showing a record number of stocks with call options trading at higher prices than put options, an inverse of the typical skew on the option market. This also coincides with a record level of valuations (c. 21x earnings) and earnings per share growth (c. 20%), a coincidence unheard of since 1999 and 2000.

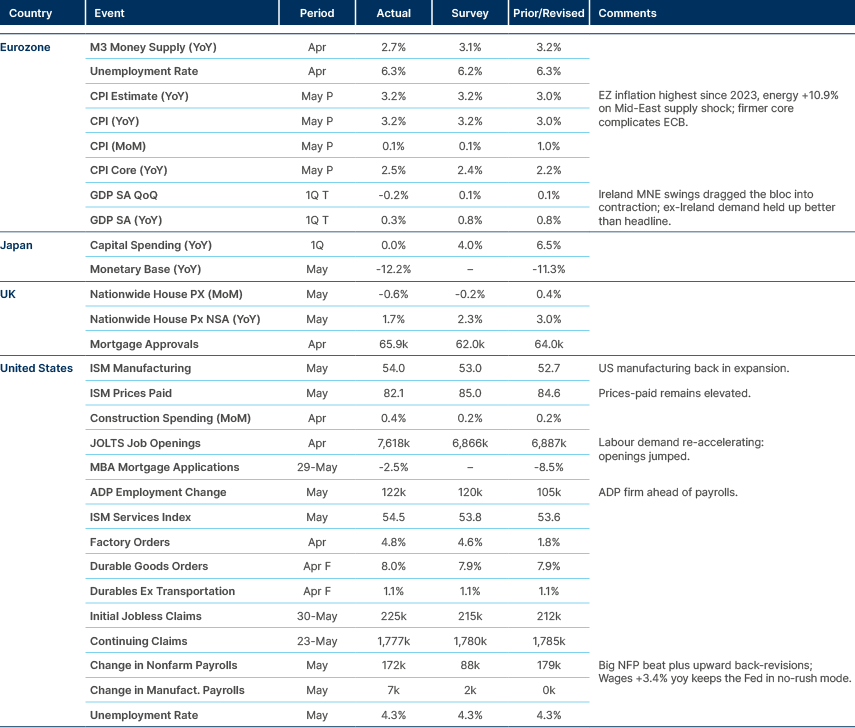

Contributing to the sell-off last week, US data surprised to the upside, leading to wider US rates. The front end now prices two hikes from the US Federal Reserve over the next 12 months. There is considerable uncertainty about the direction of Fed policy and guidance ahead of Kevin Warsh’s first meeting as Fed Chair on 17 June. With this backdrop, the market will monitor US consumer price index (CPI) inflation, which is likely to have peaked in sequential terms last month, but needs to come down to avoid further pressure on the Fed to hike. The European Central Bank (ECB) meets this week, with a 25 basis points (bps) hike fully priced, and another two hikes expected over the next 12 months. With economic data deteriorating in Europe, it is unlikely that the ECB would pre-commit to further hikes this week.

On the geopolitical front, Israel struck military targets in Iran over the weekend, in retaliation against missile attacks by Tehran, despite US President Trump’s call for Israeli Prime Minister Benjamin Netanyahu to refrain from escalation. Axios reporting Israeli strikes were “relatively limited” in scope and the Iranian state media denied it launched a strike towards a US airbase in Saudi Arabia after a missile alert. This morning, Trump said on his Truth Social platform: “there will be an Iran-Israel cease fire shortly” and “negotiations for peace are proceeding”. Trump also said he would not unfreeze Iranian assets or lift any sanctions before a peace deal is reached, but could consider those steps after an agreement. However, the US government disclosed a mechanism to make Iranian frozen assets available to Gulf countries to release for reconstruction of Iran. If confirmed, this resolves a key sticking point for a memorandum of understanding allowing for an extension of the ceasefire and a reopening of the Strait of Hormuz.

Emerging Markets

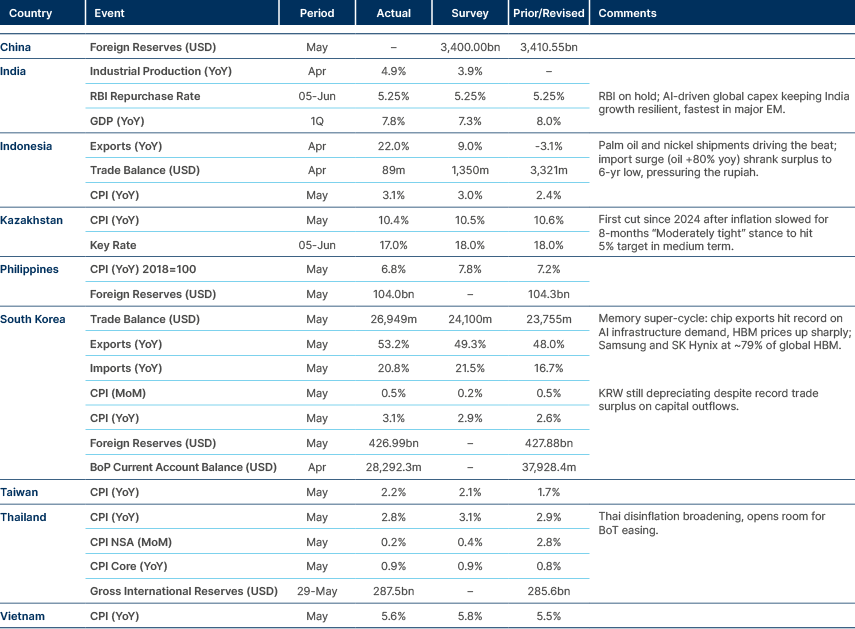

Asia

Softer inflation in Philippines, Thailand, Vietnam. Kazakhstan surprised with a 100bps cut.

India: Last Friday the Reserve Bank of India (RBI) expanded the universe of "specified securities" under the Fully Accessible Route (FAR) by including all new issuances of 15, 30 and 40-year tenor G-secs. This widens the pool of sovereign paper foreign investors can buy without quantitative limits. Investment rules for foreign investors were relaxed alongside incentives for companies and banks to raise funds from international markets. The government also said foreign investors will be exempted from tax on interest income and capital gains on government bonds. These measures helped contain the selloff in INR rates despite higher oil prices and strong GDP data. The measures would bring in USD 40-80bn of FX inflows, which is substantial relative to GIR’s estimate of India’s current account deficit of around USD 78bn in 2026.

Pakistan: State Bank of Pakistan reserves rose USD 43m to USD 17.2bn to 29 May, a seventh straight weekly gain to the highest level since February 2022. Both the central bank and the International Monetary Fund (IMF) expect further gains, helped by dollar purchases averaging USD 726m per month in July to May of FY26. Import cover stood at about 2.7 months, with total liquid reserves of USD 22.64bn.

South Korea: The country’s Finance Minister met with the central bank and regulators to agree an action plan to stop the Won’s depreciation. The measures include tighter oversight of offshore currency derivatives, inspections of suspected market misconduct, and probes into potentially illegal FX transactions.

Authorities will scrutinise offshore non-deliverable forward (NDF) trading, saying one-sided positioning in the market influenced the domestic market. They also pledged to boost transparency and encourage a shift into more activity onshore. The central bank and the Financial Supervisory Service will also conduct inspections to assess whether speculative trading or manipulation contributed to the KRW weakness, warning of strict action if violations are found. Regulators will also probe whether exporters and importers accelerated payments or delayed receipts to benefit from the currency’s slide. President Lee Jae Myung also said USDKRW is elevated, abnormal and will be temporary.

The market is now pricing in six back-to-back 25bps hikes as the market discounts some odds of the Bank of Korea hiking rates to address the KRW weakness. This morning, after an 8% decline, the KOSPI stock market triggered a circuit breaker as the semiconductor sell-off took another leg down following the accelerated drop on the Nasdaq last Friday.

In other news, the government eased safety rules for importing and installing extreme ultraviolet (EUV) chip equipment, a move expected to speed up advanced fab construction by Samsung Electronics and SK Hynix. EUV tools were previously treated as general high-pressure gas facilities, triggering repeated inspections that delayed deployment. An amendment to the High-Pressure Gas Safety Management Act will reclassify qualifying tools as 'specific facilities', shifting to three-yearly process audits. The introduction timeline per EUV unit should fall to about nine days from 34, saving roughly KRW 500m per tool. The change takes effect immediately on promulgation next week.

Vietnam: International arrivals reached 10.6 m in January to May, up nearly 15% yoy and a record for the period, or about 42% of the 25m full-year target. May arrivals were 1.8m, up 16.5%. China and South Korea led at 2.29m and 1.92m, while Russia recovered to about 95% of 2019 levels.

Registered foreign direct investment (FDI) rose 34.9% yoy to USD 24.8bn over the five months, with disbursements at a five-year high of USD 9.8bn, up 9.6%. Manufacturing took 70.4% of registered and 82.7% of disbursed capital. Singapore led new investment at USD 6.8bn, ahead of South Korea (USD 4.2bn) and China (USD 1.8bn).

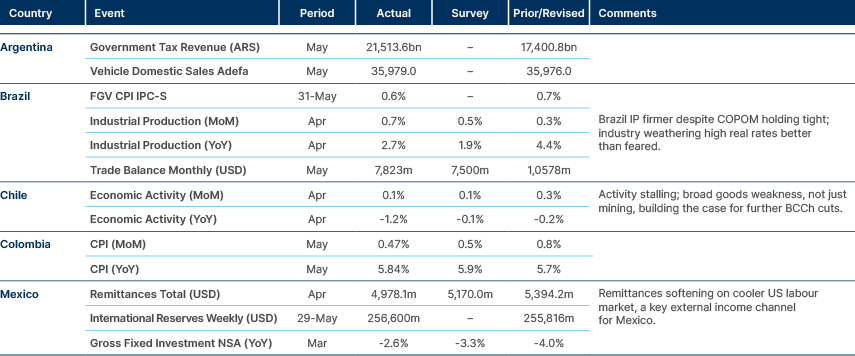

Latin America

Brazil industrial production resilient, Colombian inflation slightly below, but core firm.

Argentina: The IMF said net international reserves rose USD 7bn after central bank (BCRA) USD 10bn spot purchases, near the USD 8bn extended fund facility (EFF) accumulation target for 2026. The EFF measure excludes BCRA repos maturing in 2027. Economy Minister Luis Caputo said the USD 10bn IMF goal had been met seven months early, conflating gross purchases with the USD 8bn net target. He separately said the BCRA will likely end 2026 with USD 17bn to USD 24bn of purchases. BCRA Vice President Vladimir Werning said the BCRA reset its FX firepower by unwinding USD 2bn of short USD future contracts and repaying US Treasury and People’s Bank of China swap drawdowns.

In a positive development for the sovereign’s contingent liabilities, the US Second Circuit sided with Argentina in denying a revision of the USD 15bn claim for YPF expropriation ruling, leaving the claimant a likely-futile Supreme Court appeal or ICSID (International Centre for Settlement of Investment Disputes) proceedings.

President Javier Milei sent Congress an AI legal framework within a wider corporate law reform, pledging light regulation and a “non-human corporation” category. New nuclear guidelines prioritise exports and invite private capital.

In other news, Raizen agreed to sell its downstream oil business, including a refinery and 894 Shell stations, to Swiss trading company Mercuria for USD 1.4bn, creating a third integrated operator.

Brazil: Central bank-surveyed institutions ranked fiscal risks as the top threat to financial stability in the Q2 2026 report, with external risks second on the Middle East conflict, overtaking default and activity concerns. Leverage is stabilising at elevated levels, which could lift defaults, while system confidence stayed high but eased slightly. Respondents raised both the likelihood and impact of fiscal risks, with recent fuel subsidies adding to concerns. The government may still meet its 0.25% of GDP primary surplus target (BRL 34.0bn) only at the lower tolerance band and via exceptions. An expenditure-focused fiscal reform looks inevitable in 2027, its design contingent on the election result.

Chile: President José Kast's first State of the Nation address set out a security and reform agenda while warning recovery would be slow. The address favoured security specifics over new economic policy, consistent with the omnibus bill already covering the reform agenda.

Kast cited an inherited structural deficit of 3.7% of GDP in 2025, unemployment above 8% for 40 months. He has framed the omnibus bill as the tool for a triple fiscal, labour and economic emergency. Term goals are 4% GDP growth, 6% unemployment and at least 300k jobs recovered.

Security measures include deployments in 50 neighbourhoods, task forces on organised crime, a longer flagrancy window and 20k new prison places by 2030. On the economy, he cited a USD 89bn investment pipeline of 389 projects and defended fuel price rises within CLP 1.3trn (c. USD 1.4bn) of spending containment.

Colombia: The constituent assembly initiative backed by President Gustavo Petro's government and leftist candidate Ivan Cepeda was withdrawn, reversing course ahead of a planned 20 July Congress unveiling. The move followed centre-right figure Juan Oviedo signalling conditional support for Cepeda if the proposal were dropped.

A first post-first-round AtlasIntel poll put Abelardo de la Espriella at 50.3% versus Cepeda at 42.6% for the 21 June runoff, though internal inconsistencies suggest non-response bias is inflating the margin. The roughly 2.3m unaligned Fajardo and Oviedo-linked votes is the key swing factor.

Fitch warned of a sizeable fiscal gap, with the 2025 central government deficit at 6.4% of GDP (7.8% ex-temporary savings) and stabilisation requiring about a 4.0% of GDP adjustment, while the fiscal rule committee flagged an unprecedented 4.0% to 5.0% adjustment over the next term.

Ecuador: President Daniel Noboa scrapped the security fee on Colombian goods from 1 June, going beyond a planned cut to 75% from 100%. The reversal followed a 29 May call with right-wing Colombian candidate Abelardo de la Espriella. Bogota repealed its retaliatory tariffs, but rejected Quito's 'goodwill' framing, citing Andean Community rules on ideological non-interference. The measure stemmed from ideological friction with President Gustavo Petro rather than a real trade grievance. A right-wing Colombia, with Ecuador and possibly Peru, would tilt the region towards a pro-US bloc, leaving Brazil the outlier under President Lula.

Mexico: Fitch cut its 2026 GDP growth forecast to 1.0% from 1.7% on a weak first quarter and expects a rebound aided by the World Cup. It assumes no USMCA deal by the 1 July deadline, sees inflation easing to 3.6% by end 2028 – but staying above the 3.0% target – and expects no policy rate change through 2028.

Former president Andres Manuel Lopez Labrador publicly backed President Claudia Sheinbaum and blamed recent US actions on advisors around President Trump. The reference is to the US indictment of several Sinaloa officials, including Governor Ruben Rocha, and rumours of more to come. We see the indictments as the main risk to the ruling Morena bloc, despite its resilient popularity.

Peru: Roberto Sánchez holds a very narrow lead in Peru’s presidential election runoff, according to two early quick counts. An Ipsos quick count showed Sánchez at a 0.6pp advantage with 50.3% vs. conservative Keiko Fujimori’s 49.7%. Datum showed Sánchez with just a 0.2pp lead at 50.1% vs Fujimori’s 49.9%. Exit polls had shown Keiko Fujimori slightly ahead, but the Ipsos count has a good track record of calling the results.

A Sanchez win could be seen as negative for Peruvian assets given expectations of a larger state role and uncertainty regarding the central bank (BCRP) and the economic policy framework. Sanchez's aim to rewrite the Constitution still seems like a tall order given such reform proposals will face a lack of congressional majorities by both presidential adversaries.

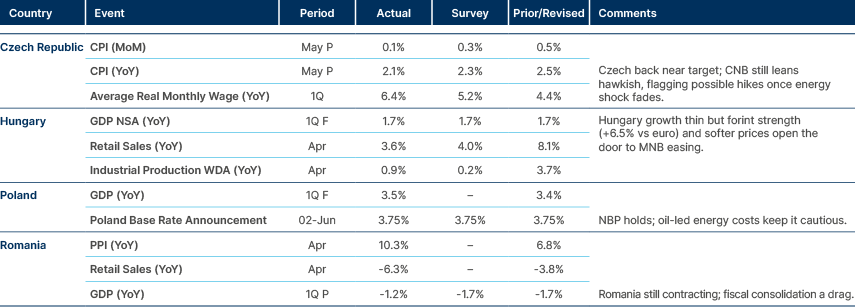

Central and Eastern Europe

Poland left policy unchanged due to energy shock.

Hungary: Ratings agency Fitch affirmed the sovereign rating at ‘BBB’ and kept a negative outlook. Fitch highlighted the rating as: “supported by strong structural indicators, including GDP per capita well above the peer median. These strengths are balanced against high public debt, a record of unorthodox economic policies, vulnerability to energy prices, and a worsening of governance indicators in recent years to closer to the 'BBB' median. The Negative Outlook reflects a greater-than-projected deterioration in public finances ahead of the April elections, low fiscal policy predictability and weak economic growth. The new government aims to reduce fiscal deficits over the medium term and will outline its strategy later in the year amid high existing expenditure commitments, particularly on social support, pre-election spending promises and an uncertain global environment.”

The statement suggests the decision doesn’t add too much emphasis on the new government plan. Thus, we expect an upward bias on the outlook. Potential further upgrades are contingent on the new government reform agenda.

Poland: S&P Dow Jones Indices is seeking feedback on reclassifying Poland from emerging market (EM) to developed market (DM), saying the country meets or exceed the criteria. Implementation would fall at the September 2027 reconstitution. S&P cited resilience amid inflation and investment delays, with deficits managed via revenue measures and EU inflows. Poland's weighting in the S&P EM basket is 1.27%, versus an estimated 0.15% in the DM basket. The move would be a milestone, though the smaller DM weighting underscores the index flow trade-offs involved.

Ukraine: President Volodymyr Zelenskyy invited Russia’s Vladimir Putin to talks in an open letter, offering Switzerland, Türkiye, or the “Arab world” and ruling out Moscow and Kyiv. The source sees little new beyond the format, given Zelenskyy has sought a meeting since 2021, and reads it as a signal to donors that he still seeks peace without major concessions.

Putin reiterated that Ukraine must cede all of the Donbas region and again ruled out European mediation, restating his preference for former German Chancellor Gerhard Schroeder, already rejected by Ukraine and the EU. The spokesman said Putin had not read the letter and that Zelenskyy should come to Moscow. Both sides remain defiant. Citing intelligence, Zelenskyy said Putin plans to continue the war in 2027 and 2028.

Central Asia, Middle East, and Africa

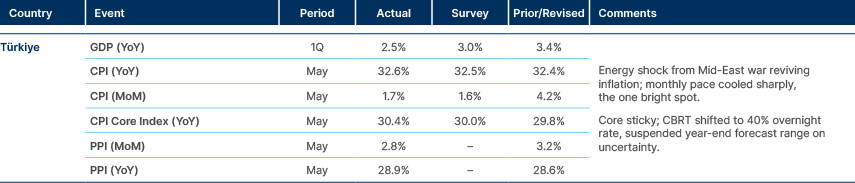

Türkiye’s core inflation remains sticky.

Pan-regional: The African Development Bank (ADB) launched a USD 7bn, five-year Integrated Aviation Transformation Programme in Brazzaville to modernise fleets, airports and logistics, with Nigeria the first to sign a national compact. The ADB says only 19% of intra-African flights use African carriers, with inefficiencies costing USD 50bn to USD 100bn a year.

Egypt: Remittance inflows jumped 62% yoy to a record USD 5.5bn in March, supporting the Pound during Iran war capital flight. However, the Saudi data shows a moderation in April, which should soften Egyptian inflows. Remittances rose 40% yoy to a record USD 41.5bn in 2025, c. 11.4% of GDP, after a 51% jump to USD 29.5bn in 2024. The gain reflects the March 2024 currency reform that liberalised the EGP and eliminated the black market premium.

Gabon: President Brice Oligui Nguema said IMF negotiations should conclude successfully once the public debt audit due this month is complete; a step needed before a new support programme. He said ties with Paris are “excellent” and announced a visit to France on 20 July and said the 2025 partial French troop withdrawal from Libreville followed a French request. Nguema rejected a US proposal to accept deported migrants and dismissed torture allegations by Sylvia Bongo, wife of former president Ali Bongo Ondimba, after her post-coup detention.

Ghana: Finance Minister Cassio Ato Forson revised the country’s 2026 growth outlook from 4.8% to 6.0% and said this could increase towards 10% should investments in the oil sector by Tullow and Kosmos yield the expected results. Gold and oil are driving the current account, and cocoa prices are rising after a massive decline in 2025.

Oman: The US pressed Oman to cut ties with Iran, the Wall Street Journal reported. Oman remained neutral through the US-Iran war, running a back channel that helped reopen Gulf flight corridors. The Trump administration reportedly threatened sanctions and strikes over an assessment that Muscat would join Iran in tolling Strait of Hormuz vessels, which Oman denies.

In other news, India and Oman brought a Comprehensive Economic Partnership Agreement into effect on 1 June, the Sultanate's most expansive trade pact. Oman grants zero-duty entry to 98% of tariff lines, covering over 99% of Indian exports by value, while India liberalises 78%. The pact also eases quotas for Indian professionals. It is Oman's first major independent pact since the 2006 US free trade agreement, and gives India deep-water access at Salalah and Duqm outside the Strait of Hormuz.

Senegal: Cheikh Diba formally took charge of the new Economy, Finance and Planning Ministry on 5 June, saying policy should be judged by its impact on citizens. The merger aims to integrate economic policy, resource mobilisation, planning and cooperation. Outgoing minister Abdourahmane Sarr urged continuity and defended a broader debt strategy attentive to regional markets.

The IMF said a mission will visit in the week of 15 June for technical talks on the macroeconomic outlook, financing needs and reforms, all needed to address significant debt vulnerabilities, IMF spokesperson Julie Kozack said. She declined to comment on possible debt restructuring or on the domestic political situation.

South Africa: Ratings agency Fitch upgraded South Africa by one notch to ‘BB’ with a stable outlook, bringing the headline rating in line with S&P (positive outlook) and Moody’s. Improved fiscal accounts with a primary surplus of 1% of GDP on average over the last four years, and structural reforms allowing for a stabilisation of debt/GDP, were the main reasons for the move. The fiscal surplus is expected to widen to 1.7% in FY2027.

President Cyril Ramaphosa pledged tougher action on illegal immigration while warning against xenophobia and violence. He promised more workplace inspections, prosecution of non-compliant employers, stronger borders and action on immigration corruption. Anti-foreigner protests have spread across Gauteng, KwaZulu-Natal and the Western Cape, with the group March & March setting a 30 June deadline for undocumented migrants to leave.

Several African countries warned their citizens after attacks on foreign nationals, with Ghana and Nigeria repatriating hundreds and Mozambique reporting deaths. Justice Minister Mmamoloko Kubayi said protests must stay peaceful and migrants should not be scapegoated. Official data put migrants at 3.1 million, or 5.1% of the population, with no reliable estimate of undocumented numbers.

Zambia: The government improved the cash tender offer on its 2053 bond to USD 843.5 per USD 1,000 and extended the deadline to 9 June (USD 740 after). The buyback will be financed partly by a USD 600m ADB loan, as part of post-restructuring debt management.

The bonds have a ‘clean-up call’ letting Zambia redeem all remaining bonds if 75% participate. This creates an incentive for market participants to tender at a higher price avoiding being ‘cleaned’ at 74c if more than three-quarters of the holders tenders the bonds. The government is trying to avoid increased financing costs as the instrument carries a step-up that could lift the coupon to 7.5% from 0.5% if Zambia meets an IMF sustainability metric over two reviews, possibly first tested in June 2026.

Developed Markets

Strong US labour market and elevated EU inflation kept global rates under pressure.

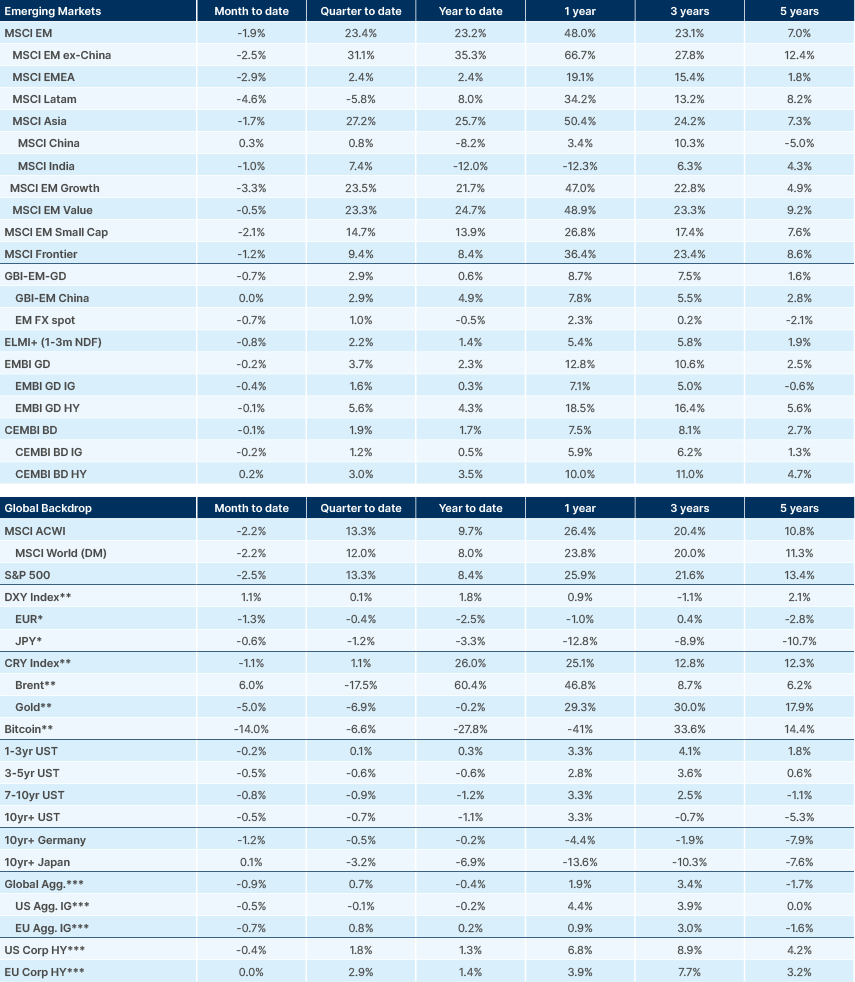

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. See https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm and https://press.spglobal.com/2026-06-04-S-P-Dow-Jones-Indices-Consultation-on-Treatment-of-MegaCap-Companies-Results