- Hostilities between US and Iran intensified, oil rose back to nearly USD 80.

- Services inflation across developed markets show no signs of meaningful pickup.

- SK Hynix launched its American Depositary Receipts on Nasdaq, to huge demand.

- Memory stocks in Korea continued to fall, in a positioning unwind.

- China’s central bank has increased its gold purchases.

- South Korea’s central bank governor sees considerable room for a stronger Won.

- Colombia’s president-elect de la Espriella accused President Petro of planning a coup.

- Türkiye commits to increasing core defence spending from 1.5% to 3.5% of GDP before 2030.

- Ukraine secured pledges of EUR 140bn in weaponry across 2026 and 2027 at Ankara NATO summit.

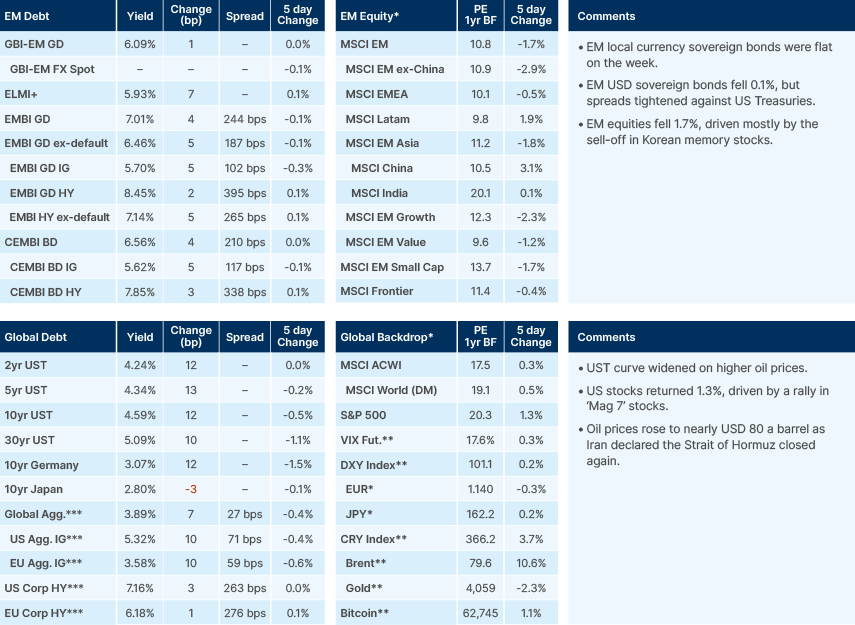

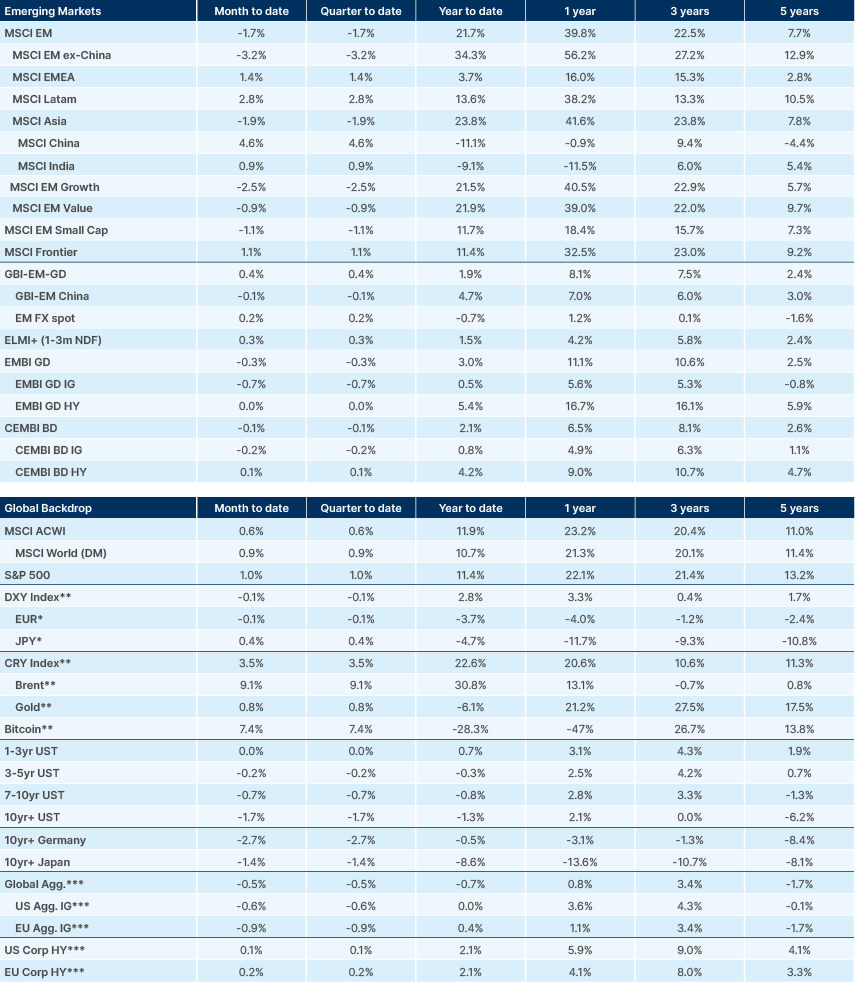

Last week performance and comments

Global Macro

The US military completed a fresh wave of strikes against Iran overnight, targeting air defence systems, coastal radar sites, missile and drone capabilities, and small boats. This was the fourth wave of strikes in a week, following Iranian attacks on three vessels, including a liquified natural gas (LNG) carrier. Iran retaliated by targeting US bases in Kuwait, Bahrain, and Qatar. In a return of the 'Schrödinger's Strait' state of play, Iran says the Strait is closed while the US says it is open.

The data shows visible ship flows have dropped, particularly through the Omani passage, and are now most concentrated along the Iranian coast. Flows had recovered to around 50% of pre-conflict levels after the Memorandum of Understanding (MoU) and prior to re-escalation. In recent days, ships transiting the Omani side have been doing so primarily in 'dark mode', with transponders switched off. The key question is whether dark crossings can sustain meaningful throughput, or whether Iran's formal closure declaration translates into physical interdiction.

According to US officials, negotiations are continuing behind the scenes, with both sides still targeting a permanent resolution by early August. Brent crude rose around 10% last week and traded just below USD 80 this morning. Very light positioning likely amplified the move. Managed money net long positioning in Brent contracts (ICE data) had fallen last week to levels not seen since the end of 2025.

The short positioning in oil may have contributed to a larger spike in prices but also reflects the reality of softer physical demand. This will likely continue to put downwards pressure on prices. Prior to the conflict, balances pointed to a 2–3 million barrels per day (mbpd) surplus for 2026, which flipped into a deep deficit after the closure. Assuming the Strait reopens on the timeline being negotiated, Morgan Stanley now estimates a surplus of 4.8mbpd in 2027, reflecting some permanent demand destruction and increased supply, a more bearish outlook than before the conflict.

However, given the relative stickiness of product prices, crude is probably no longer the key macro variable to watch. The Nymex 3-2-1 crack spread, a benchmark measure of US refiner margins, has been rising since the beginning of June, and has now reached all-time highs. Elevated crack spreads are not inflationary in and of themselves; product prices have declined significantly since their May peak, just not to the same extent as crude.

Nevertheless, the divergence reflects a few truths. First, most strategic reserve releases around the world were crude releases, not product releases, contributing to a mini glut in crude relative to products. Second, China's drop in crude imports, which did so much to suppress crude prices, did little to ease the shortfall in product supply. China imports very little refined crude. Third, Russian refined product exports have roughly halved since a year ago, with most of the decline coming in the last two months. Ukraine has been successfully attacking Russian refineries in recent weeks, prompting export bans and a decline in product shipments. Russia supplied around 11% of global diesel exports in 2025 (800kbpd), so exports halving is obviously significant, particularly into a market with low inventories following the Hormuz closure, and summer holiday season beginning.

With focus shifting to goods and non-core (energy) inflation this year, it is worth remembering that services make up around 60% of the US consumer price index (CPI) inflation basket and therefore tend to matter more for inflation and rates than goods, food or energy. In the EU, UK and Japan, services inflation is lower year-to-date (YTD). This makes sense. The hit to consumers from higher energy prices should reduce demand for services at the margin, and although unemployment is low, workers across developed markets (DM) currently lack the pricing power to demand higher wages, so energy inflation is unlikely to be passed through to services.

Services inflation snapshot:

- US: rose 0.4% from post-pandemic lows to 3.4% (20yr avg 3.0%)

- EU: stuck at 3.2% (20yr avg 2.0%)

- UK: oscillating at 3.7% (20yr avg 3.5%)

- Japan: down to 1.0% (20yr avg 0.2%)

The US is the exception, with services inflation rising from around 3.0% in February to 3.4% in May. Most of the pickup, however, has been driven by housing, which makes up 58% of the services segment of the basket. This mostly reflects measurement noise, including the shutdown-related distortions and base effects, rather than any underlying inflationary dynamic. New lease rents and construction activity remains soft. Meanwhile, declining real incomes combined with the fading boost from the ‘One Big Beautiful Bill ‘tax measures in H2 are likely to weigh further on services demand, and therefore prices, in our view.

SK Hynix's American depositary receipts (ADRs) debuted on Friday priced at USD 149, raising around USD 26.5bn in the second-largest listing on record. The shares rose to USD 168 on the first day of trading, implying a valuation of USD 1.2trn, a 20% premium to the Seoul listing.

That premium widened to 37% after today's 15% decline in the local ticker, which values the Seoul-listed shares at USD 875bn (5.6x P/E). The premium is likely to persist as the ADRs are not fungible and Korean capital controls and regulations prevent arbitrage workarounds. If the US market keeps on pricing higher valuations for memory chips companies, SK Hynix would be able to access capital cheaper via new equity or convertible issuance. Korea is now having its largest drawdown since the rally began. At the time of writing, the Kospi is down 28% from its peak (including a 22% two-day fall in early March) and is trading around its 100-day moving average, with another 18.5% of downside to the 200-day. Today's sell-off was compounded by broader Asian weakness after the latest US strikes on Iran.

In our view, the sell-off has been driven by positioning and technicals rather than fundamentals. The Korean retail frenzy, compounded by leveraged exchange-traded funds (ETFs), was always going to bring elevated volatility. Negative artificial intelligence (AI) narratives may have triggered the latest bout of it, but the fundamentals and the trend higher in Korean stocks are likely to remain intact. Even after the drawdown, the Kospi is up 70% YTD, SK Hynix is down nearly 40% from its peak but up around 180% YTD, and Samsung is down nearly 30% but up 114%. Samsung's earnings call last week, followed by a more bullish TSMC report last night, showed no signs of waning chip demand.

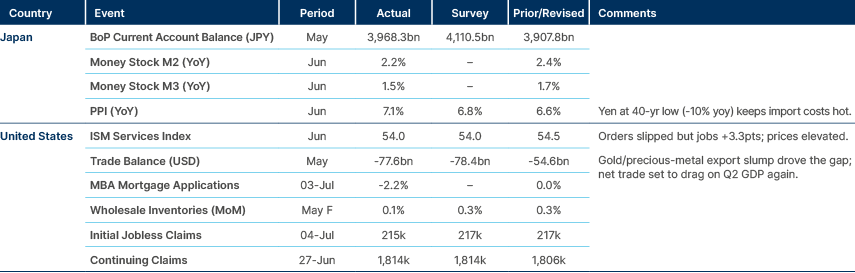

Japanese Finance Minister Satsuki Katayama said on Friday that the government wants GPIF, the world's largest pension fund with around JPY 293trn (USD 1.8trn) in assets under management (AUM), to shift allocation back towards domestic assets. The remarks come against persistent yen weakness near JPY 162 per dollar and a recent Japanese Government Bond (JGB) sell-off. Even a modest reallocation implies large repatriation flows, as roughly half of GPIF assets sit overseas.

Meaningful repatriation could in principle occur within the existing framework, without a formal policy asset mix review, as GPIF has deviation bands of 6% around foreign equities and 5% around foreign bonds relative to its 25% targets, worth some JPY 18trn and JPY 15trn respectively. In 2014, when GPIF moved 17% of its AUM into foreign assets (around JPY 22trn at the time), USDJPY rose from 109 to just below 122 in six weeks, although the BoJ's surprise easing announced the same day makes it hard to isolate the GPIF effect. A comparable shift in the opposite direction would be a material JPY positive and JGB supportive event, with implications for yen-financed carry positions across emerging markets (EM).

The US Federal Reserve (Fed) announced the leadership and objectives of its new task forces, which will review communications strategy, balance sheet policy, data quality, the productivity and labour market impact of AI, and the inflation framework. Appointments are generally of a very high calibre and are likely to improve the nuance around Federal Reserve policymaking, in our view. They include former Bank of England governor Mervyn King, venture investor Marc Andreessen, former New York Fed official Peter Fisher, former Brazilian central bank president Arminio Fraga, former Reserve Bank of India governor Raghuram Rajan, former Fed governor Jeremy Stein, and Nobel laureate Thomas Sargent.

Emerging Markets

Asia

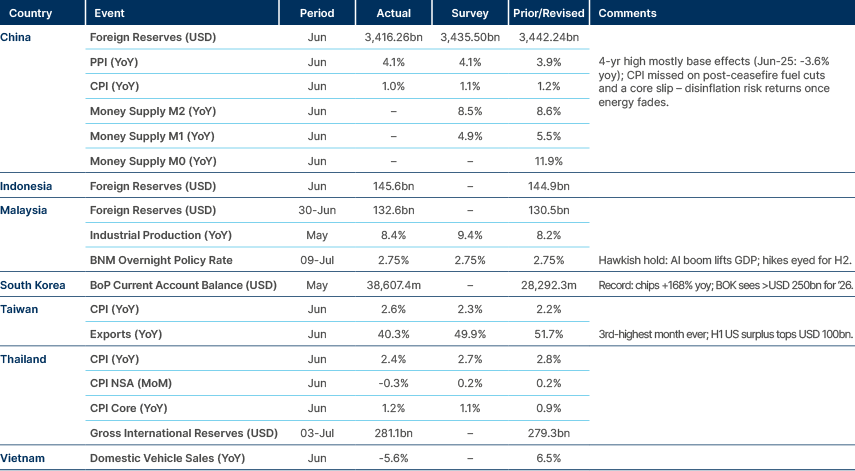

China: China's central bank bought 480k troy ounces of gold in June, the largest monthly purchase since October 2023, extending its buying streak to 20 consecutive months and bringing total holdings to 75.44 million ounces (2,346 tonnes). China is closing in on becoming the world's third largest official holder behind the US (8,133 tonnes) and Germany (3,350 tonnes), needing only to overtake France (2,437 tonnes) and Italy (2,452 tonnes).

Pakistan: The government hopes to host the next round of US-Iran negotiations on 11 July, with Switzerland the alternative venue. The agenda reportedly covers Iran's nuclear programme, the lifting of US sanctions and the unfreezing of Iranian assets abroad, plus the Strait of Hormuz and Lebanon. Last week's technical talks in Doha already paved the way for a partial release of frozen Iranian assets.

Philippines: Central bank (BSP) Governor Eli Remolona hinted at one more 25 basis points (bps) hike, arguing the economy can absorb it as government spending lifts H2 growth back above 3% yoy, a recovery from a scandal-constrained first half but still well below trend. The key rate stands at 4.75% following 50bps of cumulative tightening. June CPI inflation eased to 6.4% yoy from 6.8%, but remains well above the 2–4% target band.

South Korea: Bank of Korea Governor Hyun-Song Shin sees considerable room for the Won to strengthen, calling the recent slide out of line with fundamentals given Korea's very large current account surplus. He blamed the move on US monetary policy expectations and foreign portfolio rebalancing, and expects foreign equity selling to ease in H2. On a Korea-US swap line, Shin said talks continue but stressed Korea faces no dollar liquidity stress.

Separately, the ruling Democratic Party wants a measure penalising deliberate share-price suppression in the upcoming tax reform, raising inheritance and gift taxes on listed companies with P/B ratios below 0.8 by valuing them as unlisted firms. Tax officials warn a uniform threshold is problematic, as low P/B can reflect sector structure rather than deliberate undervaluation.

Latin America

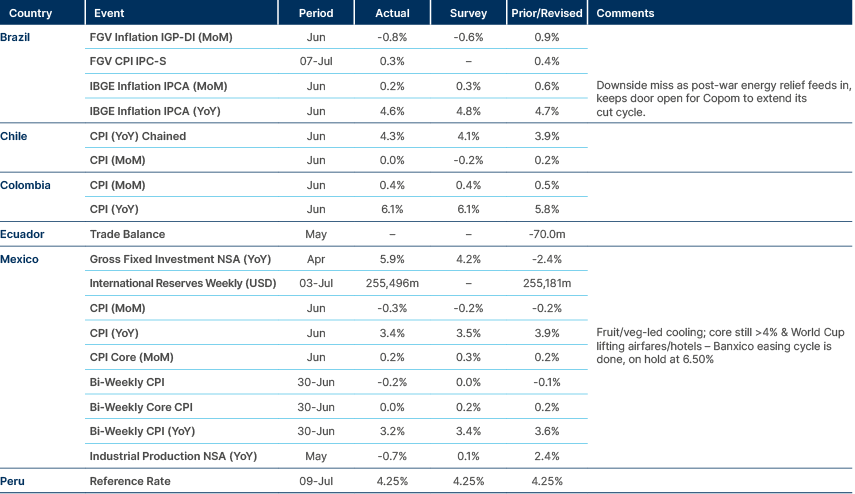

Chile: The International Monetary Fund (IMF) cut its 2026 GDP growth forecast to 1.8% from 2.2% following the Article IV review, while nudging 2027 up to 2.6%. It projects the government will miss its structural deficit targets in both years, at 3.1% of GDP in 2026 and 2.4% in 2027 versus targets of 2.6% and 1.8%. The IMF called the economy resilient but sees risks tilted to the downside, largely tied to higher oil prices, and said keeping debt below 45% of GDP will require additional fiscal effort. It also urged the central bank (BCCh) to stand ready to tighten if oil-driven second-round inflation effects emerge.

Colombia: President-elect Abelardo de la Espriella urged the armed forces to disobey any unconstitutional order from President Gustavo Petro, who since Monday has branded him illegitimate and claimed runner-up Ivan Cepeda actually won the 21 June runoff. The Historic Pact will challenge the result in court, while Petro continues invoking civil disobedience. Markets shrugged, with USDCOP firming intraday to close at 3,323. The near-term market risk is lower than the longer-term political risk, since the fraud narrative arms the left's 2030 comeback bid, and echoes of the 2021 protests suggest social unrest may be closer than markets are pricing.

Central and Eastern Europe

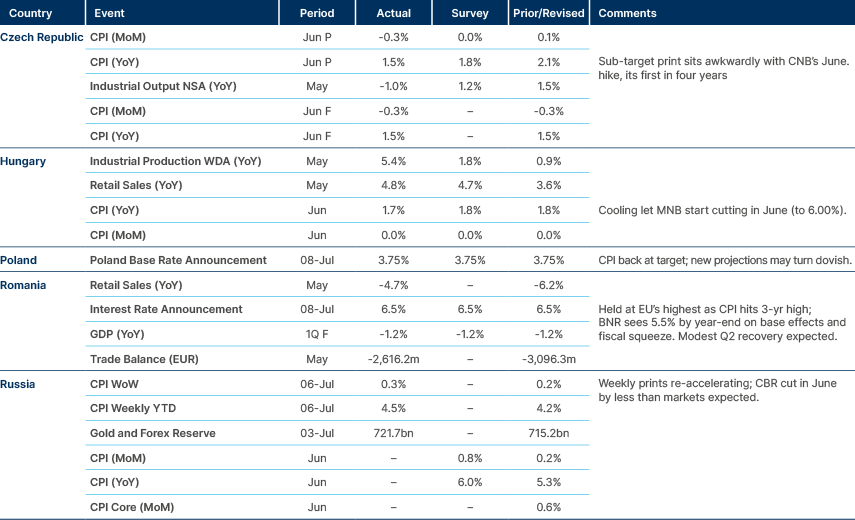

Czech Republic: Defence spending is estimated at 2.01% of GDP in 2026 according to the latest NATO report, sparing Prime Minister Andrej Babis from explaining a sub-2% ratio though still leaving the country near the bottom of the alliance. Across the alliance, five members already exceed the new 3.5% guideline (Estonia, Greece, Latvia, Lithuania, Poland), with Denmark close behind at 3.49%.

Hungary: June Monetary Policy Committee (MPC) minutes showed the base rate was cut 25bps to 6.0% with ten votes in favour, external member Zoltán Kovács alone backing 50bps. The cut rested on an improved inflation outlook, a stronger forint and lower energy and food prices. The Council stressed keeping the real rate positive and high in international comparison.

Prime Minister Peter Magyar submitted his 12-point constitutional amendment to parliament. Key provisions include the immediate termination of President Tamás Sulyok's mandate, a 12-year term limit for MPs, a 70-year age cap on Constitutional Court judges and stripping the Fiscal Council of its budget veto. Critics argue several clauses strain checks and balances. Sulyok has invited the Venice Commission to review and can refuse to sign, in which case Magyar has threatened impeachment.

Poland: Finance Minister Andrzej Domański says EU SAFE loans will save the Treasury at least PLN 36bn versus market financing, with the National Development Bank (BGK) saving a further PLN 67bn over the loans' lifetime, reflecting the EU's superior credit and liquidity. Poland has already signed PLN 120bn (EUR ~28bn) of deals with domestic companies, roughly two-thirds of its EUR 43.7bn allocation, and received some EUR 6.6bn at signing.

Romania: Interim Finance Minister Alexandru Nazare said 49% of the 2026 financing plan was covered by mid-year, with 58% of the domestic programme and 35% of the external target done, and without resorting to pre-financing. Demand recovered strongly from May, with June bids around 70% above amounts offered. Budget execution helped, as the five-month deficit narrowed to 1.75% of GDP from 3.35% a year earlier. Rating agency meetings begin next week, with preserving the rating deemed essential for stable financing conditions.

Ukraine: President Volodymyr Zelenskyy said US PAC-3 Patriot missiles will arrive within days, apparently agreed at the Ankara summit, easing an acute interceptor shortage that has aided recent Russian strikes. Trump also promised Ukraine a Patriot production licence, a meaningful post-war security guarantee ,but not a near-term fix given production lead times. The summit declaration pledged EUR 70bn in military equipment and assistance for 2026 and at least the same for 2027. The US is meanwhile testing Ukrainian air and marine drones ahead of a potential drone deal, mirroring agreements Ukraine has signed with around 10 European partners.

Central Asia, Middle East, and Africa

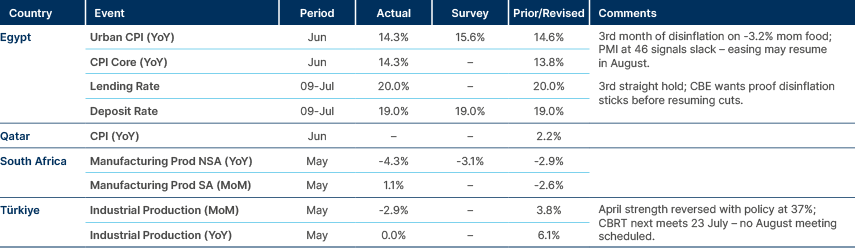

Egypt: The June non-oil purchasing managers’ index (PMI) fell to 46.0 from 47.1, the sharpest deterioration in three and a half years, on weak external and domestic demand, elevated input costs and supply disruption. Output and new orders contracted sharply and employment kept falling, prompting S&P Global to trim its Q2 GDP forecast to 3.8% yoy. Business confidence nonetheless kept improving on hopes of better conditions and FX recovery.

Nigeria: S&P Dow Jones Indices placed Nigeria on its 2027 watchlist for an upgrade from Standalone to Frontier Market status, citing regulatory reforms that improved transparency and enforcement. The signal contrasts with FTSE Russell's June decision to pause Nigeria's planned September reclassification over T+1 settlement concerns, with an update due by the end of August.

Saudi Arabia: Aramco cut its Arab Light price for Asia for a third straight month, lowering the August official selling price (OSP) by USD 11.00/bbl to a USD 1.50 discount to Oman/Dubai, far deeper than expected and the lowest level since 2020. The July OSP had still stood at a USD 9.50 premium. The cut reflects weak Chinese refinery demand, cheaper US and West African barrels, and the resumption of tanker transit through Hormuz over the past six weeks.

Türkiye: President Recep Erdoğan told the NATO summit it will lift core defence spending to 3.5% of GDP before 2030 and already spends 1.5% on resilience, hitting the 5% benchmark five years ahead of the 2035 deadline. Erdoğan announced an additional USD 24bn for the Steel Dome air defence project and claimed a top-ten global ranking in defence production. Politically, he pressed allies to drop intra-alliance defence trade restrictions and warned the EU against excluding non-EU allies from European security initiatives.

United Arab Emirates: ADNOC expanded its long-term energy security partnership with South Korea, guaranteeing delivery of up to 24m barrels of emergency crude and gaining access to Korean refining and storage infrastructure at the Yeosu hub. Co-locating inventories inside Korea moves ADNOC's barrels past major maritime chokepoints and to the doorstep of Northeast Asian demand.

Developed Markets

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. As at latest data available on publication date.

*EMBI GD and EMBI GD HY Yield/Spread ex-default yields and spreads calculated by Ashmore. Defaulted EMBI securities includes: Ethiopia, Ghana, Lebanon, Sri Lanka, and Venezuela. **Price only. Does not include carry. ***Global Indices from Bloomberg. Price to Earnings: 12 months blended-forward.

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.