- Oil at USD 70 a barrel and softer US payrolls may signal peak hawkishness.

- Semiconductor rally takes a breather due to few negative narratives.

- Bank of Korea warned of risks from single stock ETFs.

- World Bank upgraded Vietnam to upper-middle-income status.

- Brazil’s central bank raised its 2026 inflation forecast from 3.9% to 5.2%.

- Colombia’s central bank hiked its policy rate by 75bps to 12.0%.

- Massive Russian strike on Kyiv killed at least 13 and injured dozens.

- Saudi Arabian crude exports returned to pre-war levels at 6.3mbpd.

- German cabinet likely to approve 2027 draft budget on Monday.

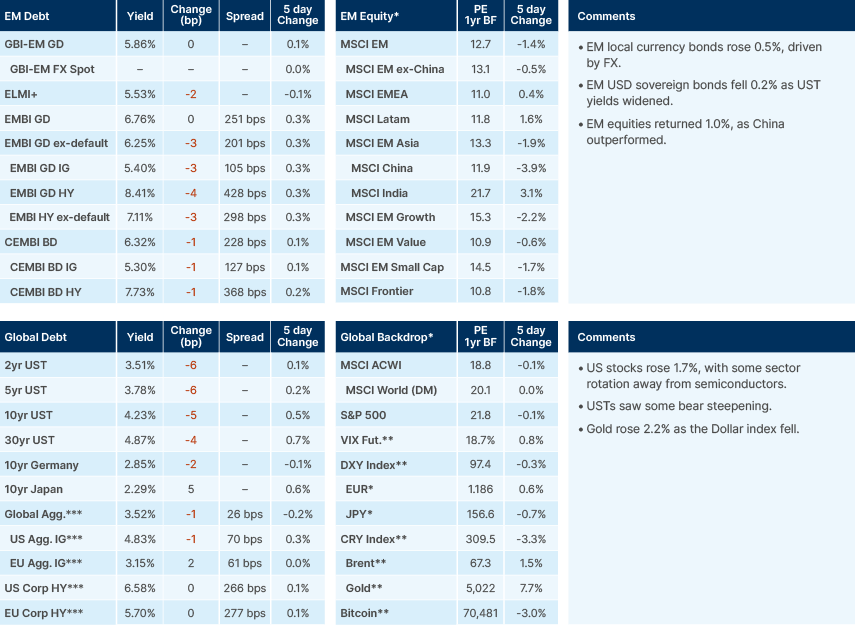

Last week performance and comments

Global Macro

As the fragile ceasefire between the US and Iran continues to hold, oil prices begin the week between USD 64 (Omani spot) and USD 72 (Brent first future). Oil prices below USD 75 in early July was not an outcome most analysts had as a base case just a month ago, and it has spurred a major reset of inflation expectations in bond markets, with the two-year US breakeven now trading below 2%, the lowest since October 2024. The corresponding rise in forward real interest rates as markets have also priced more hawkish US Federal Reserve (Fed) policy has very much dissolved the monetary debasement narrative that captured the zeitgeist last year, at least for now.

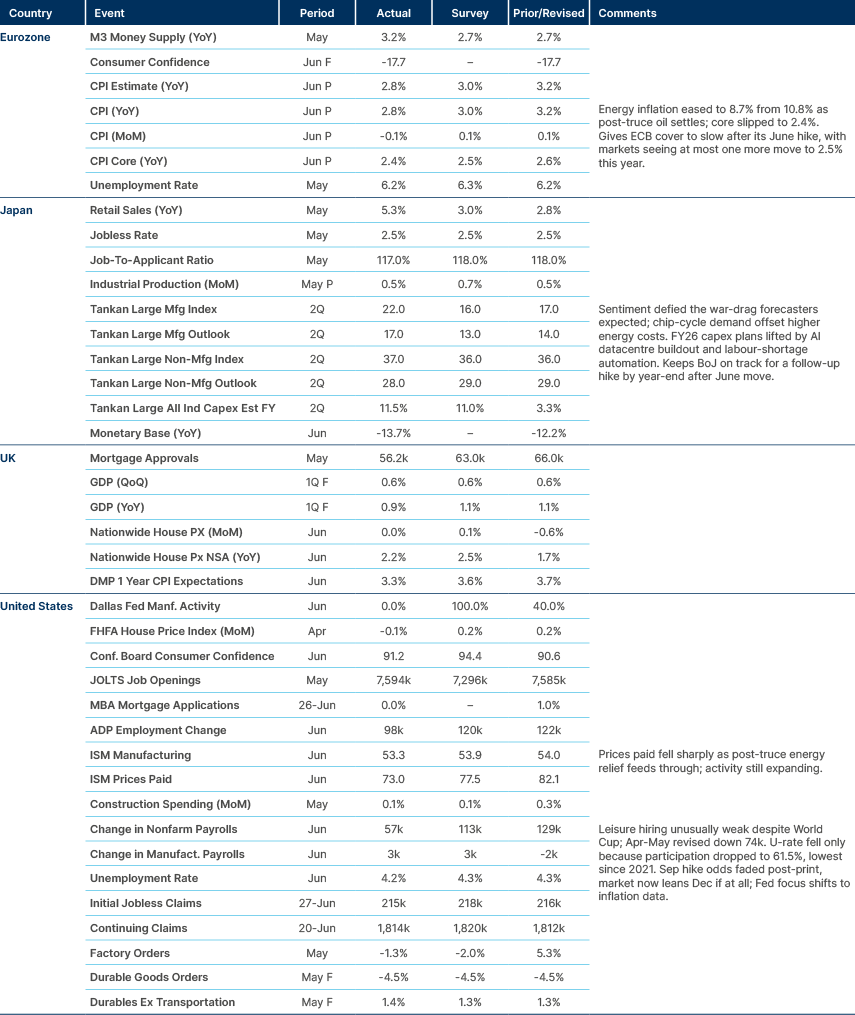

The key macro data point last week was non-farm payrolls. The headline number came in softer than expected at +56k. Private payrolls ex-healthcare and education came in negative for the first time since February. We flagged after the last print that while better jobs data this year is certainly a reality, under the hood the hiring has looked patchy and uneven across sectors. Moreover, a meaningful portion of it was likely linked to the FIFA World Cup, as well as the more sustainable AI capex trend. Despite the weak print, a shrinking workforce so far this year meant that the unemployment rate still fell, down to 4.2% now. But while there certainly is not much slack in the labour market, demand remains relatively weak, in our view. This is reinforced by wage inflation, which was flat at 3.5% yoy, thus below inflation over the last 12-month period.

Softer payrolls and oil prices back at nearly USD 70 a barrel may well signal a peak in central bank hawkishness for the time being with 30 basis points (bps) of tightening priced by markets by year-end. There may now be some value therefore in the front-end and the belly of the yield curve, but repricing will need to be triggered by softer inflation prints. A peak in hawkishness and more importantly, markets expectations of hawkishness may also lead to an unwind of some of the US dollar strength we have seen in recent weeks.

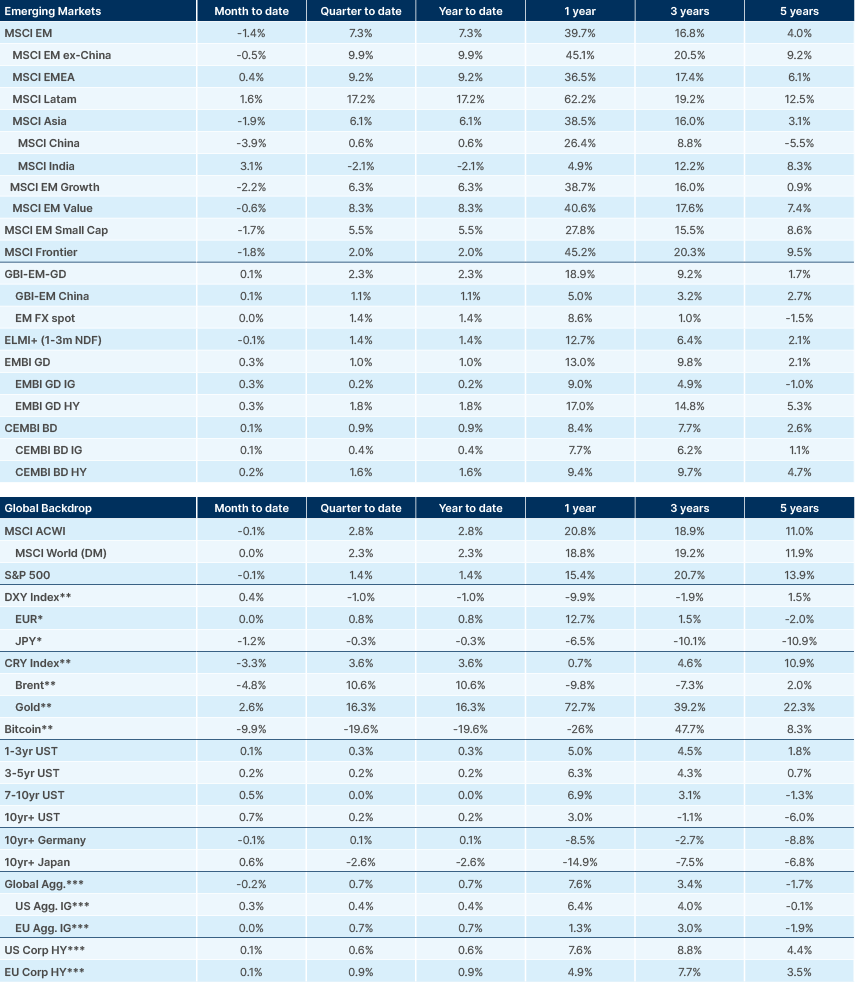

Another factor that may well pare the Fed’s hawkishness is a slowdown in the semiconductor-driven rally in US stocks. The S&P 500 had a weak month in June, down 1% and ticked lower again last week as volatility rose within the index. Semiconductor stocks saw a significant move lower, with the Philadelphia Semiconductor Index down nearly 12% on the week. Various shifts in the narrative are puncturing the extreme bullishness of recent months for the time being.

One is increasing government intervention in availability of the newest models. Another is the accelerating capabilities of cheaper Chinese models such as DeepSeek and corresponding gains in international market share. Chinese competition may make it more difficult for Anthropic and OpenAI to continue hiking prices. A third was the news from Meta last week that it will begin to sell excess compute. Investors have spun both bullish (demand high enough that renting compute is worth it because it’s so lucrative) and bearish narratives (Meta can’t find use case/more supply coming online) out of this.

In our view, none of these stories represent a meaningful concern to the durability of the AI capex trend, or the tightness of its related supply chains. Even so, the uncertainty alone has been enough to dent sentiment for now, especially with positioning in flagship semiconductor names, particularly memory chip makers, very heavy. A loss of momentum in the key driver of emerging market (EM) performance year-to-date (YTD) may slow gains for now. However, a rotation in performance leadership away from semiconductors and high beta names towards other areas of the index now offering significant value (such as India, Latin America, and Chinese tech) is overdue and would ultimately be healthy for the sustainability of the rally, in our view.

Geopolitics

US President Donald Trump will meet with Turkish President Recep Tayyip Erdoğan at 3:15pm local time in Turkey on Tuesday, according to Trump’s official White House schedule. On Wednesday, he will meet with NATO Secretary General Mark Rutte at 10:30am, Ukraine President Volodymyr Zelenskyy at 2:30pm, and Syrian President Ahmed al-Sharaa at 3:30pm.

Emerging Markets

Asia

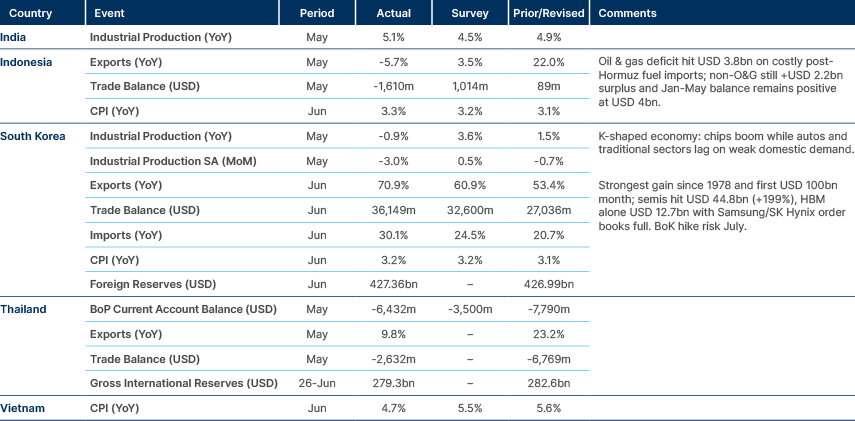

South Korean exports remain solid.

South Korea: China Business News reported on Saturday that Samsung plans to raise average third-quarter DRAM (dynamic random access memory) prices by around 20% from the previous three months, and has already verbally notified some customers. An unidentified consumer electronics manufacturer and a separate industry source both confirmed they had received notice of the planned increase. The move points to firming pricing power in memory as AI-driven demand continues to tighten supply.

The Bank of Korea (BOK) warned of the risks posed by single-stock leveraged exchange-traded funds (ETFs). In a written response to People Power Party lawmaker Park Sung-hoon, reported by Yonhap, BOK said: “With Samsung and SK Hynix accounting for more than half of stock market capitalization and trading volume, expanding investment in single-stock leveraged ETFs could further intensify this concentration”.

Presidential Chief of Staff, Kang Hoon-sik raised the prospect of a fund that would channel excess revenue from the chip industry into future growth. “We aim to make bold investments for the future, including supporting the three mega projects, creating future growth engines, addressing K-shaped polarization, and supporting housing, startups and jobs for those in their 20s and 30s”, he said.

The government, together with Samsung and SK Hynix, formalised a KRW 800trn semiconductor cluster in the country’s southwest, anchored by four memory fabrication plants. A new nuclear plant was endorsed to meet the cluster’s 6.3 gigawatt power requirement, although its water supply remains contested. Separately, SK Group and KKR will form Korea’s largest renewables company, targeting 10 gigawatts of capacity by 2031 to power AI data centres, while a new humanoid robot strategy aims to lift Korea’s global share to 20% from around 1% today. In domestic politics, Parliament approved Han Sung-sook as Prime Minister with 166 votes, in a session boycotted by the opposition People Power Party.

Taiwan: Hon Hai (Foxconn) reported that revenue grew 52% yoy in June, implying that sales for the June quarter rose almost 40% to TWD 2.5trn (around USD 79bn) on Bloomberg calculations. That was ahead of the TWD 2.4trn analysts had expected on average, underscoring the strength of AI server demand flowing through Taiwan’s contract manufacturers.

Vietnam: The World Bank upgraded Vietnam to upper-middle-income status after gross national income per capita reached USD 4,970 in 2025. Growth momentum remains strong: second-quarter GDP accelerated to 8.4% year-on-year, while in June industrial production rose 12.7% and retail sales 14.8%, and the trade deficit narrowed to USD 2.6bn. The reclassification is an important milestone, though over time it may erode Vietnam’s access to concessional financing.

General Secretary of the Communist Party, Tô Lâm, signalled a strategic shift in foreign direct investment (FDI) policy under Resolution 10, prioritising technology transfer and self-reliance over headline volume. Execution remains a weak point, however: public investment disbursement reached only 25.7% of the annual plan in the first half, well short of the 50% targeted by the end of the third quarter, prompting a zero-tolerance warning from Prime Minister Lê Minh Hùng over delays to transport projects.

Latin America

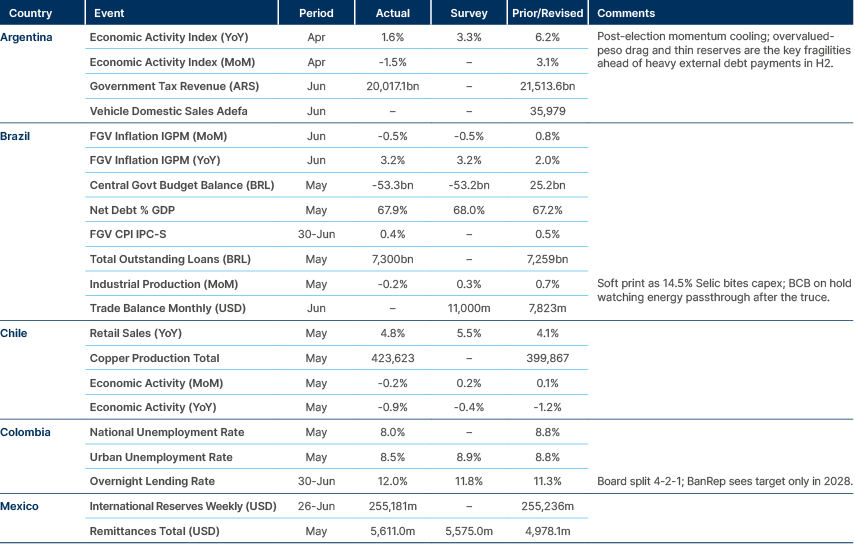

Activity softened in Argentina in April.

Argentina: Pampa Energia’s USD 4.5bn Rincon de Aranda project became the first upstream oil and gas entry into the Incentive Regime for Large Investments (RIGI), targeting output of 45k barrels per day in the Vaca Muerta shale formation by 2027. Approved RIGI projects now total USD 46.3bn, with a further USD 87.3bn under evaluation, including commitments from Glencore, Chevron and YPF. The pipeline underlines the regime’s growing traction as a magnet for energy and resource investment.

Brazil: Brazil’s central bank raised its 2026 inflation forecast from 3.9% to 5.2%, citing the output gap, conflict-driven fuel prices and higher inflation expectations. Inflation is now expected to breach the top of the target band, above the 4.50% ceiling, through end-2026, which would trigger a formal explanatory letter in October. After three cuts that brought the policy rate to 14.25%, the 4-5 August decision looks genuinely open. EmergingMarketWatch leans towards a hold, given continued fiscal stimulus and a tight labour market, though one further 25bps cut before pausing cannot be ruled out.

Colombia: Colombia’s central bank raised its policy rate by 75bps to 12.0% on 30 June, more than markets had expected, in a three-way 4-2-1 split. Tightening now totals 275bps this year, running sharply against the regional easing trend, with inflation at 5.8% and expectations above target across all horizons. The seasonally-adjusted unemployment rate hit a record low of 8.1% in May, although public-sector hiring accounted for 1.7 percentage points of the job growth.

President-elect Abelardo de la Espriella named Miguel Gomez-Martinez, a pro-market conservative, as Finance Minister. The initial read is market-positive, though the reaction is likely capped until the head of public credit is also named. Interest costs are projected at 3.9%-4.6% of GDP in 2027, with TES government bonds clearing at yields of 13%-14%. De la Espriella’s pledged cuts of 700k state jobs would, if delivered, threaten the very labour market strength currently underpinning the central bank’s hawkish stance.

Central and Eastern Europe

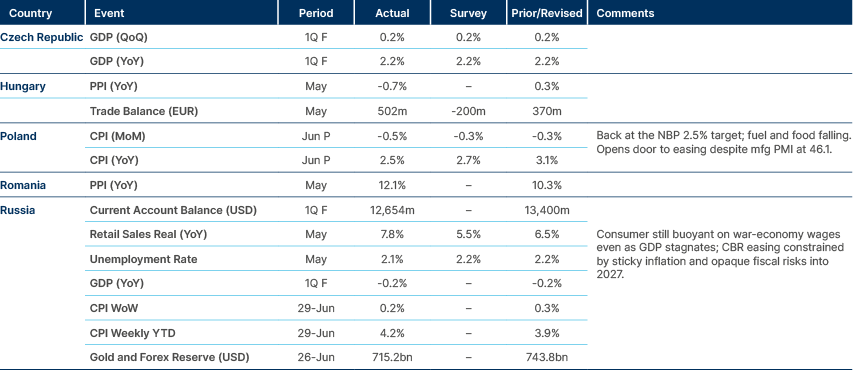

Inflation surprised to the downside in Poland.

Czech Republic: The Czech National Bank’s Deputy Governor Eva Zamrazilová characterised June’s 25bps rate hike as fine-tuning rather than the start of a new cycle, citing core inflation near 3%, strong services-sector wages and excess credit growth. EmergingMarketWatch doubts a 3.75% policy rate is restrictive enough, and expects a further 25bps hike in either September or November.

Hungary: The government scrapped the fuel price cap on 26 June. Retail prices fell only modestly, with gasoline easing to HUF 580 from the HUF 595 cap, implying little relief for June inflation. The Economy Minister retains the option to reimpose measures should prices exceed the regional average.

Poland: National Bank of Poland Governor Adam Glapiński put the central bank’s unrealised gold profit above PLN 150bn at end-May, down from PLN 193bn in February, and renewed his call for a cross-party deal to sell gold to fund defence spending. The plan remains blocked by the standoff between the government and President Karol Nawrocki. A modified bill may reach the Sejm in July, but any realised profit would only feed into the budget in mid-2027, just before the elections.

Romania: The CFA Romania macroeconomic confidence index fell 7.7 points to 30.5 in May, close to record lows. One-year inflation expectations rose to 7.53%, with the RON seen at 5.35 to the EUR in a year’s time. The 2026 growth outlook was cut to a marginal contraction, and the head of CFA Romania warned of stagflation, arguing that only spending cuts can resolve a deficit-driven inflation problem, with the fiscal gap running at 6.2% of GDP.

Ukraine: A large-scale Russian strike on Kyiv killed at least 13 people and injured dozens, damaging more than 20 residential buildings. Attacks of this kind now recur every two to three weeks. Despite the pressure, support for European Union (EU) membership rose to 70% and for NATO to 63% in June polling, helped by the opening of the first cluster of EU accession negotiations and the EUR 90bn support package.

Central Asia, Middle East, and Africa

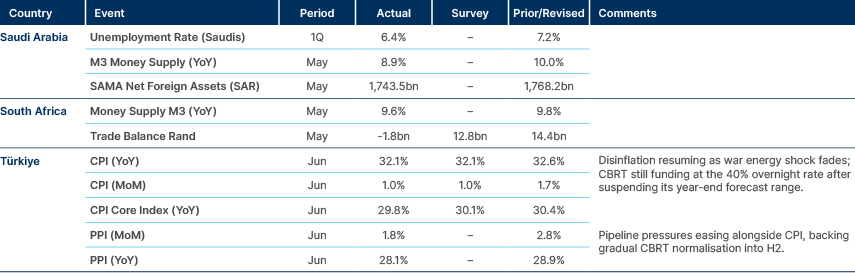

Saudi unemployment rate declined in Q1 2026.

Kuwait: Crude output recovered to 1.65 million barrels per day (mbpd) in June from just 580,000 in May, reaching 1.9mbpd in the final ten days of the month as the reopening of the Strait of Hormuz restored maritime routes. All force majeure notices have now been rescinded. With Brent crude trading near USD 72, July output should rise further.

Nigeria: The World Bank is backing Nigeria’s 2026-2032 development plan with USD 1.25bn in financing aimed at spurring job creation and private investment.

Separately, an International Monetary Fund (IMF) official said that Nigeria’s unreported spending equals around 2% of GDP, underlining persistent gaps in fiscal transparency.

Saudi Arabia: Crude exports returned to pre-war levels at 6.3mbpd over the six days to Wednesday, according to Bloomberg tanker data, up from 4.45mbpd in June, as loadings resumed at Ras Tanura and flows from Yanbu continued. If sustained, these volumes would support oil revenues in the third quarter.

South Africa: The new Democratic Alliance leader, Geordin Hill-Lewis, sharpened his attacks on the African National Congress (ANC) over Black Economic Empowerment, the National Health Insurance scheme and the Basic Education Laws Amendment Act, while reaffirming his party’s commitment to the Government of National Unity (GNU), as he courts some six million undecided voters ahead of the 4 November local elections. Hill-Lewis claims the ANC now polls below 50% across all demographics, and recent by-election trends point to the party possibly falling below 40%.

UAE: Abu Dhabi’s dual-tranche Dollar benchmark drew more than USD 11bn in orders, with initial price thoughts of 50bps over US Treasuries for the five-year tranche and 55bps for the ten-year. The proceeds will fund diversification efforts, including AI chip manufacturing, and the deal re-establishes a liquid sovereign yield curve that local issuers can price against.

Developed Markets

US payrolls softer than expected. Softer inflation in Europe. Japan activity solid.

Germany: The German cabinet is likely to approve the 2027 draft budget on Monday, with EUR 203.6bn in new borrowing, above the EUR 196.5bn flagged in April, Reuters reported over the weekend. The increase reflects higher defence and investment spending. New borrowing would comprise EUR 118.7bn in the core budget, EUR 54.9bn from the infrastructure fund and EUR 30bn from a special defence fund. Core defence spending is set to rise to EUR 109bn from EUR 82.2bn this year, while total investment climbs to EUR 117.5bn from EUR 78.9bn in 2025, and overall spending rises 5.9% year-on-year to EUR 555.4bn.

Japan: Nikkei published a follow-up overnight on the government’s US-style ‘DOGE’ efforts. This is a Cabinet Office unit, established in November 2025 under Finance Minister Satsuki Katayama, and modelled on the US Department of Government Efficiency, tasked with reviewing policy tax breaks and subsidies and eliminating ineffective programmes to create fiscal space. The government had previously cited savings from the initiative as a potential funding source for its proposed consumption tax cut, and as a means of honouring its pledge not to rely on additional deficit-financing bond issuance.

United Kingdom: A group of economists, including Andy Burnham adviser Jim O’Neill, urged the next UK government to consider a sweeping tax overhaul to revive weak growth, warning that “incrementalism will not fix Britain.” The letter said that proposals in the University College London report, which include scrapping stamp duty and council tax, cutting income taxes for most workers, and introducing a 1% annual property value tax, merited serious consideration, while stopping short of endorsing them. The report argued the reforms could be delivered without higher borrowing, creating a GBP 38bn fiscal buffer.

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. As at latest data available on publication date.

*EMBI GD and EMBI GD HY Yield/Spread ex-default yields and spreads calculated by Ashmore. Defaulted EMBI securities includes: Ethiopia, Ghana, Lebanon, Sri Lanka, and Venezuela. **Price only. Does not include carry. ***Global Indices from Bloomberg. Price to Earnings: 12 months blended-forward.

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.