- Oil prices fell due to rising hopes of a US/Iran deal, but no breakthrough yet.

- The US continued strikes on military targets around Hormuz.

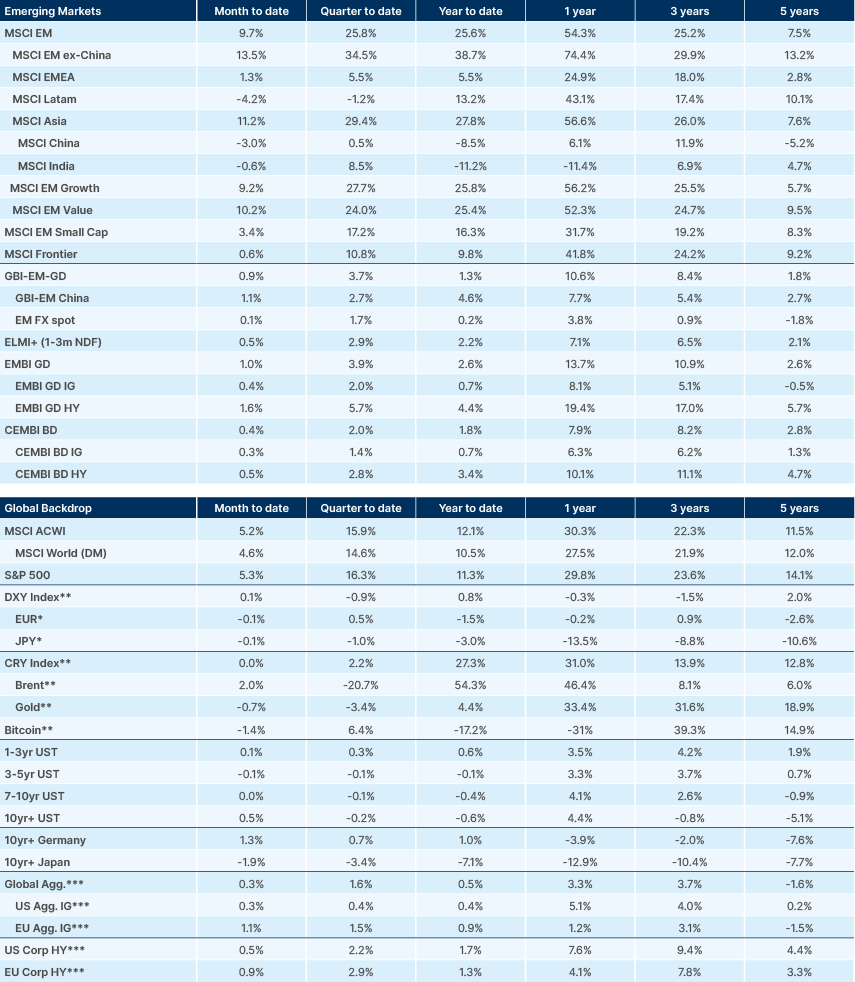

- EM assets posted solid returns for May.

- Samsung averted a strike after agreeing a deal with its union.

- Argentina’s Economy Minister Caputo predicts Milei will win re-election comfortably in 2027.

- De La Espriellla won 44% in Colombia’s first-round election, setting up a runoff with Cepeda.

- With Peru’s runoff election three weeks away Fujimori leads Sanchez by 3% in the polls.

- US President Trump hosted Brazilian presidential contender Flavio Bolsonaro in Washington.

- Poland signed first 40 contracts under the EU’s SAFE defence programme, worth PLN 100bn.

Last week performance and comments

Global Macro

US President Donald Trump held a Situation Room meeting on Friday to make a "final determination" on signing a 60-day extension to the ceasefire between the US and Iran. However, the two-hour meeting ended without a decision. On Sunday, the BBC reported that Trump is pushing for changes in the memorandum around both the Strait of Hormuz and enriched uranium removal. Both remain hard red lines for Tehran, so the gap that blocked a signature all week is unchanged. This (Monday) morning, Trump struck a calmer tone on his social media platform Truth Social, telling critics to stand down while he negotiates.

Military action continued over the weekend. US forces struck strategic targets around Hormuz, including a telecommunications tower on Sirik Island and sites on Goruk and Qeshm. The strikes were framed by the US administration as self-defence, with the claim that the ceasefire was still in place. Iran's Islamic Revolutionary Guard Corps (IRGC) retaliated by firing ballistic missiles at a US airbase in Kuwait, claiming to have destroyed it. The ceasefire is now being sustained rhetorically while both sides trade direct blows, a fragile posture. This is not uncommon in war, however. As US Vice-President JD Vance says: "Ceasefires, they're not always perfect".

The Israel Defence Force (IDF) captured Beaufort Castle in southern Lebanon, the deepest ground incursion into Lebanese territory in over 26 years, a clear sign Israel is using the diplomatic vacuum to degrade Hezbollah while no deal constrains it. Reports say Iranian President Masoud Pezeshkian has submitted a resignation letter to the Supreme Leader, complaining that he and the civilian government have been sidelined and the IRGC now controls decision making.

Despite the ongoing closure of the Strait of Hormuz, the de-escalation rhetoric kept oil prices on a downward path with a 7.5% decline in brent to USD 92. Neither party is interested in a full-blown return to the war, but energy experts are still very worried about prices during the summer and autumn considering the reopening of the Strait is likely to take months and the full normalisation of the energy flows may not happen before 2027. This morning, Bloomberg reported Iran has allowed 15 ships to cross the Strait over the past 24 hours.

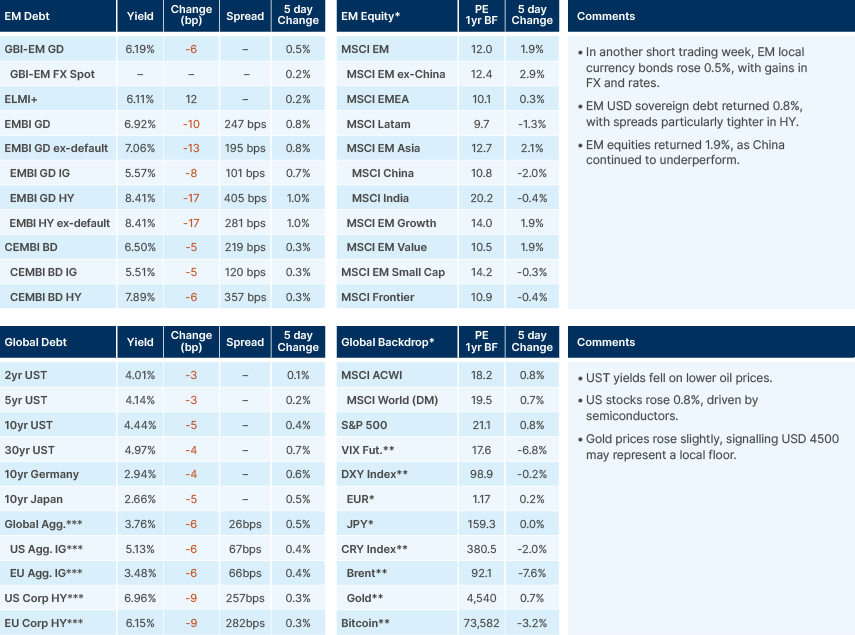

Despite geopolitical uncertainties, emerging market (EM) assets had solid returns in May, with the MSCI EM rising 9.7%, driven by South Korea and Taiwan. Latin America, China and India underperformed, declining 4.2%, 3.0%, and 0.6%, respectively. The EM lead over global equities widened as the MSCI World rose 5.6%, slightly ahead of the S&P 500, which was up 5.3%. The narrow market leadership driven by Artificial Intelligence (AI) and energy remains a feature of both developed markets (DM) and EM, with just 2% of all 1,224 stocks in the MSCI EM and 4% of the S&P 500 trading at all-time highs.

It was also a positive month for EM debt. Sovereign debt rose 1.0%, led by high yield (HY), which gained 1.6%. Local currency bonds rose 0.9%, with returns coming from carry and slightly tighter rates. Corporate debt rose 0.4%, with investment grade (IG) and HY delivering broadly similar returns of 0.3% and 0.5%, respectively. EM debt outperformed the Global Aggregate Index (0.3%) and US HY (0.5%).

Emerging Markets

Asia

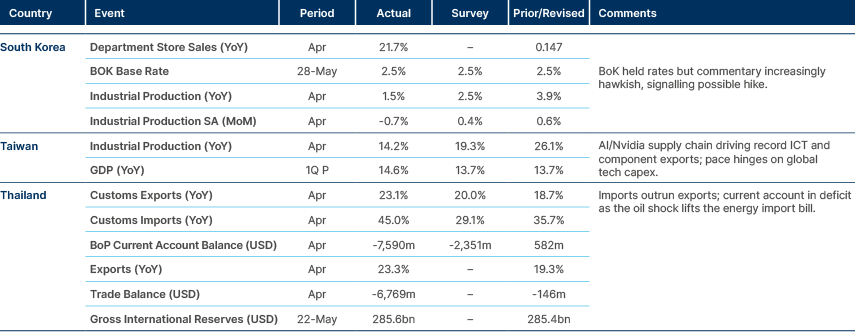

South Korea held rates, but central bank more hawkish.

South Korea: South Korea's record semiconductor export boom is increasingly a story of concentration rather than breadth. In the first quarter, Korea's five largest exporters, including Samsung Electronics and SK Hynix, accounted for USD 95.7bn, equivalent to 43.5% of total exports of USD 219.9bn and more than 80% of the entire increase in exports. The narrowness is just as stark in production, where manufacturing output rose 3% quarter-on-quarter but only 0.2% once chips are stripped out, with semiconductor output alone up 14.1%. Because chips generate just 2.1 jobs per KRW 1bn of output, around a third of the manufacturing average, the boom is doing little for employment and is widening wage gaps across the economy. Chief Presidential Secretary for Policy Kim Yong-beom cast the resulting mix of high interest rates, elevated inflation and a strong dollar as the cost of success of a transition to a higher-growth phase, projecting nominal growth close to 10% in 2026 on improving terms of trade from semiconductors and AI, and attributing Won weakness to foreign profit-taking after the rally in the Korea Composite Stock Price Index (KOSPI). The framing is politically convenient, but it captures a real tension between headline growth that is genuine in aggregate yet barely felt in the wider labour market.

Seoul is holding back strategic oil reserves it had previously pledged to release, delaying 22.46 million barrels originally due by 9 June. Officials now see no urgent need given improved supply, alternative sourcing and crude swap arrangements, and report that roughly 85% of pre-war crude volumes are secured through July. The more durable shift is in where that crude comes from, with non-Middle East suppliers now accounting for 51.5% of tentatively secured volumes for May to July, up sharply from 30.9% a year earlier, and the Americas alone rising to 35.6% from 23.1%. By treating International Energy Agency (IEA) coordinated reserves as a last resort rather than drawing them now, Korea is positioning for a possible tighter phase around August rather than reacting to present conditions.

Samsung Electronics defused near-term strike risk after its union ratified a wage agreement with 73.7% support on a 95.5% turnout. The endorsement was highly uneven, running at 80.6% within the semiconductor-heavy supra-enterprise union, but just 21.1% in the union representing finished-products staff, a split that mirrors a settlement skewed heavily toward chip employees. Memory staff could receive close to KRW 600m should operating profit reach KRW 300trn, against roughly KRW 6m in shares for finished-products workers. The deal buys labour peace in the division that matters most for output, but the disparity leaves a reservoir of discontent elsewhere in the group.

Latin America

Inflation trending higher in Brazil, activity still strong.

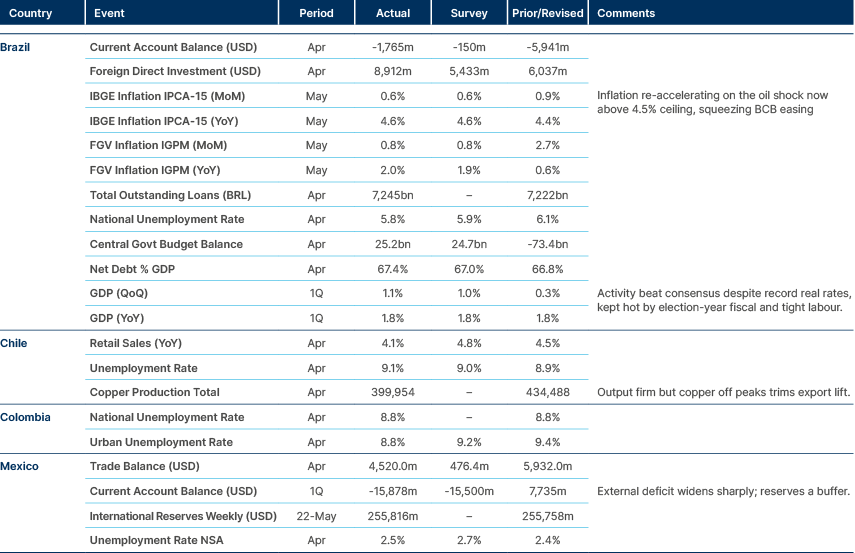

Argentina: Economy Minister Luis Caputo confirmed the government will deploy USD 1bn from its latest International Monetary Fund (IMF) disbursement to repurchase close to USD 1.9bn in non-marketable Treasury bonds held by the Central Bank of Argentina (BCRA). That lifts total repurchases in May to USD 22.3bn in nominal terms and trims the gross debt stock by around 3.3% of gross domestic product (GDP). For the BCRA, swapping illiquid non-marketable paper for cash strengthens gross reserves and liquidity, plausibly in preparation for an upcoming Bopreal payment of about USD 1bn. The operation is as much about improving the quality and tradability of the BCRA balance sheet as about the headline debt reduction.

Caputo also predicted that President Javier Milei will win re-election comfortably in 2027, describing it as an atypical contest in which accelerating growth drives sentiment. He also claimed this year will deliver the strongest expansion of Milei's term after 4.4% growth in 2025. He expects inflation to end 2026 near 20% and pointed to a fall in poverty of some 25pp. EmergingMarketWatch (EMW) assesses that the recovery remains export-led and has yet to translate into employment or purchasing power, which explains why approval has stayed negative despite macro stabilisation, while still regarding Milei as the clear favourite. The gap between strong aggregate data and weak household sentiment is the central political risk to watch.

Brazil: Central Bank of Brazil (BCB) Governor Gabriel Galipolo signalled that the country's positive output gap is narrowing back toward potential under the weight of restrictive policy, while cautioning on the inflation risks from the Middle East energy shock and distinguishing direct fuel effects from more persistent second-round effects. He also flagged food-price risk from El Nino. The Monetary Policy Committee (Copom) has now cut the benchmark Selic rate by a cumulative 50 basis points over two meetings to 14.50.

Presidential candidate Flavio Bolsonaro met with US President Trump in Washington in an effort to bolster his candidacy, and asked for Brazilian criminal gangs to be designated as terrorist organisations, a step President Lula opposes. Bolsonaro rejected suggestions the trip was intended to deflect attention from the Banco Master scandal. EMW speculated the visit may firm up Bolsonaro's core support of roughly 20 to 25%, but is unlikely to win over independents or materially alter the shape of the race, which remains broadly unchanged.

Colombia: Colombia's first-round vote on 31 May upended the polls. The right-wing Abelardo de la Espriella came first with 43.7%, ahead of the leftist Ivan Cepeda on 41%. With neither clearing the winning threshold, the two advance to a runoff. Centre-right candidate Paloma Valencia's vote collapsed to just 6.9%, and both she and former president Alvaro Uribe immediately endorsed de la Espriella, so a high share of her vote should flow his way. That leaves Sergio Fajardo's still uncommitted centrist bloc as the more important prize, though lingering centrist disaffection with the Petro administration makes a clean return of those votes to the left far from certain.

For markets, the notable shift is that the contest now sits on unusually orthodox ground. De la Espriella's programme closely resembles Valencia's: fiscal consolidation of around 3% of GDP over four years, weighted to spending cuts, liberalisation of oil and gas and construction, repeal of the decree forcing pension funds to repatriate foreign assets, and openness to the IMF, all against an inherited central government deficit near 7.8% of GDP. More surprising is the Cepeda camp, which is weighing a roughly 2% of GDP adjustment and floating market-acceptable finance ministers in Clara Lopez, Jose Roberto Acosta and German Umana, any of whom we would see as a marked improvement on the heterodox, market-hostile German Avila. Both run-off candidates now offer a more orthodox prospectus than the campaign's polarised tone suggests.

Mexico: The Bank of Mexico (Banxico) Governor Victoria Rodriguez indicated that the policy rate now sits firmly in neutral territory, citing an ex-ante real rate of 2.8% within an estimated neutral band of 1.8% to 3.6%, and signalled a hold from here without committing to a horizon. That stance is more hawkish than Deputy Governor Analilia Mejia, who continues to view policy as restrictive, pointing to a board that is no longer uniformly dovish. Rodriguez characterised the increase in the Special Tax on Production and Services (IEPS) as an orderly first quarter shock that produced no second-round effects. Banxico nonetheless cut its 2026 growth forecast by 0.5pp to 1.1% on weak investment and consumption, and dovish members still hint at further easing, leaving the near-term path finely balanced.

Peru: With the election runoff over the next weekend, the latest polls show Keiko Fujimori ahead of Roberto Sanchez by roughly 3%, narrower than before. Fujimori leads in Lima and among higher-income voters, while Sanchez is ahead in rural areas and the south. The bloc of voters without an obvious allegiance to either candidate is large. Beyond the campaign, the government approved a diesel subsidy worth about USD 1.4bn, easing the energy shock for consumers but adding to a stretched fiscal position, while the Producer Price Index (PPI) rose 2.5% month-on-month. There was no monetary policy decision in May.

Central and Eastern Europe

No rate cut yet in Hungary, disinflation halted in Poland.

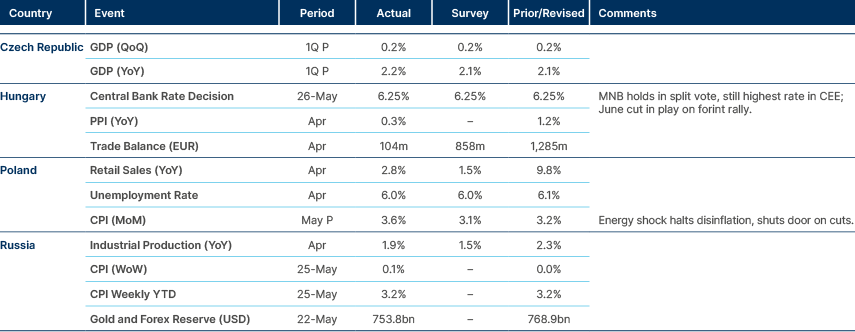

Czech Republic: The Czech National Bank (CNB) attributed weaker than projected first quarter growth of 2.2% year-on-year, below its own 2.5% forecast, to higher energy prices. The shortfall was transmitted largely through imports, as oil and gas costs rose on the back of the US/Iran war. Domestic demand held up well, with investment broad-based across machinery, buildings and vehicle-fleet renewal, and only modestly softer household consumption.

Prime Minister Andrej Babis again pressed the CNB to cut its policy rate, arguing that Czech firms face worse financing terms than their euro-area peers and pointing to rising mortgage costs. The CNB responded that it does not comment on political statements and that its independence is guaranteed in law.

Hungary: Ratings agency S&P affirmed the 'BBB-' sovereign rating, but maintained a negative outlook. This outlook "reflects risks to fiscal and economic stability over the next two years. Large budgetary deficits, high debt, and elevated interest expense continue to limit Hungarian authorities' policy flexibility to manage endogenous and exogenous pressures". The negative outlook seems conservative, and its likely to be removed as the new Tisza Party government progresses on reforms.

Kazakhstan: Opening a Eurasian Economic Union (EAEU) forum in Astana, President Kassym-Jomart Tokayev urged the bloc to deepen ties with Southeast Asia, Africa, Latin America and the Middle East. Tokayev also praised the progress of Free Trade Agreement (FTA) talks with India, and said future negotiations should proceed only with partners offering tangible benefits. He also called for the digitisation of transport corridors to lift transit volumes. The tone was consistent with Kazakhstan's established line of pragmatic, interest-driven integration rather than political alignment.

Poland: Prime Minister Donald Tusk said the first 40 contracts under the EU's Security Action for Europe (SAFE) defence lending programme, worth roughly PLN 100bn, would be signed by 30 May. This is the deadline for single country defence projects, after which new projects must involve other member states. Poland's allocation under the facility is EUR 44bn (PLN 186bn), out of a total EUR 150bn, and the agreement signed with the European Commission on 8 May unlocked an advance of around EUR 6.5bn, benefiting more than 10,000 Polish firms. The structure lets Poland increase defence spending without issuing its own bonds. However, because Value Added Tax (VAT) is not levied on these purchases, the budget will forgo revenue worth about 0.14% of GDP in 2026.

Central Asia, Middle East, and Africa

Rate hike in South Africa on surging PPI.

South Africa: S&P affirmed the country's 'BB' rating and maintained the positive outlook. A key factor for a one or two notch upgrade would be the continued delivery of reforms and fiscal discipline, allowing for higher GDP growth path than in previous decades.

Developed Markets

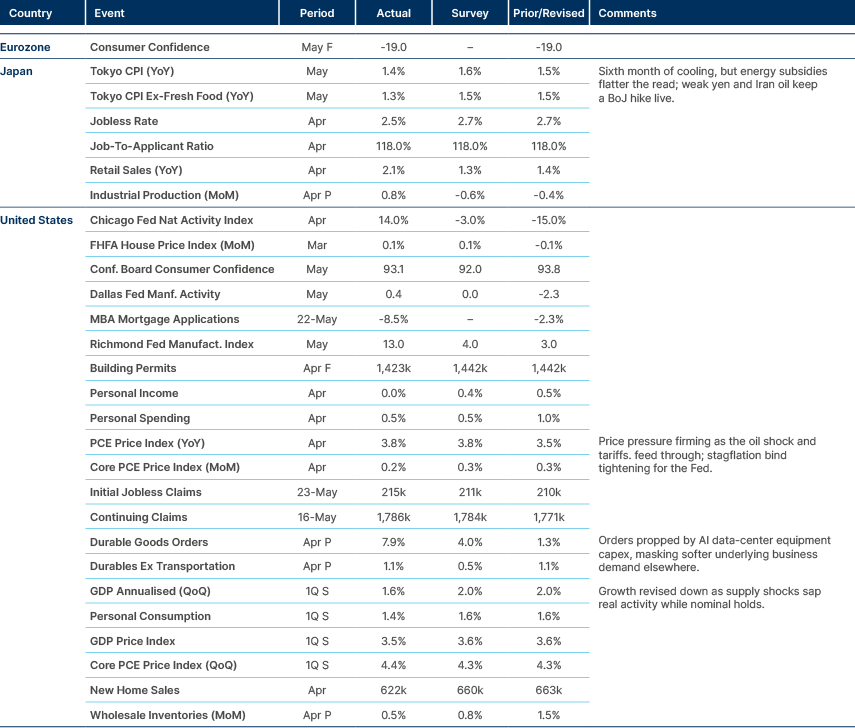

US industrial activity picking up alongside inflation.

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.