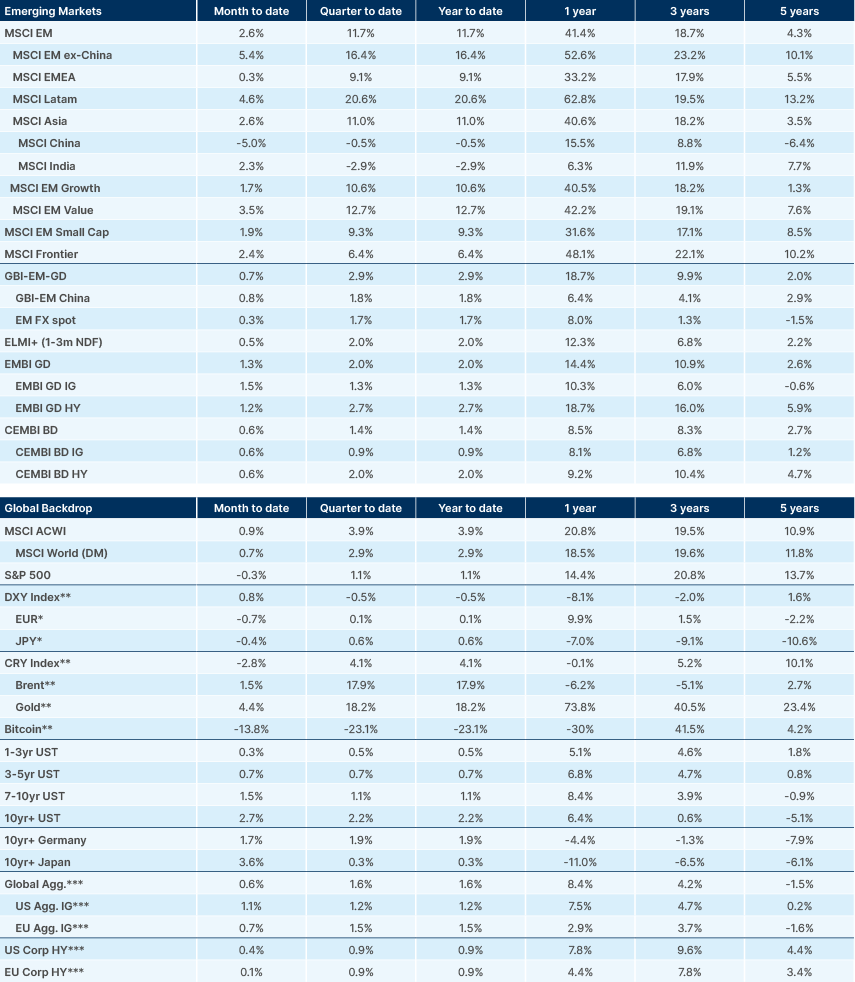

- Flows into EM assets continue to accelerate.

- Korean tech exports surge, highlighting rosy outlook for tech hardware exporters.

- US Supreme Court ruled IEEPA tariffs invalid, reopening ‘Pandora’s box’ of tariff noise.

- FOMC meeting minutes were cautious, with core PCE still elevated.

- US amasses a record number of troops in the Middle East as pressure on Iran mounts.

- Mexican security forces kill leader of the Jalisco New Generation Cartel.

- Peru named another new interim president.

- China to grant zero tariff access to 53 African countries from 1 May.

- IMF urges South Africa to reach a 3% primary surplus to ensure long-term debt stability.

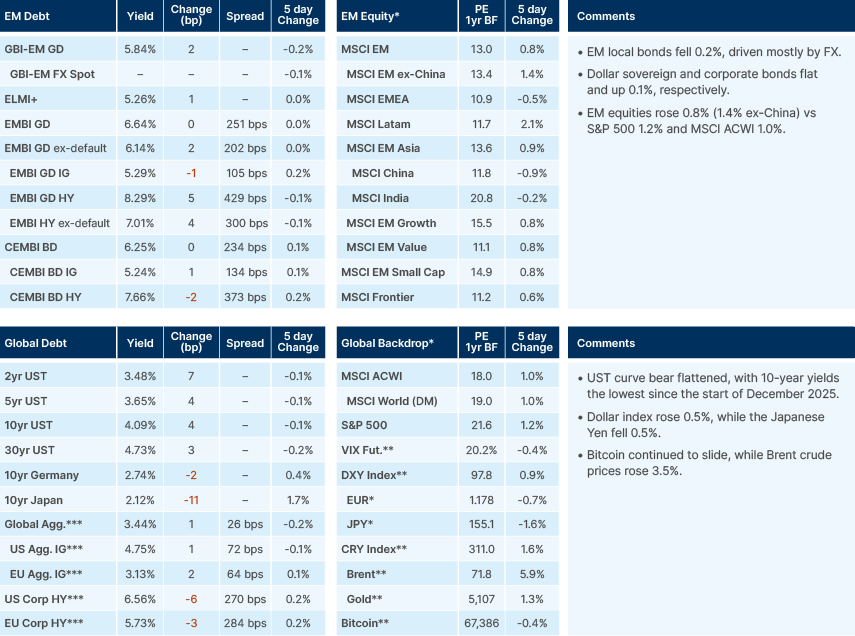

Last week performance and comments

Global Macro

Flows to emerging market (EM) funds continue to surge this year. Data from Bank of America Merrill Lynch shows an EM ex-China equity inflow of USD 71bn year-to-date (YTD), which is higher than flows to US, Europe and Japan funds combined. Flows to EM bond funds are also accelerating with net inflows of USD 3.5bn in the past two weeks. Historically, after periods of outflows from EM, such as the last two years, rotation back into the asset class has lasted for multiple years and coincided with long periods of EM equity outperformance. We will delve into the EM flow picture more deeply in this month’s Emerging View, to be published at the end of the week. EM stocks flows have been supported by better earnings momentum across the board, but with a big highlight to South Korea.

Korea’s February 20-day exports rose 23.5% yoy, following 33.8% in January, despite two fewer working days due to the Lunar New Year. On a per-day basis, growth accelerated sharply to 47.3% yoy from 14.8%, with average daily shipments edging up to USD 3.35bn from USD 2.5bn in January. Semiconductors remained the key driver, surging 179.1% yoy (from 70.2%). Exports to China, Vietnam and Japan rose 55.9%, 40.2% and 33.7%, respectively, while shipments to the US and EU increased 45.4% and 32.8%. The data reinforces the strength of the AI-led semiconductor cycle. Performance has been positive across many EM markets so far this year, but Korea and Taiwan becoming such clear beneficiaries of the AI infrastructure build out (US hyperscaler capex = Korea/Taiwan profit) has helped extend EM equity outperformance extend YTD, with Korea up 43% and Taiwan up 18%. Nvidia’s earnings report on Wednesday will likely determine the trajectory of the next leg of the AI trade, but barring a macro shock, the outlook continues to look rosy for semiconductor manufacturers.

The US Supreme Court ruled tariffs under the International Emergency Economic Powers Act (IEEPA) illegal, in a 9-3 vote. In recent months, IEEPA tariffs had been contributing 45% of total tariff revenue and have raised c. USD 120bn so far. In response, US President Donald Trump announced a 15% global tariff under Section 122. This keeps the weighted average US tariff at 11.1%, down from 13% before the Supreme Court decisions, according to data from UBS Global Research. The new 15% unilateral levy is only valid for 150 days, after which Congress will vote on whether to extend it. If they vote not to, the administration could largely put the tariffs back in place with some patchwork of Section 301 and 232 tariffs, focusing just on their largest trading partners.

In our view, the changes in the US tariff mechanism are unlikely to have a significant macro impact, given the multiple ways different tariffs can be re-instated to circumvent the IEEPA ruling. In terms of refunding US corporates, the USD 120bn is likely to be repaid to companies over a long period as individual court cases are processed. So far, EM countries are the major winners from the new 15% mechanism, as US allies with the preferential 10% ‘minimum’ tariff appear to be the biggest losers from the rate rising. Brazil will see its tariff rate drop by 14%, while China will see its rate drop by 7%. This is likely to be temporary, however, as section 301 tariffs may well be enacted or threatened: particularly to keep the ability of the US to enforce its “trade deals”. Europe and China said they are evaluating the changes in US policies before responding.

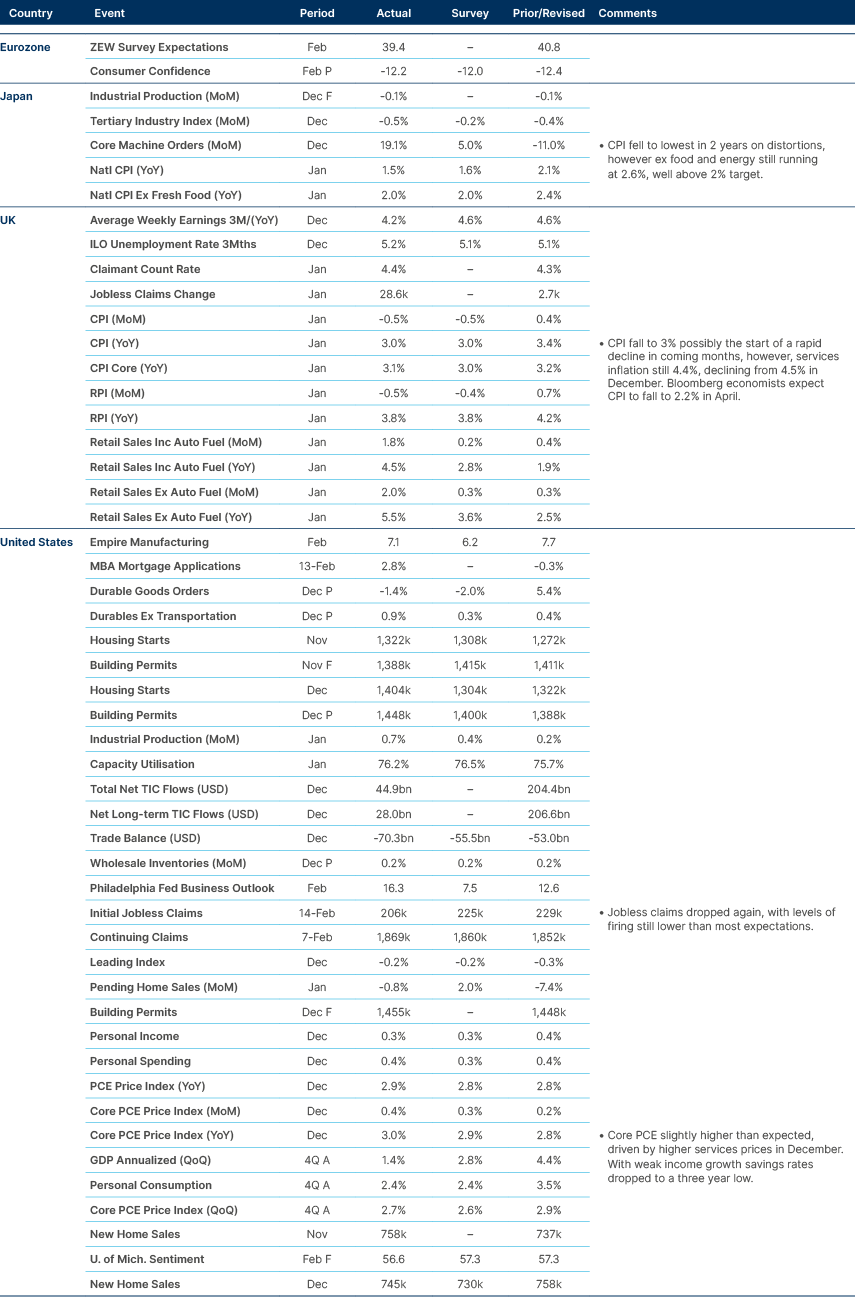

The meeting minutes from January’s Federal Open Markets Committee (FOMC) meeting were cautious, with most board members agreeing that rate cuts should be deferred until clearer evidence of sustained disinflation. The base case remains one to two cuts in H2 2026, data dependent, with a hold likely at the 18 March meeting. The challenge remains balancing inflation risks against labour market softening, but inflation control remains the F ed’s dominant concern. A move in the core personal consumption expenditures (PCE) index toward 2.5% (vs. 2.9% in December 2025) or a broader rise in unemployment would give the FOMC cover to ease. Nevertheless, Dollar funding pressure would ease even if the Fed delivered one or two cuts later in 2026 as priced, reinforcing a structural tailwind for EMFX. There has been no progress so far on Kevin Warsh’s appointment as the new Fed Chair, and even if confirmed his influence in 2026 would likely be limited.

Geopolitics

The US has amassed a record number of troops (as much as a third of US military assets) in the Middle East as pressure on Iran ramps up. The USS Abraham Lincoln carrier group is positioned off the coast of Oman as the USS Gerald Ford moves into the region. US bombers, fighter jets and drones have been taking up positions at the Muwaffaq Salti Air Base, while support and special forces planes have taken up positions at Diego Garcia in the Indian Ocean. Additionally, throughout last Thursday, more US military aircraft flew from Europe to the Middle East.

A historical analysis shows military actions have taken place 75%-80% of the time following mobilisations as large as this one. The activity came off the back of talks in Geneva between the US and Iran, where diplomatic efforts were made to find a resolution over Tehran’s nuclear programme. US Press Secretary Karoline Leavitt mentioned there was some progress, but both parties were very far apart on some issues.

The situation remains fluid. Nevertheless, it remains unlikely a regime change in Iran would take place, in our view.. Trump’s harsh criticism of failed US interventions in Afghanistan and Iraq weigh against it. As a result, a targeted attack like the one in 2025, with aims of damaging nuclear and military infrastructure, is more likely in our opinion. We believe, a short military intervention is unlikely to lead to Iran blocking the Strait of Hormuz, where one-third of the entire seaborne oil market flows through.

Commodities

Brent prices rose above USD 70/bbl on fears of potential supply disruptions, especially following Iran's brief closure of part of the Strait of Hormuz on 17 February. Treasury yields and break-evens rose due to inflation concerns, albeit the sell-off was also supported by hawkish January FOMC meeting minutes and weak demand at a 20-year US Treasury auction.

Emerging Markets

Asia

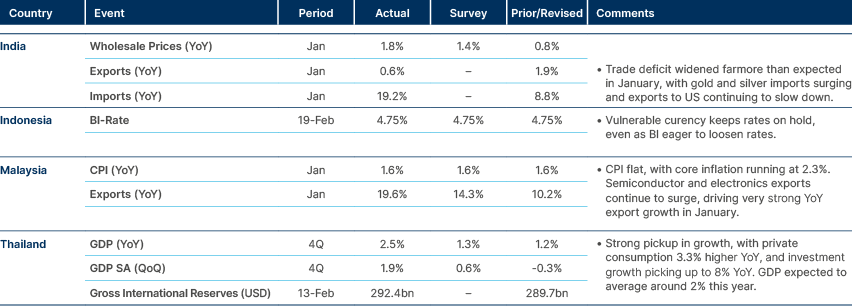

Indonesian central bank remains on hold.

Philippines: The central bank cut its target reverse repurchase rate by 25 basis points (bps) to 4.25% to address weak domestic demand, while keeping 2026-2027 inflation forecasts manageable. Further easing or a hold is possible for the next central bank meeting on 23 April.

South Korea: President Lee Jae-myung is tightening mortgage refinancing for multi-homeowners to curb unearned income and stabilise the property market. In other news, former president Yoon Suk Yeol was sentenced to life imprisonment for the 2024 insurrection, but avoided the death penalty. His supporters remain a source of tension, but the only path to his release would be a presidential pardon, which the ruling Democratic Party is moving to block legally.

Latin America

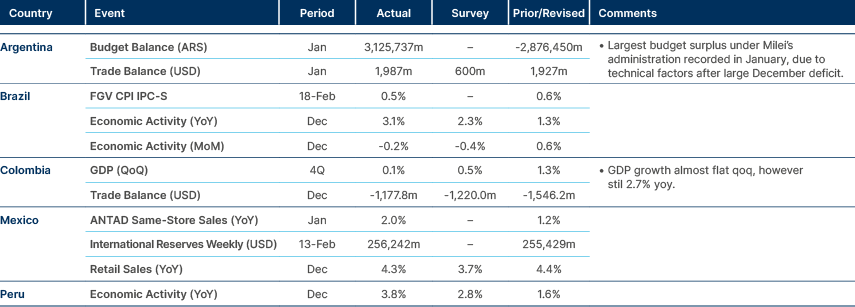

Argentina posts bumper budget surplus in January, Colombia GDP flatlining qoq.

Colombia: Polymarket data shows left-wing candidate Iván Cepeda leading first-round presidential projections by far. However, he remains neck-and-neck with Abelardo de la Espriella in the second round. The 8 March legislative elections are expected be the decisive test for party strength and coalition-building ahead of the final vote.

Dominican Republic: Moody’s affirmed the sovereign ‘Ba2’ rating with a stable outlook due to positive economic growth, improving institutional strength and robust investment flows. However, weak debt affordability and high foreign currency borrowing remain key credit weaknesses.

Mexico: Mexican security forces killed the leader of the Jalisco New Generation drug cartel, leading to severe retaliatory violence across at least 13 states. This includes rioting and looting, as well as roadblocks across the country. Past captures of cartel leaders have set off wars between the government and cartels, as well as between opposing factions jockeying for power in the beheaded criminal group. Schools have been shut in several Mexican states, and local and foreign governments alike warned their citizens to stay indoors. President Claudia Sheinbaum urged calm, and authorities announced late on Sunday that they had cleared most of the more than 250 cartel roadblocks across 20 states. The White House confirmed that the US had provided intelligence support to the operation to capture the cartel leader and applauded Mexico’s army for taking down a man who was among the most wanted criminals in both countries.

Banxico’s February minutes reveal a dovish majority leaning towards a 25bps rate cut in March, viewing recent tax-driven inflation as temporary and prioritising economic and currency strength over the 3% inflation target. President Sheinbaum is considering fracking to boost domestic gas production and reduce reliance on US imports. Reports of an internal fracture in the ruling National Regeneration Movement party (MORENA) suggest a power struggle between Sheinbaum and her predecessor López Obrador ahead of the 2027 mid-term election.

Panama: Fitch Ratings reported that the country’s debt levels remain unstable due to a lack of structural consolidation and limited scope for further investment cuts. The absence of a formal tax reform and the lack of legislative majority for the ruling party to approve revenue boosting measures have created uncertainty around fiscal targets being met.

Peru: Despite executive volatility following the removal of President José Jerí, macro stability remains anchored by the interim five-month mandate of President José Balcázar, who is prioritising governability and fiscal restraint before the April general elections. Balcázar was elected by Congress through an unusual coalition consisting of a left-right pact, defeating frontrunner María del Carmen Alva. He has pledged to ensure “unquestionable” elections on 12 April, refocus the fight against organised crime, and maintain macroeconomic and policy continuity. This is Peru’s eighth presidency in nine years.

Central and Eastern Europe

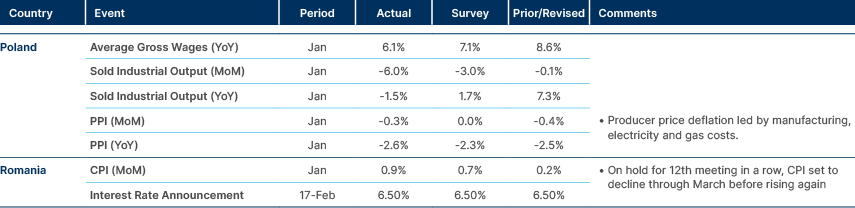

Romanian central bank remains on hold with inflation elevated.

Czech Republic: From 2027, the government will freeze the retirement age at 65 and restore a more generous indexation formula, resulting in an annual increase of CZK 28bn. The biggest fiscal burden will come from freezing the retirement age, but this will not likely be apparent until the mid-2030s.

Hungary: The opposition Tisza Party’s election manifesto has pledged to cut the budget deficit to below 3% by 2030 through eliminating corruption, stopping large scale ‘prestige’ investments and overpriced public procurement. The policy would be supported by the introduction of a 1% wealth tax, while low earners would receive tax relief and benefit from regulated energy prices.

Poland: Poland is expected to save PLN 36bn-60bn by replacing domestic debt with EU SAFE loans to fund defence industry investment. Meanwhile, Fitch Ratings said Poland could keep its ‘A-’ rating until 2027 or longer if the deficit does not worsen above 7% of GDP. In other news, the odds of a policy rate cut in March increased after wage growth slowed for the 28th consecutive month to 6.1%, missing expectations.

Romania: Romania’s public debt rose 1.6% month-on-month in November, reflecting a combination of increased borrowing from local banks and from the population through government securities, alongside drawing on the government’s cash buffer to finance fiscal outlays. The rise in debt comes against a backdrop of persistently large deficits and elevated financing needs as Romania’s public finances have shown sustained expansion in recent years, pushing gross debt toward and above traditional EU comfort levels. Fitch Ratings reaffirmed Romania’s ‘BBB’ sovereign credit rating with a negative outlook, noting that a continuation of rising debt or a deterioration in fiscal and external balances would elevate the risk of a downgrade.

In related policy news, Romania’s Constitutional Court upheld the government’s magistrates’ pension reform, which gradually raises the retirement age for judges and prosecutors to 65, introduces caps on benefit payments, and clears the way for the release of EUR 231m in funds that had been withheld from the third instalment of Romania’s financing under the European Union’s Recovery and Resilience Facility (RRF). The decision removes a legal hurdle to disbursement and supports Romania’s broader adjustment efforts.

Türkiye: The government budget deficit widened by 54.1% yoy in January, due to rising interest outlay despite a ten-fold improvement in the primary surplus.

Türkiye plans to mobilise USD 10bn in investment by 2030 to expand data centre capacity and strengthen its artificial intelligence ecosystem, as part of a broader push to upgrade digital infrastructure and support higher value-added growth. The strategy includes the development of a domestic large language model in Turkish, aimed at accelerating AI adoption across industry, public services and manufacturing, while reducing reliance on foreign platforms. The initiative also envisages the creation of a dedicated research and development framework to support AI innovation, talent development and private-sector integration.

Ukraine: Ahead of a new Ukraine-US-Russia round of talks in Geneva, President Trump urged Kyiv to come to the negotiating table fast. At the Munich Security Conference over the weekend, Ukrainian President Volodymyr Zelenskyy complained about US pressure on Ukraine rather than Russia to accept concessions, whilst the request for fast-tracked EU entry for Ukraine was rejected.

During the talks, Zelenskyy proposed a reciprocal troop withdrawal from the Donetsk region and rejected Russian sovereignty claims. Zelenskyy warned that Russia could be abusing diplomacy to buy more time on the battlefield after a third round of Russia-US talks began.

Middle East and Africa

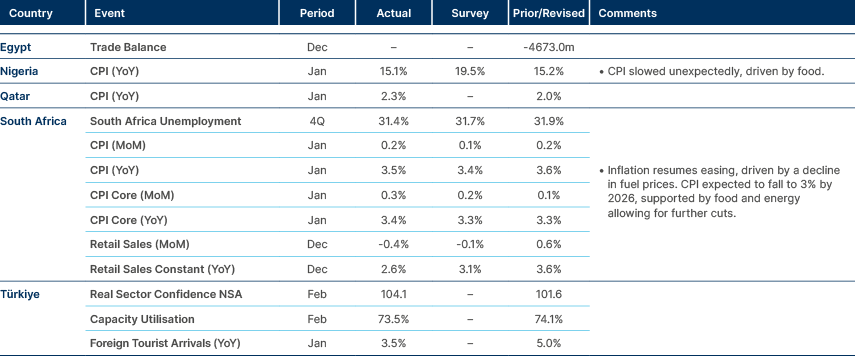

South Africa’s CPI inflation continues its decline.

Africa: China will implement zero-tariff treatment on imports from 53 African countries from 1 May.1 Trade between China and Africa continues to grow but remains structurally imbalanced as Africa's trade deficit with China widened to USD 59.6bn Jan-Aug 2025.

Egypt: The Finance Ministry wants to raise tax revenues to 15-16% of GDP by expanding the tax base rather than hiking tax rates. Proposed changes include a 0.125% stamp tax on EGX transactions and unified tax treatment for listed/unlisted shares.

Ivory Coast: Italian energy company Eni announced a large gas and condensate discovery offshore. It was named Calao South, and the volumes are estimated at up to 5trn cubic feet of gas and 450m barrels of condensate.

Nigeria: The next presidential and parliamentary elections have been scheduled for 20 February 2027, on a staggered timetable. The presidential vote will test the reform agenda of President Bola Tinubu, who is widely seen as a near-certainty for re-election.

In other news, the Petroleum and Natural Gas Staff Association (PENGASSAN) warned that the recent executive order directing revenues to the country’s Federation Account and ending the Nigerian National Petroleum Company (NNPC)’s 30% management fee on profit oil and gas, could threaten 4,000 jobs due to the loss of funds.

Pakistan: The opposition alliance, Tehreek Tahafuz-i-Ayeen Pakistan (TTAP), said it will continue its sit-in outside of the Supreme Court until the government accepts all its demands, including transferring jailed former prime minister Imran Khan to a private hospital amid concerns over his vision loss.

South Africa: The International Monetary Fund (IMF) projects South African public debt will rise to 84% of GDP by 2031 and urged the country to reach a 3% primary surplus to ensure long-term stability. Recommendations for fiscal consolidation include spending reforms, procurement savings and stronger tax administration.

As widely anticipated, the Reserve Bank (SARB) proposed replacing the prime rate with the repo rate (SARB policy rate) to improve transparency and directly link loan pricing to lending rates. The move could increase competition and potentially lower rates in some cases over time.

Zambia: Finance Minister Situmbeko Musokotwane is pushing for Zambia’s inclusion in global bond indices amid the Kwacha rally and significant oversubscription in 2026 auctions. This arises from policy shifts and macro progress, including inflation decline and rate cuts. The case for eventual index inclusion is positive in our view, though liquidity depth and policy consistency remain critical in attracting durable passive inflows.

Developed Markets

US core PCE rose in December, UK CPI dropped significantly in January.

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.

1. Eswatini is excluded due to its recognition of Taiwan.