- Stalemate in Hormuz after the US slammed Iran’s counterproposal.

- Q1 2026 earnings season reflects the AI-driven profits boom.

- Bank Indonesia announced a multi-pronged stabilisation package.

- Indian PM Modi called for nationwide austerity to preserve FX reserves.

- JPMorgan raised its Kospi bull case target to 10,000.

- Fitch upgraded Argentina from ‘CCC+’ to ‘B-‘ with a stable outlook

- World Bank approved USD 1bn of financing for Egypt under GROWTH II.

- S&P affirmed Qatar’s ‘AA/A-1+’ rating with a stable outlook.

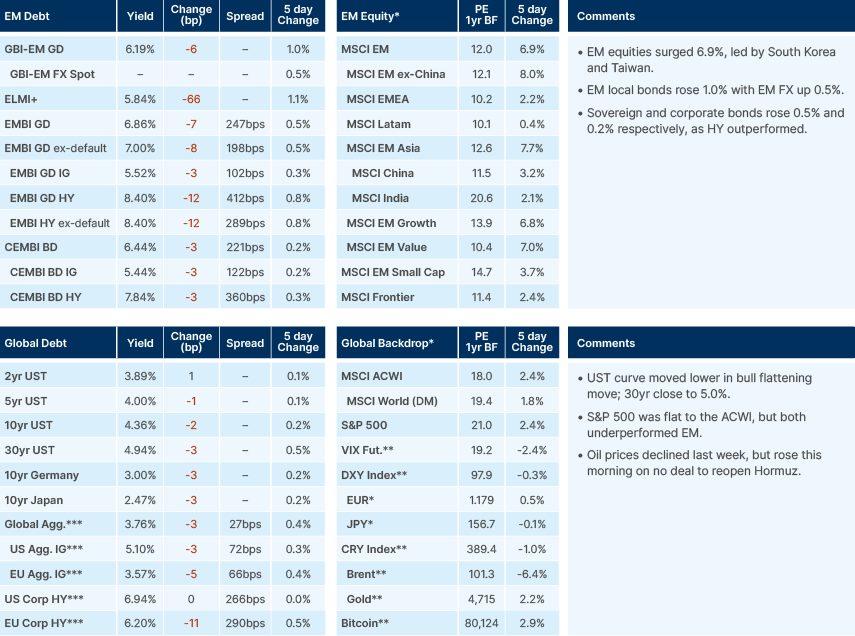

Last week performance and comments

Global Macro

The Strait of Hormuz (SoH) is back at stalemate mode after US President Donald Trump rejected Iran’s proposal for reopening the SoH and control over its uranium stockpile.1 Iran will be the key topic of discussion on the summit between presidents Trump and China’s Xi Jinping in Beijing this week (13 to 15 May). Other topics to monitor are trade and investments (potential of China investing in US manufacturing). The Iranian Foreign Minister Abbas Araghchi was in China on 6 May as China remains one of Iran’s key allies.

Against this backdrop, the UK and France will host more than 40 defence ministers on plans to restore SoH trade flows. The mission is described as “defensive and independent” to safeguard vessels transiting the strait. Last week, transiting vessels were challenged and a few naval skirmishes between the US and Iran were reported. Iran resumed attacks over the weekend on Qatar, Kuwait, and the UAE.

In Russia, President Vladimir Putin praised troops fighting in Ukraine for a "just cause" against "an aggressive force armed and supported by the entire NATO bloc". Putin also said he'd be willing to meet Ukraine President Volodymyr Zelenskyy in a third country, but only after a peace treaty aimed at a long-term historic perspective is finalised, "this should be a final deal, not the negotiations". Whilst Putin has made similar statements before, this took place during Russia’s Victory Day Parade without any hardware displays due to fears of Ukrainian attacks. Russia also agreed on a three-day ceasefire (until today) mediated by the US when an exchange of 1,000 prisoners from each side was agreed.

The situation across these two geopolitical theatres highlights investors’ challenge of weighing between war and peace prospects that change tweet-by-tweet.

In the meantime, the Q1 2026 earnings season is showing the AI revolution is driving a rare boom in profits. The consensus forecast for one-year forward earnings growth is 25.6% higher than in December 2025 for the S&P500 and 50.8% higher over the same period for the MSCI EM. This growth, both in the US and emerging markets (EM), has been highly concentrated in semiconductor, technology, and energy stocks. Nevertheless, all sectors have delivered earnings growth in Q1 2026, a rare stat.

The largest ten companies in the S&P now represent 40% of the index, a level of concentration similar to the peak of the dot.com bubble (41%) in the early 2000s, Japan’s share of MSCI ACWI (44%) in the late 1980s, and the same as the ‘Nifty Fifty’ as percentage of S&P in the late 1960s. Nevertheless, it remains below the peak of concentration in railways in the late 19th century, when the sector came to represent 63% of US stock market. Debating the sustainability of earnings seems futile now as AI is already carving itself as one of the major secular themes in the history books. The main risks for investors today are the unwind of semiconductors positions, Chinese and/or Indian stocks rallying, and Brazil underperforming on negative election surprises.

The impact of AI on the macro picture has been ambiguous, so far. The surge in semiconductor prices is very visible in producer price indices, as electronic components and accessories rose 20% last year. However, its pass-through to consumers has been more complex to infer. Goldman Sachs said software and accessories are 30x larger in the US personal consumption expenditures (PCE) index than consumer price index (CPI) inflation. Furthermore, the software deflator for capex (which does not include computer accessories and is quality-adjusted), has declined almost 4% over the last year.

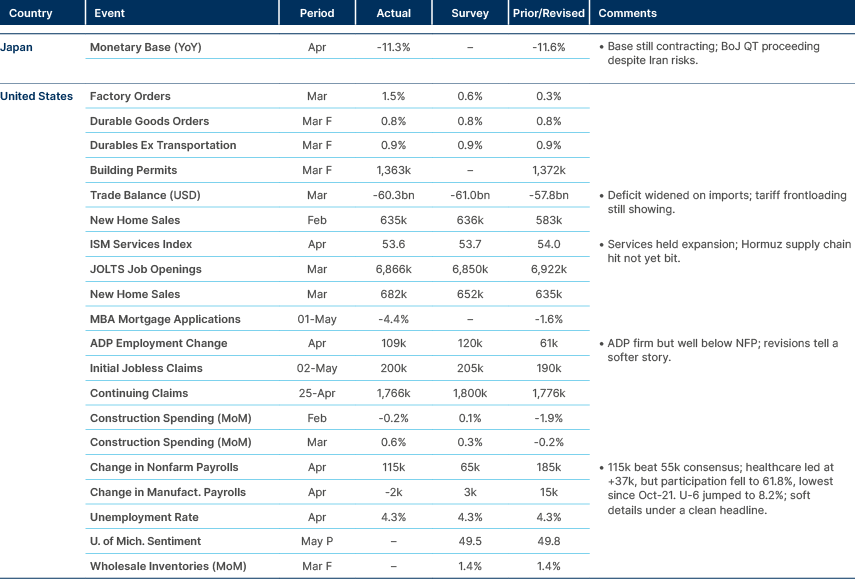

Last week, the non-farm payrolls showed a solid increase of 115k, above consensus of 65k, but both the three and six-month moving averages are stabilising at around 50k. Most economists believe that the break-even to keep unemployment unchanged declined to 0-100k given the clampdown on US immigration.

A key development to highlight in the currency space has been the surge in FX interventions. Last week, Bloomberg reported that Japan’s Ministry of Finance spent JPY 4.68trn (USD 30bn) in the first week of May to support its currency, the same intervention as the prior week. In EM India, Indonesia, South Korea, and Taiwan have all been intervening to keep its currencies from weakening excessively:

- Bank Indonesia announced a multi-pronged stabilisation package on 5 May after the Rupiah hit a record low of IDR 17,425, including “around the clock" intervention on spot, non-deliverable forwards (NDFs), and offshore NDFs. The country’s FX reserves stood at USD 148.2bn at March-end.

- In Korea, the KRW touched 1,520 in early April, the weakest since March 2009, prompting Ministry of Economy and Finance (MOF)/Bank of Korea (BOK) verbal intervention, National Pension Service (NPS)-led dollar-hedging flows, and a four-way consultative framework (MOF, BOK, NPS, Welfare ministry) to align pension outflows with FX stability.

- And in Taiwan, the central bank (CBC) saw the steepest monthly drop in FX reserves in nearly 15 years in March (down USD 8.6bn to USD 596.9bn), explicitly attributed to stabilise the TWD against Iran-war-driven outflows. Intervention reportedly continued at a similar pace through April.

US Treasury Secretary Scott Bessent is in Japan and South Korea this week, ahead of Trump’s meetings in China on later this week. A key topic of conversation is likely to be trade surpluses with the US. The market will therefore focus on any indications of interventions on the FX front.

Emerging Markets

Asia

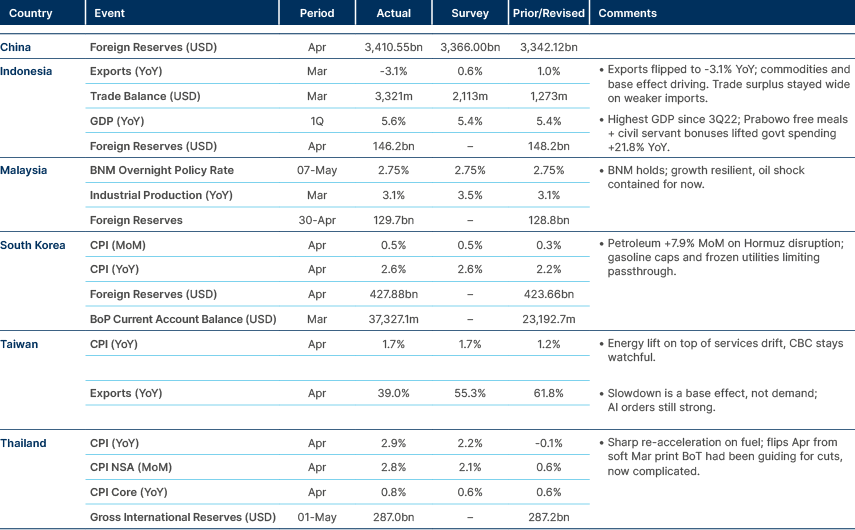

Indonesia GDP growth highest since 2022.

China: April exports surprised sharply to the upside, rising 14.1% yoy versus consensus of 8.4% and March's 2.1%, while import growth moderated to 25.3% from 27.8%. The export beat is concentrated in AI-linked categories where prices have risen sharply, but the gain accrues to a narrow set of industries. The import side reflects soaring energy prices, the cost of which is borne across the entire economy. The composition matters more than the headline. A small group of high-end exporters is capturing the AI capex cycle, but the energy bill is a broad-based tax on activity, which leaves the net macro impulse less constructive than the trade balance alone would suggest.

India: Following the ruling BJP's strong showing in state elections, Prime Minister Narendra Modi called for nationwide austerity to preserve FX reserves. Measures advocated include working from home where possible, judicious fuel use, postponement of non-urgent foreign travel, and a one-year moratorium on gold purchases. The framing is unusual for an Indian PM in the wake of a political win, and points to genuine official concern about the external account in the current oil price environment. Gold imports in particular have been a recurring pressure point on the current account and the Rupee. Whether the rhetoric translates into binding policy or remains exhortation will be the next watch item.

Indonesia: Bank Indonesia halved the monthly FX purchase limit to USD 50k per person from USD 100k, requiring documentation above the cap, and Governor Perry Warjiyo signalled a further reduction to USD 25k is in preparation. The move is an attempt to defend the Rupiah through capital flow controls rather than rate hikes, preserving rate-cutting optionality for the domestic cycle. Quantitative tools of this kind tend to be partially effective at best, and BI may ultimately still be forced into a 25 basis point (bps) policy rate hike if pressure on the currency persists. The sequencing tells you the central bank's preference ranking: growth support first, FX defence via administrative measures second, rate hikes as the last resort.

South Korea: JPMorgan raised its Kospi bull-case target to 10,000 and base case to 9,000 on the strength of the chip cycle. The upgrade is consistent with first-quarter trade data which show Korea overtook Japan to become the world's fifth-largest exporter, with quarterly exports at a record USD 219.9bn, around USD 30bn ahead of Japan. Export growth ran at 31.3% yoy, the fastest among the top seven exporting nations. Beyond semiconductors, K-consumer goods (cosmetics, agri-marine, household goods) are emerging as a second growth leg, with the trade ministry expanding its strategic items list from 15 to 20. Early SoH disruption is showing through in autos and battery materials, which warrants monitoring.

A new BOK study estimates the equity wealth effect in Korea at around 1.3%, materially below the 3–4% range typical in the US and Europe. The structural reason is that equity gains tend to be channelled into housing rather than consumption, particularly for non-homeowners (around 70% of the gain flows to property). However, recent AI-driven price moves have broadened equity ownership to younger and lower-income investors, which mechanically raises both the upside wealth effect and the downside risk in a correction. The composition shift is the key insight: the same wealth effect coefficient applied to a different ownership distribution produces a different macro response.

The government extended its ban on petroleum hoarding through July to enforce the price ceiling, with stronger administrative fines and informant rewards being introduced. Officials estimate the price cap shaved 0.6 percentage points from March CPI inflation and 1.2 points from April; without it, headline inflation would have printed at roughly 2.8% and 3.8%, respectively. The mechanism is effectively a stealth subsidy with the fiscal cost obscured rather than absent. The longer the cap holds, the larger the eventual pass-through when it is lifted.

Thailand: Gross international reserves rose USD 6.5bn mom to USD 286.9bn at end-April, reversing a USD 13.4bn March drop and up 11.7% year-on-year. FX reserves rose 2.8% mom to USD 245.2bn, while gold holdings fell 1.1% to USD 34.9bn. The Baht firmed to 32.495 from 32.585 over April and was trading at 32.225 at the time of release. The reserve rebuild reverses March's drawdown and is consistent with a less defensive FX posture, though the absolute level had already been comfortable. The gold reduction is small, but worth noting against the broader EM trend of central bank gold accumulation.

Latin America

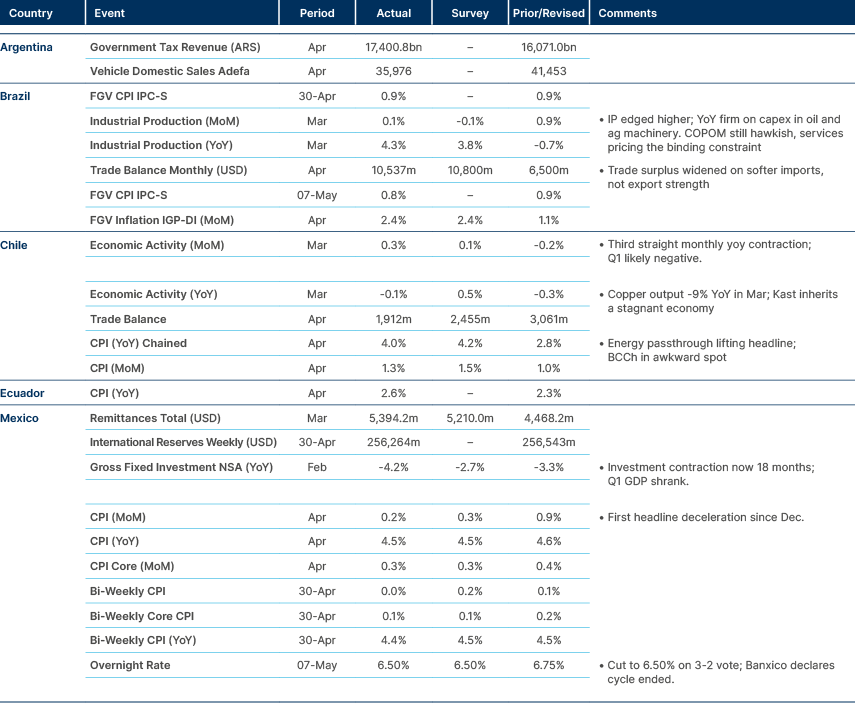

Chile’s weak copper output driving soft economic activity.

Argentina: Fitch upgraded Argentina’s credit rating on May 5th from ‘CCC+’ to ‘B-‘ with a stable outlook. This is Argentina’s first upgrade in eight years and reflects, according to the agency, structural improvements in fiscal and external metrics. Specifically, Fitch referred to progress on economic reforms, stronger management of FX reserves and growing confidence that the country will meet its debt obligations. Moodys and S&P are yet to revise their rating for Argentina. Milei announced preparations for a "Super RIGI", an upgraded version of the existing large-investment incentive regime targeting industries that do not yet exist in Argentina. Detail is thin, but Deregulation Minister Federico Sturzenegger's recent comments on a special regime for fully AI-run companies point to AI infrastructure as the likely focus. The framing fits Milei's broader pattern of using fiscal carve-outs to attract specific high-value sectors rather than pursuing broad-based reform. Execution risk is high and the policy detail will determine whether this is a credible investment vehicle or political signalling.

Colombia: AtlasIntel's latest poll keeps Iván Cepeda leading the first round at 37.4%, but shows him losing every runoff scenario tested. Cepeda loses to centrist Sergio Fajardo 37.9% to 39.8%, to Abelardo de la Espriella 42.0% to 47.8%, and to Paloma Valencia 40.6% to 49.1%. This breaks from Invamer, which still has Cepeda winning the runoff. The polling environment itself is degrading: Law 2494 of 2025 has pushed GAD3 out of pre-election publication, and AtlasIntel faces a CNE inquiry. The decisive variable for the second round is whether de la Espriella and Valencia (jointly near 50% in the first round) consolidate behind a single centre-right candidate, with no public sign of an alliance yet. For markets, the AtlasIntel scenarios are constructive relative to the Gustavo Petro continuity case, but the divergence across pollsters and the regulatory pressure on independent firms argues for caution.

Peru: López Aliaga led a rally outside the National Jury of Elections (JNE) rejecting the 12 April election results and demanding an internationally supervised audit, but turnout came in below 3,000, signalling limited street-level mobilisation behind the challenge. Aliaga currently trails Roberto Sánchez (Together for Peru, positioned as Castillo's political heir) by more than 20,000 votes, leaving him outside a runoff against Keiko Fujimori on current trends. The JNE expects to certify results by mid-May. A Sánchez-Fujimori runoff would be a polarised contest that markets will read as binary on policy continuity.

Central and Eastern Europe

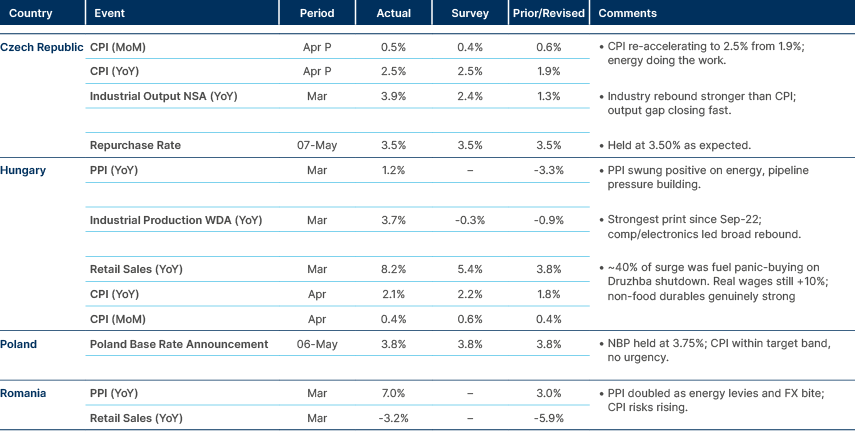

CPI inflation accelerating due to energy costs.

Hungary: Deputy Governor Zoltán Kurali signalled that the Forint's roughly 8% YTD appreciation against the EUR has opened policy room, with a June rate cut possible after the updated Inflation Report. He came across as notably more dovish than Governor Mihály Varga who, after the April Monetary Policy Committee meeting, flagged that inflation could approach 5% in the autumn and that developed market rate paths were a central bank (NBH) constraint. Kurali also confirmed NBH support for the new government's eurozone accession objective. The internal MPC divergence is the more important signal than the specific dovish call: it suggests the next move is more contested than the headline rhetoric would imply.

Péter Magyar was officially sworn-in as Hungary's new Prime Minister on Saturday. He gave President Tamás Sulyok until 31 May to resign, arguing he was not fit for office for allowing the country to slip into autocracy under predecessor Viktor Orbán. The aggressive opening posture against the presidency signals Magyar intends to drive institutional reform quickly, with implications for the central bank, judiciary and media regulator. For markets, the policy mix matters more than the political theatre: the eurozone accession ambition is constructive, but the speed and breadth of institutional confrontation will determine whether Hungary stabilises or enters a new period of governance volatility.

Poland: Finance Minister Andrzej Domański said the Iran war's economic impact has been limited so far beyond fuel prices and tax cuts, but flagged that defence spending remains the priority and that there is no room for new social programmes. He backed EU joint borrowing for defence while acknowledging political resistance. The deficit plan is a gradual reduction to 6.8% of GDP in 2026 from 7.3% in 2025, with no major fiscal action expected before the autumn 2027 election. Government GDP forecasts have been trimmed to 3.6% from pre-war hopes of above 4%. The fiscal trajectory is high relative to peers but the government has chosen to defer adjustment rather than risk political backlash ahead of the election.

The European Commission approved Poland's SAFE loan agreement, making Poland the first EU member to clear the programme. Poland is set to receive nearly EUR 43.7bn of the EUR 150bn envelope, with a 15% advance (over EUR 6.5bn) due on signing. The Law and Justice Party (PiS) has politicised the programme via National Bank of Poland (NBP) President Adam Glapiński's "Polish SAFE 0%" counter-proposal, but the NBP is unlikely to fund it via gold sales before the 2027 election. The actual EU disbursement is the more relevant variable for the fiscal arithmetic, and the early approval suggests Poland will be a major beneficiary of the EU's coordinated defence financing push.

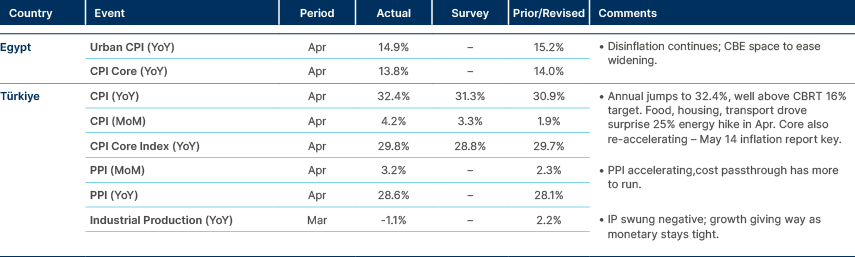

Türkiye: Finance Minister Mehmet Şimşek warned that the SoH blockage represents the most severe supply shock since the 1970s and acknowledged Türkiye is not immune. Inflation expectations have shifted from a year-end target near 20% to roughly 27%, and the budget deficit could edge toward 4% of GDP from a previously projected 3-3.5%. A formal reassessment is planned over the summer, with revised 2026 numbers and an updated medium-term framework to follow. The candour from Şimşek is constructive in itself, but the magnitude of the upward revision to the inflation path materially complicates the central bank’s policy trajectory.

The sliding-scale fuel mechanism has absorbed most of the price shock, with diesel held at TRY 72.7 versus an unsubsidised TRY 89.4 and petrol at TRY 64.6 versus TRY 79. The fiscal cost was around TRY 90bn (USD 2bn) over two months, with full-year revenue foregone potentially reaching TRY 600bn (USD 13-14bn). Each USD 10 rise in the oil price adds USD 3-4bn directly to the import bill, and USD 5bn including indirect effects; a USD 95 oil average versus the budgeted USD 65 implies roughly USD 15bn of additional current account pressure. The mechanism is buying domestic political space at the cost of fiscal and external balance deterioration, and the position is not sustainable through year-end at current oil levels.

Ukraine: A US brokered three-day ceasefire with Russia (9–11 May) is collapsing on its final day. Both sides accuse each other of violations. Zelenskyy says Russia is "not even particularly trying" to observe it; Moscow's defence ministry insists it has "strictly observed" the truce. NASA satellite data analysed by ISW shows military activity decreased but did not stop. The 1,000-prisoner swap and a brief pause on large-scale strikes are the only concrete results. US envoys Witkoff and Kushner are expected in Moscow soon for further negotiations around a more permanent ceasefire.

Central Asia, Middle East, and Africa

Turkey CPI jumps, core still stable.

Egypt: The World Bank approved USD 1bn of financing under GROWTH II to support private-sector job creation, fiscal resilience and the green transition, including a USD 200mn UK credit guarantee. The package backs state owned enterprise (SEO) governance reform, fair-competition enforcement, domestic revenue mobilisation, deeper local debt markets and lower government funding costs. The composition of the package reflects the World Bank's standard structural agenda for Egypt: the disbursement matters fiscally but the conditionality is where the medium-term improvement (or disappointment) will be determined.

CPI inflation rose 14.9% yoy in April, down from 15.2% yoy in March and below the 15.9% yoy consensus. The deceleration extends the disinflation trajectory and supports the case for further easing by the central bank (CBE), though the path is contingent on FX stability and the energy import bill in the current oil environment.

Nigeria: Aliko Dangote announced plans for a 20,000 MW power project, raised in talks with the International Finance Corporation (IFC), expanding the group beyond refining, cement and fertiliser. Cash flow from existing investments is described as sufficient to fund the build. Actual Nigerian grid supply has averaged near 3,331 MW versus a 6,000 MW stabilisation target, with the World Bank putting the cost of unreliable power at around USD 29bn annually, or 10% of GDP. New Minister of Power Joseph Tegbe replaces Adebayo Adelabu, who resigned last month. A successful Dangote build-out would be transformational for Nigerian industrial productivity, but the track record on Nigerian power projects argues for scepticism on timeline and capacity.

Qatar: S&P affirmed Qatar at ‘AA/A-1+’ with a stable outlook but forecast a 5.1% GDP contraction in 2026 driven by the LNG shutdown and SoH closure. The base case assumes the strait reopens by end-May with gradual normalisation through H2, and a full LNG restart taking up to a month once decided (12 of 14 trains). Full-year LNG output is seen 40% below pre-war levels. The contraction headline is severe but the stable outlook reflects Qatar's fortress balance sheet and the temporary nature of the supply disruption rather than structural deterioration.

Net government assets remain at around 135% of GDP (USD 300bn), but the current account is forecast to swing to -0.7% from a 15% surplus in 2025, and the fiscal deficit to widen to about 1.9% from 1.2%. LNG expansion plans (126 metric tonnes per annum (mtpa) by 2027, 142 mtpa by 2030) remain intact but delayed. Bank external debt of USD 119bn (33% of domestic lending), of which 52% is non-resident deposits and interbank, is the key watch item if the conflict escalates. The sovereign can absorb the shock indefinitely; the banking system's external funding profile is the more fragile pressure point.

Saudi Arabia: The capital market regulator expects more than USD 10bn of inflows from Saudi sovereign sukuk inclusion in JP Morgan and Bloomberg EM bond indices in 2027, against a local debt market of around SAR 1.04tn (USD 278bn) and just over USD 3bn of over the counter (OTC) bond turnover in Q1. Inclusion follows reforms including the Primary Dealers Program expansion to international banks, an OTC settlement framework launched in mid-2025, and Euroclear connectivity. The inflow estimate is plausible given the structural underweighting of Saudi paper in benchmark portfolios, and the local market infrastructure improvements are necessary preconditions for absorbing that flow without disorderly price action.

Saudi Arabia and Kuwait have lifted restrictions on US use of bases and airspace, clearing the way for a restart of Project Freedom to escort commercial ships through SoH. The reversal followed a phone call between Trump and Crown Prince Mohammed bin Salman, after Riyadh had blocked access in response to US officials downplaying Iranian strikes on the UAE. Pentagon officials cited a possible restart as early as this week. The reopening of Gulf Cooperation Council support for US naval operations in the Gulf is the most material shift in the regional security architecture since the war began, and is incrementally constructive for shipping insurance, oil flows and EM credit spreads more broadly.

South Africa: The Director General of the Department of International Relations and Cooperation (DIRCO) flagged plans to scale up crude imports from Angola and Nigeria to reduce exposure to SoH and conflict-prone supply, alongside a debate on accelerating domestic exploration. Nigeria already supplies 48% of South African crude (4.5bn litres in 2024) and Angola 15% (1.5bn litres), but both are expanding their own refining capacity and may prioritise domestic use. The diversification rationale is sound, but the supply availability is not guaranteed.

The bigger constraint is domestic. South Africa has lost roughly half its refining capacity since 2020 (Sapref and Engen shut), leaving Astron at around 100,000 barrels per day (bpd) and Natref at around 107,000 bpd. Around 75% of refined fuel needs are now imported, which means additional crude purchases do not solve energy security without rebuilding refining capacity. The structural energy security problem cannot be addressed at the crude level alone; the policy gap is in downstream investment, which has been deferred for over a decade.

Angola: The Lobito Corridor Master Plan has identified around 100 investment projects along the 1,300km route, with a total portfolio that could reach USD 6bn and agriculture as the largest single cluster. Around 30% of market potential is tied to Katanga in the DRC, anchoring the corridor's role in cobalt and copper exports. The 30-year concession is run by a Mota-Engil/Trafigura/Venturis consortium, with the first cargo shipment completed in July 2025. The corridor is strategically important as a Western-aligned alternative to Chinese-controlled DRC export routes, which is why the project has attracted disproportionate political attention from Washington and Brussels.

Funding is slipping. The Africa Finance Corporation is now lining up USD 3–5bn from at least ten lenders, with fundraising expected to start in Q3 2026 and close in late 2027, versus an original timeline that had the money in place this year. Construction completion has slipped to 2030, two years late. The slippage is consistent with the standard pattern for large African infrastructure projects but reduces the near-term economic upside for Angola and the strategic value to Western backers in the current geopolitical window.

Developed Markets

US nonfarm payrolls held up.

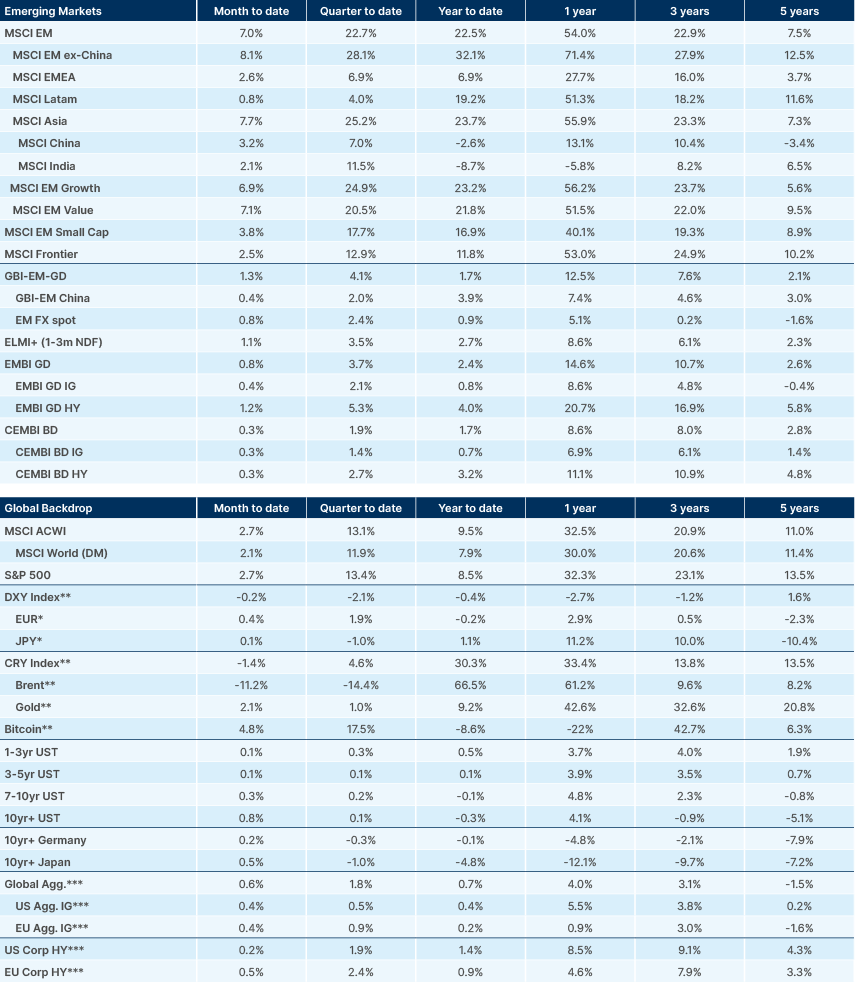

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. https://www.axios.com/2026/05/10/trump-iran-war-us-peace-plan-tehran-response-inappropriate