- Ceasefire between US and Iran at its most strained point yet.

- Global oil inventories still high in headline terms, but operational stress is close.

- G4 central banks remain on hold, for now. Monetary policy diverges across EM.

- Bank Indonesia signalled it will step up FX market intervention.

- Moody's shifted Vietnam's sovereign outlook to Positive from Stable.

- Brazil’s central bank delivered a unanimous 25bps cut to 14.50%.

- Venezuelan oil production has recovered further with exports averaging 1mbpd since March.

- Kazakhstan’s central bank is considering a rate cut in June.

- UAE surprised markets after announcing it would leave OPEC+ from 1 May.

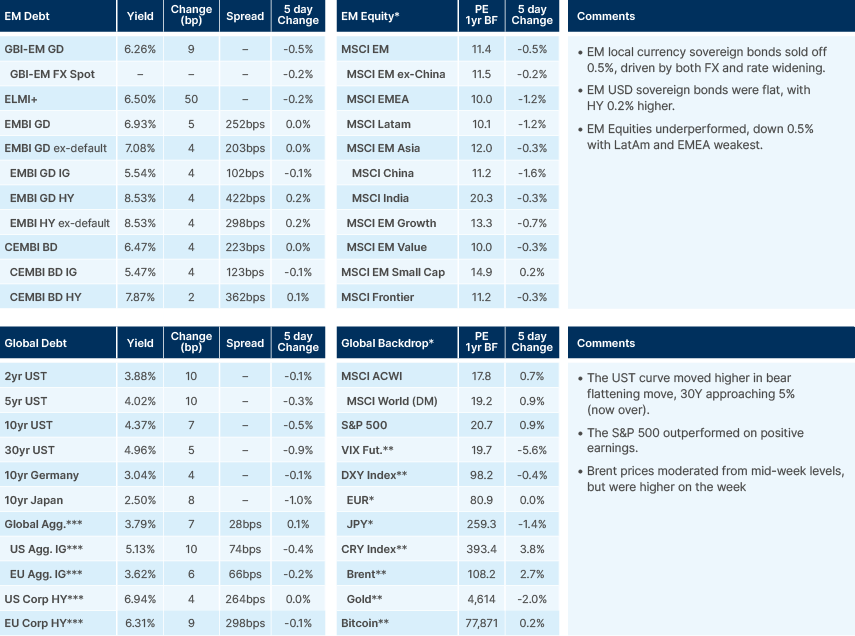

Last week performance and comments

Global Macro

Towards the end of last week and over the weekend, news flow around the US/Iran conflict and ongoing negotiations had been relatively benign. Last Friday, the US submitted a counterproposal to Iran for a permanent ceasefire, and on Saturday, news of meaningful nuclear concessions from Iran filtered through. On Sunday, however, the mood soured with US President Donald Trump casting doubt on whether a deal would be achieved, threatening escalation and launching “Project Freedom”, a military escort initiative to help stranded vessels exit the Persian Gulf.

Most analysts argue that, given the very low risk tolerance from most tankers, “Project Freedom” is unlikely to provide a meaningful release valve for the Strait of Hormuz bottleneck. Nevertheless this, together with the ongoing (partial) enforcement of the US navy’s blockade on Iranian exports, led to renewed Iranian attacks in the Gulf yesterday. Targeted locations included the oil terminal at Fujiarah, which was hit by drones. The US military also said it fought off attacks from Iranian drones, missiles and small boats, as two US warships crossed Hormuz along with two US-flagged merchant vessels. US Defence Secretary Pete Hegseth is holding a press conference today with the Chairman of the Joint Chiefs of Staff, General Dan Caine. The Iranian Foreign Minister said "there's no military solution to a political crisis", and suggested talks with the US were “making progress with Pakistan's gracious efforts.”

Headline global oil inventories remain high, at around 8 billion barrels, according to JP Morgan. However, operationally, significant stress is not far away. Like blood pressure in the human body, the global oil supply system needs a minimal level of reserves to operate before it begins to break. This level is quite high; JP Morgan (JPM) estimates this point at around 7.6 billion barrels, and expect this level to be breached in June at the current run rate of inventory drawdowns. At this point, product shortages begin to become more likely, and product prices increase meaningfully as refiners compete more aggressively for barrels.

Since the conflict began, commercial inventories, particularly in developed markets, have been somewhat protected by drawdowns in volumes of oil in transit, oil in floating storage (including sanctioned Russian vessels) and releases from government stockpiles. However, excess oil in transit and excess floating storage is now minimal. JPM argues that although the International Energy Agency (IEA) and government mandates Strategic Petroleum Reserve (SPR) releases will continue, it will not be enough to prevent commercial inventories reaching “operational stress” levels by mid-June. To be clear, the JPM figures refer to global stress levels, particularly across OECD countries. Various demand elastic smaller countries with low inventory levels have already made major demand adjustments, including widespread industry closures in countries such as Sri Lanka.

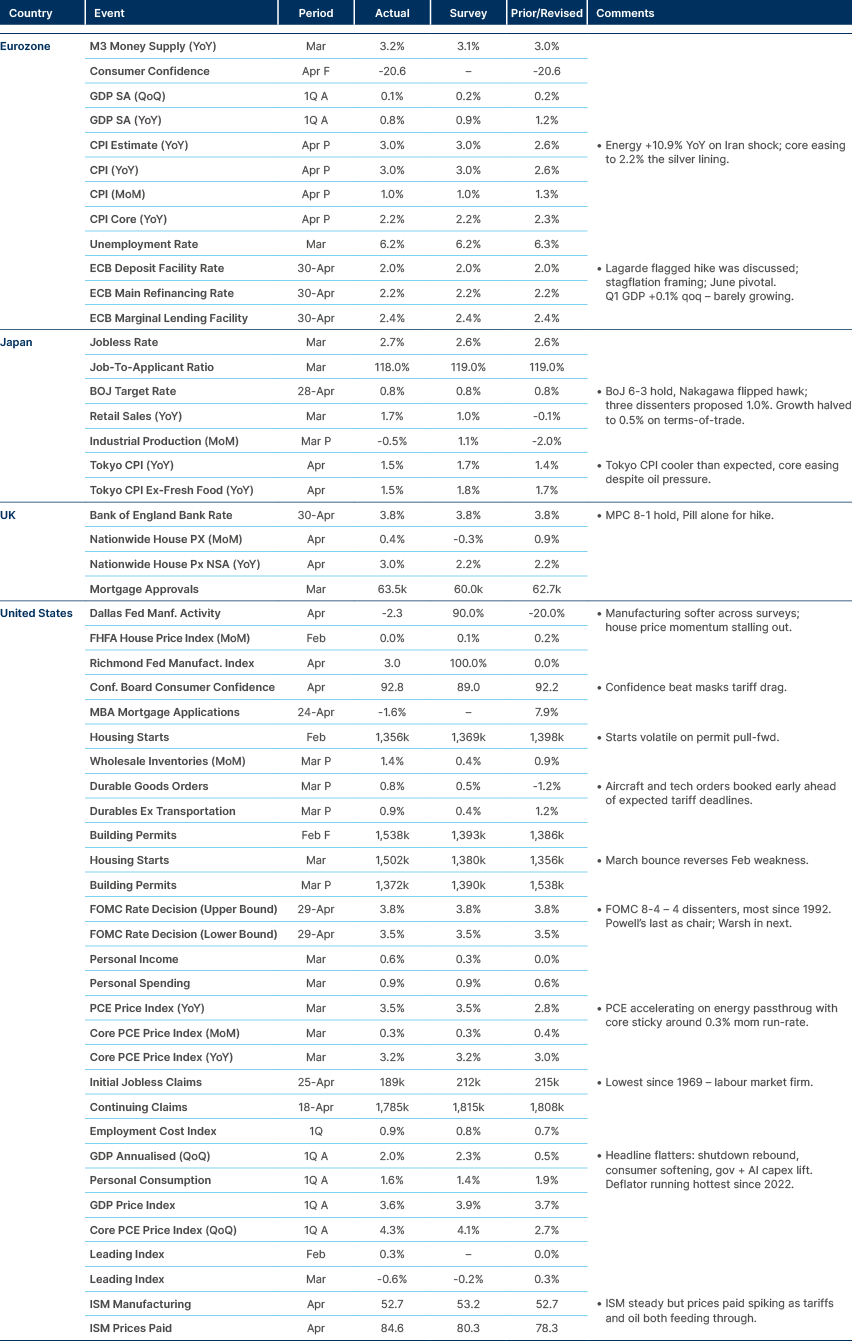

Last week each of the G4 countries held interest rates, but the energy shock has clearly reset the trajectory. The US Federal Reserve (Fed) held with only Stephen Miran dissenting by calling for a cut, while three regional directors objected to including an easing bias in the statement. The bigger story was Fed Chair Jerome Powell signalling he will stay on as Governor through 2028, the first outgoing Chair to remain on the board since Marriner Eccles in 1948. The European Central Bank (ECB) kept its main policy rate at 2.0%, but moved meaningfully more hawkish, with President Christine Lagarde flagging June as the right time to assess; a hike is now around 90% priced. The Bank of England (BoE) vote of eight to one to keep rates on hold disguised a notably dovish press conference, with BoE Governor Andrew Bailey citing a loosening labour market and limited corporate pricing power. However, he stopped short of ruling out hikes if the energy shock persists. The Bank of Japan (BoJ) held rates by a six to three vote, the most hawkish split of Governor Kazuo Ueda’s tenure, alongside a stagflationary Outlook Report (FY26 core consumer price index (CPI) inflation raised to 2.8% from 1.9%, FY26 GDP cut to 0.5% from 1.0%) and the market now prices around 65% odds of a June hike.

The common thread is that core inflation pass-through from the energy shock has so far remained limited. The hawkish signalling reflects insurance against second-round effects rather than a response to data already in hand.

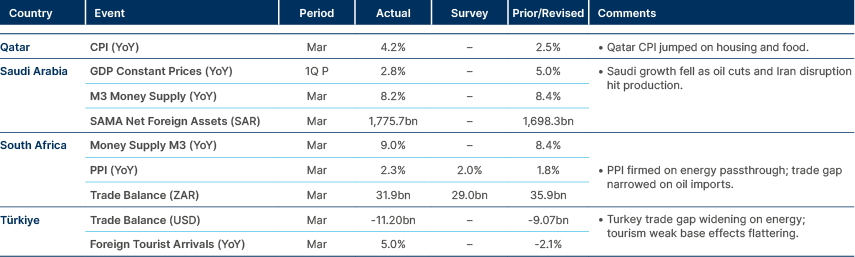

Emerging market (EM) central banks are diverging. Most held rates in April: Türkiye at 37% (hawkish revision expected at the 14 May Inflation Report), South Africa at 6.75% (modelled path now sees one 2026 cut vs two), Indonesia at 4.75% for a seventh meeting, India on a clean "wait and watch" pivot, and Colombia at 11.25% against consensus for a 50-100 basis points (bps) hike. Two countries have already hiked: Pakistan +100bps to 11.50% (its first move since June 2023) and the Philippines +25bps to 4.50% (first move in over two years), both pre-emptive against energy-driven pass-through. Cuts were LatAm only: Brazil -25bps to 14.50%, and Mexico signalling another cut in May, possibly the last this cycle. A continuation of high oil prices will likely tilt more emerging markets hawkish, however, most EM central banks are still running high real interest rates, which provides a healthy buffer against the need to react aggressively, like in 2022.

Emerging Markets

Asia

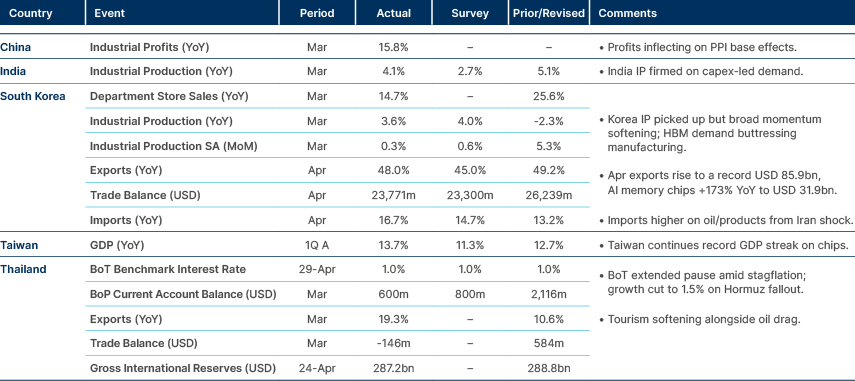

Korean exports remain solid as China’s industrial profits increased.

Indonesia: Bank Indonesia indicated it will step up efforts to defend the rupiah, with the monetary policy department director defending the strategy against accusations it merely burns reserves. The triple-intervention framework — spot, domestic non-deliverable forward (NDF) and secondary market bond purchases — remains in place. The Rupiah has weakened around 3.5% YTD against the dollar and is now trading in the USD/IDR 17,200–17,300 range, having broken below the psychological 17,000 mark. With FX-only tools showing diminishing returns, we think a policy rate hike in May or June is increasingly likely.

Philippines: Philippines central bank (BSP) Governor Eli Remolona indicated that it stands ready to deliver further hikes to anchor inflation expectations and head off second-round effects. The base case is a sequence of small 25bps moves, conditional on the magnitude of Iran spillovers, which Remolona described as still modest. The Monetary Board hiked the reverse repurchase (RRP) rate by 25bps to 4.50% last week — the first rate increase since October 2023. Growth guidance was nudged to 4.5–4.6% for 2026 (from 4.4%), still well below the 5.0–6.0% government target, with a 6% pickup expected in 2027. Remolona emphasised the BSP does not target a USD/PHP level and downplayed the 60 threshold, while noting Middle East remittance flows have held up.

South Korea: Bank of Korea (BOK) minutes for April revealed a notably more hawkish board than at the February meeting. While the 2.50% hold was unanimous, three of six members now lean hawkish on our reading of the comments and only one sounds dovish. The board flagged non-linear effects from the energy shock and the risk that elevated inflation expectations become entrenched, with CPI inflation expected to stay materially above the prior 2.2% objective. Growth was revised below the previous 2.0% projection, with the board describing a deepening ‘K’-shape — IT and semis hitting record exports on AI-related demand, while non-IT, consumption and construction remain weak. We now think the next BOK move is more likely a hike than a cut.

Separately, Seoul expects to secure up to 90% of pre-war naphtha import volumes for May, easing pressure on the petrochemical complex. Yeochun NCC has lifted operating rates to 65% (from 55% on April 1) and Korea Petrochemical to 72% (from 62%). The government is injecting KRW 674.4bn to subsidise up to half the gap between pre-war and current import prices over April–June, while Korea has locked in 2.1 million tonnes of naphtha from Middle East producers including Oman and Saudi Arabia — roughly one month of demand at last year's usage rate.

On his state visit to Hanoi, President Lee Jae Myung called for a substantially deeper Korea-Vietnam economic partnership, framing supply chain resilience as the strategic priority. Lee highlighted Vietnam's sixth-largest global rare earth reserves and its status as Korea's top urea supplier in 2024, and pushed for joint development of liquified natural gas (LNG_ and nuclear power capacity in Vietnam). Daewoo E&C and other Korean firms pitched smart cities, transport and nuclear projects in closed-door sessions, with Korea aligning around the Ninh Thuan 2 nuclear bid.

Vietnam: Moody's shifted Vietnam's sovereign outlook to Positive from Stable while affirming the country’s ‘Ba2’ rating, citing institutional reform progress and a reduced probability of adverse US trade actions versus prior expectations. Administrative consolidation, ministry restructuring and project approval reforms initiated in late 2024 have begun delivering measurable improvements in coordination and efficiency. Core credit strengths remain intact and have supported Vietnam through the recent energy and freight shocks. These are an export base, recovering domestic demand, sustained foreign direct investment (FDI) inflows, low and stable government debt and reduced external financing. Banking sector risks and real estate vulnerabilities remain the binding constraints on a full upgrade.

Latin America

Colombia kept is policy rate unchanged due to political pressure.

Argentina: The Mining Secretariat projects mining exports doubling to USD 15.4bn by 2030 from USD 7.7bn in 2026, and surpassing USD 30bn by 2034. Gold leads near-term at USD 5.2bn this year, with lithium (USD 1.5bn) and silver (USD 1.0bn) supporting. The growth profile flips from 2030 as nine copper projects come online, with copper exports projected to reach USD 16.3bn by 2034 from effectively zero today. The forecast assumes USD 56bn of investment to develop new projects and expand existing ones, covers projects at preliminary economic assessment stage or later, and excludes 13 advanced-exploration copper projects. Mining is positioned to become the next major export industry behind oil and gas, though the projection hinges on commercial conditions remaining favourable and Argentina avoiding a return to interventionist macro policy, in our view.

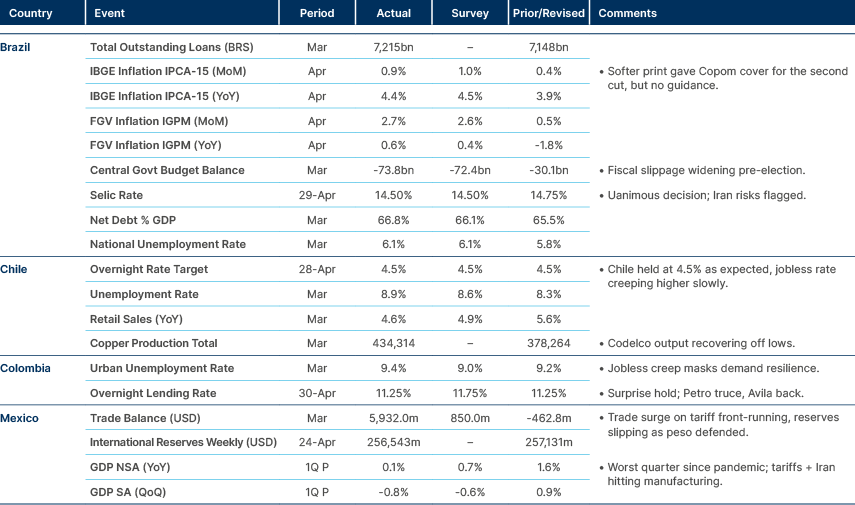

Brazil: The Central Bank of Brazil’s Monetary Policy Committee (Copom) delivered a unanimous 25bps cut to 14.50%, the second consecutive move, and explicitly attributed the room to manoeuvre to the prolonged restrictive stance maintained through 2025. Copom withheld forward guidance, framing further moves as data-dependent and contingent on clarity around the Middle East energy shock. The 2026 inflation forecast was raised to 4.60% from 3.90%, breaching the 4.50% upper tolerance band, while end-2027 was held at 3.50%. The risk balance was kept numerically even but recalibrated, with second-round effects from the energy shock added to the upside risks (de-anchored expectations, services inflation, FX) and the downside risks (sharper domestic slowdown, global deceleration, falling commodity prices). The statement was not hawkish enough to telegraph a pause, so we view another 25bps cut as the base case for the next meeting. However, a June pause cannot be ruled out depending on the energy shock evolution and the government's mitigation measures.

An Atlas poll has President Lula tying Flávio Bolsonaro 47.5% vs 47.8% in the runoff scenario, an improvement on the March survey where Lula trailed. Lula's approval ticked up to 46.8% (from 46.0%) and disapproval fell to 52.4% (from 53.5%). Lula extended his first-round lead over Flávio to 6.9pp from 5.8pp.

Chile: The government has said it will send Congress a 4.0% minimum wage hike for the May annual revision, in line with central bank inflation projections, despite lacking sign-off from the CUT labour federation, which had opened with 18.3%. The proposal frames the adjustment as preserving real wages after large recent hikes, particularly given the cost pressures from working time and pension reforms now feeding through.

President José Antonio Kast committed publicly to keeping the 12.5% SME corporate income tax rate permanent, after the People's Party threatened to vote against the omnibus bill. The pandemic-era cut from 25% to 10% had been raised to 12.5% in 2023 and was scheduled to step up to 15% in 2029 and back to 25% in 2030. The omnibus fiscal cost calculations had already assumed those scheduled hikes, so locking in 12.5% creates a long-term revenue gap not captured in current projections.

Colombia: The central bank of Colombia (BanRep) held the policy rate at 11.25%, formally describing the unanimous decision as reached "by consensus" while explicitly noting board members held diverse opinions on monetary policy — language that suggests unanimity was constructed rather than spontaneous. The statement laid out a hike-justifying backdrop: March CPI inflation rose to 5.6% (46bps above end-2025), core ex-food-regulated rose to 5.8% (~80bp above end-2025), end-2026 survey expectations rose again, and the bank flagged Iran-related risks to energy, fertilisers and imported goods alongside firmer Q1 high-frequency activity and a tight labour market.

A CNC poll for Cambio puts left-wing candidate Iván Cepeda at 37.2% in the first round, ahead of hardline-right Aberlardo de la Espriella (20.4%) and Uribista Paloma Valencia (15.6%). The more important signal is Cepeda's ceiling: his rejection rate has hit 32.7% and his runoff margins have collapsed from 55% to 37.9% versus de la Espriella, and from 57% to 40% versus Valencia. The right remains fragmented, with de la Espriella retaking second from Valencia after the latter's primary-driven momentum faded. The blank/undecided pool sits at 16.6%, the highest in a year, and historically activates against high-rejection candidates.

Venezuela: Oil production recovered further with exports averaging 1 million barrels per day (mbpd) since March. March-April monthly gross oil revenues estimated at about USD 2.5bn. Chevron CEO Mike Wirth said Chevron should be fully paid off in Venezuela at some point in 2027, and that the company would provide updates on what the model would be for cash distributions going forward.

Central and Eastern Europe

Hungary held rates in first meeting post government transition.

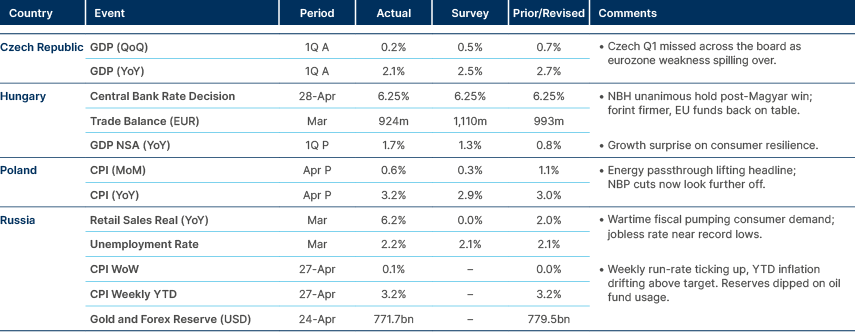

Czech Republic: CNB Deputy Governor Eva Zamrazilová told Bloomberg the next policy move is most likely a hike, though there is no need to rush. She characterised the risk of policy error from holding rates steady as "near zero," with headline inflation expected to remain inside the 2%+/-1pp tolerance band through end-2026 and limited evidence of second-round effects from the Iran conflict. Notably, Zamrazilová flagged food prices as a bigger concern than core inflation. Persian Gulf countries are major ammonia fertiliser producers and the Hormuz blockade is pushing fertiliser prices up 20-30%, which will eventually feed through to food. She expects GDP growth weaker than the CNB's 2.9% forecast, but not as low as the Finance Ministry's 2.1%. The comments effectively pre-commit the 7 May meeting to a hold and push the difficult decision to 18 June, by which point food price dynamics and second-round effects may be clearer.

Hungary: Outgoing PM Viktor Orbán offered to step down as Fidesz leader at the party's national executive committee meeting, taking responsibility for the heavy election loss to the Tisza Party. The committee declined the resignation, with Orbán indicating he would continue if elected by the 13 June Party Congress. The party blamed the loss on collective and individual responsibility while publicly placing primary responsibility with Orbán. Fidesz nominated former government spokeswoman Eszter Vitalyos for Deputy Parliamentary Speaker after Tisza rejected outgoing foreign minister Péter Szijjártó over his ties to Russia. Tisza's Agnes Forsthoffer will hold the Speaker role. Orbán also confirmed he will not take up his MP seat despite topping Fidesz's national list, framing it as a sacrifice to focus on party reorganisation. Other senior Fidesz and KDNP figures also surrendered their mandates, including Deputy Leader Lajos Kosa, KDNP Leader Zsolt Semjén, Deputy Speaker János Latorcai, Miklós Soltesz and Erik Banki, also surrendered their mandates.

Kazakhstan: NBK Deputy Governor Akylzhan Baimagambetov said the central bank may consider a rate cut in June, conditional on consistent moderation in inflation. CPI inflation eased to 11% yoy in March from 11.7%, but remains well above the medium-term target. The Deputy Governor flagged utility tariff hikes, fuel prices, external volatility and ongoing absorption of this year's VAT reform as continuing inflation pressures, pushing back against earlier bank claims that the tax reform impact had been fully digested. Tenge strength may be masking these pressures. Macro forecasts will be refreshed in June. We think the central bank is leaning cautious and may push easing into H2.

Poland: Central bank (NBP) voting records for the March 25bps cut show a second dissenter joining hawk Joanna Tyrowicz. Henryk Wnorowski also opposed the cut, taking the vote to eight to two versus the nine-to-one splits seen on prior cuts. The other eight members including Adam Glapinski and new appointee Marcin Zarzecki backed the move. Zarzecki's vote is somewhat surprising given the Iran war had just begun. Tyrowicz again motioned for a 75bps hike, which was rejected. The March split is largely irrelevant going forward, All members including Tyrowicz now back rates on hold given the Iran-driven inflation jump and uncertainty, with the next move likely deferred until at least July and dependent on the energy price trajectory.

Romania: The CFA Romania macro confidence index slumped 10.2 points in March to 38.2, with both current conditions and expectations components weakening sharply on the oil shock and broader risk aversion. Inflation expectations for the next 12 months jumped 1.72pp to 7.61%, with 47% of analysts expecting further increases versus 37% expecting a decline. Around 86% of analysts expect the leu to weaken over the next 12 months, with the average forecast at EUR/RON 5.1303 in six months and 5.1644 in 12 months. The deterioration reflects concerns about Romania's external position and regional spillovers from the energy shock.

Central Asia, Middle East, and Africa

Saudi Arabia GDP growth contracting due to Iran shock.

South Africa: Iran has reportedly offered crude oil supply to South Africa, with the proposal communicated to the Department of Mineral Resources and Energy in April, according to officials cited by Business Day. The Iranian embassy confirmed it stood ready to respond to requests from friendly countries. The Energy Department declined to comment and the government has given no signal it intends to accept. South Africa halted Iranian crude imports in 2012 under tightening sanctions and has since diversified its supply base toward Nigeria and Angola. US secondary sanctions create material risk to any renewed deal — restricting access to dollar payment rails, shipping and insurance — and US-SA relations are already strained by Pretoria's diplomatic engagement with Iran.

Turkiye: Q1 foreign tourism income rose 4.2% yoy to USD 9.9bn, driven by a 1.5% rise in visitor numbers, a 2.4% increase in per capita spend to USD 1,022 and a 2.7% rise in nightly average to USD 102. Food and drinks accounted for 27% of revenue, international transit 15.8% and package tours 13%, with package tour spending up 12.6%. Outbound spending by Turkish residents fell 9.1% to USD 2.2bn despite 13.1% more travellers, with per capita spend collapsing 19.7% to USD 758 — a function of high base effects and tight monetary policy squeezing discretionary budgets. Local reports flag a Q2 reservation drop tied to the Iran conflict, which will likely weigh on summer-season revenue and add pressure to the current account.

United Arab Emirates: The US and UAE are discussing a potential currency swap line to bolster dollar liquidity in global funding markets, raised by UAE Central Bank Governor Khaled Mohamed Balama with US Treasury Secretary Scott Bessent and Fed officials during recent Washington meetings. Bessent defended the proposal before the Senate Appropriations Committee, framing it as a tool to prevent disorderly US asset sales and maintain dollar funding order, and rejecting bailout characterisations from Senator Chris Van Hollen. The Fed would ultimately decide. The arrangement would extend swap-line architecture beyond traditional major central bank partners — a notable expansion of "dollar diplomacy" that could reshape global liquidity networks if implemented, with other Gulf and Asian allies reportedly expressing similar interest.

The UAE surprised markets by announcing it would be leaving OPEC+ effective 1 May, after being a member since 1967. Pre-conflict output of ~3.3-3.5mbpd could increase to as high as 5mbpd, when Hormuz reopens.

Developed Markets

Central banks across DM remain on hold.

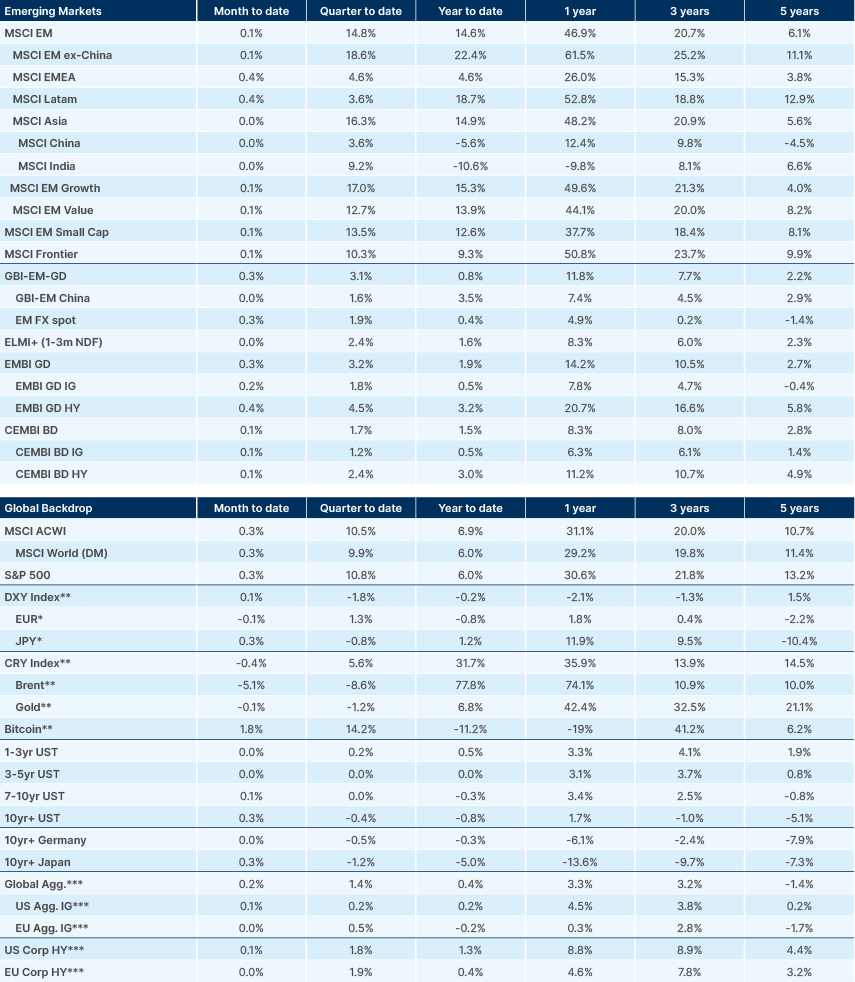

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.