Regime change in Hungary and positive election results in Peru

- Hungary set to align more closely with EU policies after a landslide victory for the opposition.

- First round of Peru general elections set up a market friendly result in run-off

- The US are moving to embargo Iranian oil exports through the Strait of Hormuz.

- AI capex continues to drive very strong earnings growth from the US to Korea.

- Korea exports running at record levels so far in April.

- S&P downgraded Colombia’s foreign-currency sovereign rating to BB- from BB.

- Fitch revised Turkey’s outlook to Stable from Positive.

- OPEC+ announced a 206,000-bpd production increase for May, repeating the April increment.

Last week performance and comments

Global Macro

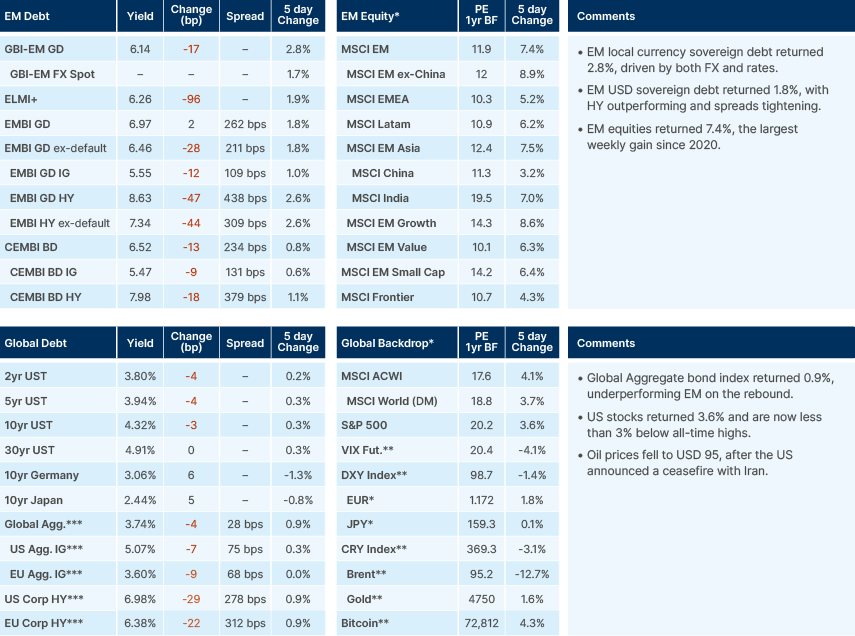

After a two-week ceasefire with Iran was announced on Tuesday, emerging market (EM) stocks notched their best weekly performance since 2020, surging 7.5%. EM bonds also saw a strong recovery, particularly local currency bonds. However, over the weekend, the first formal US-Iran negotiation in Islamabad ended without agreement after 21 hours of talks. The core impasse appears to be Iran’s refusal to surrender its enriched uranium stockpile or commit categorically to never enriching again. Iran is also still seeking to retain some level of control over the Strait of Hormuz, which is unacceptable to the US administration, and indeed other countries, including the rest of NATO. Iran’s Minister of Foreign Affairs, Abbas Araghchi, claimed a memorandum of understanding was close but blamed US negotiators for “shifting [the] goalposts”. Both sides indicated a willingness to continue talks, but the failure suggests each believes it has further leverage to exercise before compromise can be made and a deal can crystallise.

US President Donald Trump responded by declaring a US naval blockade of the Strait of Hormuz, effective today. US Central Command (CENTCOM) later clarified the blockade targets traffic from Iranian ports specifically, meaning vessels transiting to or from non-Iranian ports should, in theory, be unimpeded. Trump also threatened to interdict vessels that had paid tolls to Iran, though how this would be enforced is unclear. The UK and other NATO members are sending minesweepers to support freedom of navigation but are explicitly not participating in the blockade itself.

The near-term risk includes higher energy prices and Iranian retaliation, but this latest roll of the dice from the US may ultimately accelerate negotiations, which is probably part of the reason why the market reaction has been relatively sanguine so far. The critical uncertainties are the timeline, when the US begins escorting commercial ships through, and the China dimension. The US is now potentially blockading Chinese vessels carrying Iranian crude oil, while Trump has threatened 50% tariffs on China if it is caught providing air defence systems to Iran. This dynamic may incentivise Beijing to put more pressure on Tehran to make a deal.

The key watchpoints will be whether the US manages to open the Strait to friendly countries this week. Also important will be the renewal of the US waiver on Russian oil sanctions (which expired on 11 April) and Iran oil general licences (due April 19), continued Iranian retaliation against Gulf Cooperation Council (GCC) states (which did not stop during the ceasefire) and Israel’s next moves in Lebanon and Iran.

Sell-side consensus over the last three months shows a moderate stagflationary tilt for FY2026 numbers, inflation revised up 57 basis points (bps) in developed markets (DM) and 43bps in EM, while growth forecasts have barely moved, down just 15bps in DM and 7bps in EM. The resilience in growth reflects oil-related GDP downgrades (Middle East, Europe) being offset by AI capex upgrades (Taiwan, US). On the inflation side, revisions are more broadly distributed: EU consumer price index (CPI) inflation up 90bps to 2.7%, US up 40bps to 3.2%, with large EM net oil importers seeing significant increases.

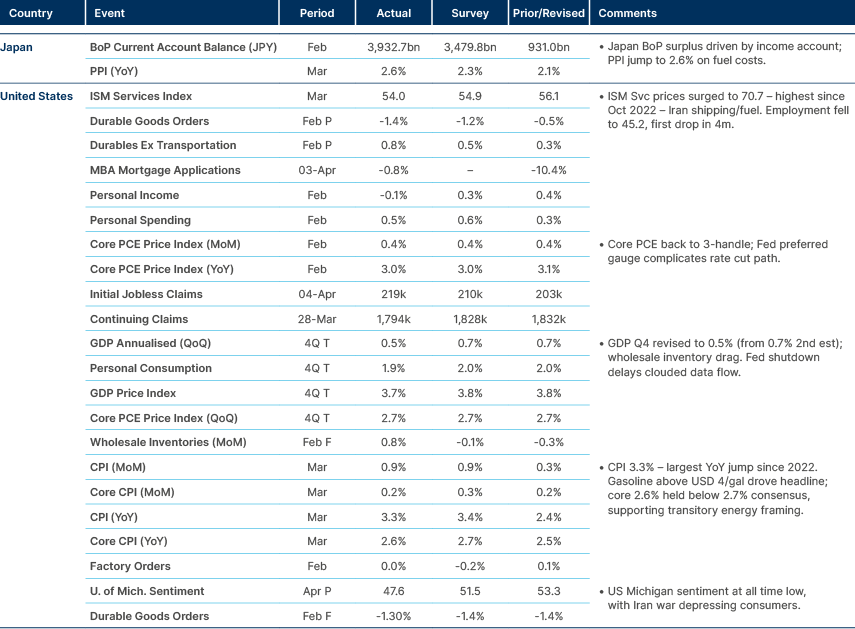

March US CPI inflation confirmed the energy pass-through: +0.9% mom, annual rate jumping to 3.3% from 2.4%, driven almost entirely by gasoline (+21.2% mom, the largest monthly increase since 1967). Critically, core inflation held at just 0.2% mom, taking the annual rate to 2.6% versus consensus of 2.7%. Shelter inflation continued its downtrend at +3.0% yoy. Early signs of supply chain pass-through are visible in PMI delivery times and manufacturing output prices, but levels remain well below 2021-23 peaks. The Federal Reserve is likely to look through the headline spike while core inflation holds. Another notable data point was University of Michigan consumer sentiment falling to 47.6 from 53.3, an all-time low, as higher energy prices begin to bite and Democrats continue to feel very downbeat under the Trump presidency.

US Q1 earnings are tracking at +17% yoy, the strongest in four years, but the composition is strikingly narrow. Tech+ is delivering 23% revenue growth and 30.4% earnings per share (EPS) growth versus just 5.1% for the rest of the S&P 500 so far. Goldman estimates 40% of all S&P 500 earnings growth is currently being driven by AI infrastructure alone. This tech concentration is one reason why global growth has not been revised down further despite the energy shock: the sectors driving marginal growth are more insulated from the oil channel, for now. For EM, the read-through is continued support for the Asian semiconductor supply chain. South Korea reported another record early-month export total in April, up 36.7% yoy to USD 25.2bn in the first 10 days. Semiconductor exports surged 152% yoy to USD 8.6bn.

Anthropic’s release of its Claude Mythos model this week emphasises the accelerating pace of the cycle. The model will not be released to the public for cybersecurity reasons, but its performance metrics relative to previous models and other large language models are public. They show a significant step change in capabilities. Mythos is a strong reminder that AI progress is not slowing down. The result is that software stocks continue to underperform (S&P Software & Services -25.5% YTD) due to fears of disruption, while semiconductors and AI infrastructure stocks have outperformed since the Mythos announcement, with very strong momentum after the initial ceasefire last week. Anthropic's revenue is reportedly now running at USD 30bn ARR, up from USD 1bn at the start of 2025, an unprecedented 30x in 15 months. Roughly 80% of this is enterprise revenue driven by API contracts and cloud provider partnerships, with over 1,000 companies now paying more than USD 1 million a year each. The rest is driven by individual subscriptions, where penetration remains very low. Per Anthropic, only an estimated 3% of US households currently pay for an AI subscription. Nevertheless, Anthropic are scaling enterprise revenue at a rate that has never been seen in the history of corporates. This alone may not put the ‘AI bubble’ narrative to bed, but it at least demonstrates the incredible potential for AI token demand and vast monetisation as models continue to improve.

Commodities

OPEC+ announced a 206,000 barrels per day (bpd) production increase for May, repeating April’s increment. OPEC also issued a pointed statement on safeguarding international maritime routes and energy infrastructure, a notable departure from its usual strictly economic rhetoric.

Geopolitics

Taiwan's opposition leader visited China last week and met President Xi Jinping. According to the Financial Times, Xi Jinping told the opposition leader that unification is an 'inevitability'. Following the meeting, however, China announced a series of policy measures to demonstrate “goodwill” towards Taiwan. The measures include facilitating the sales of Taiwan’s agricultural and fishery products, investment into mainland China and promoting the resumption of certain outbound travel to the island, according to a statement released by the Xinhua News Agency. The steps are aimed at promoting the peaceful development of cross-strait relations, it said.

Emerging Markets

Asia

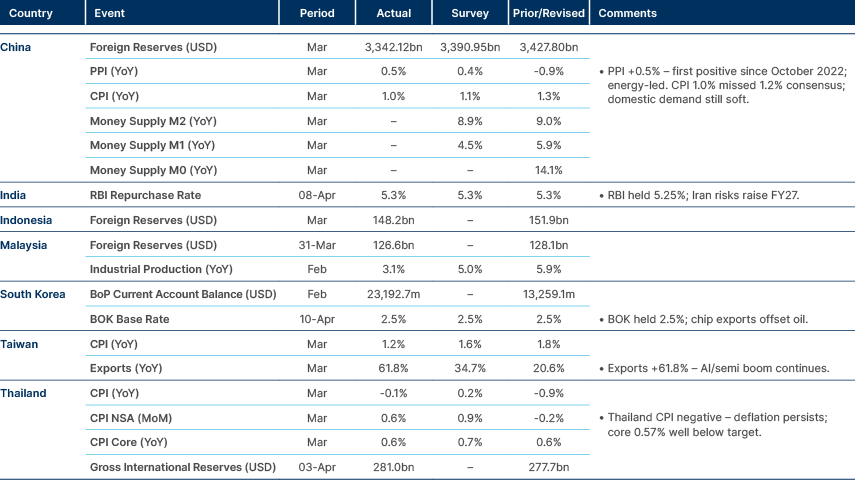

China PPI positive for first time since 2022 on higher energy prices.

Indonesia: Bank Indonesia (BI) Governor Perry Warjiyo told parliament that the scope for further rate cuts is increasingly limited, with the central bank now recalibrating monetary policy towards pro-stability and prioritising rupiah defence through increased Rupia Securities (SRBI) auction volumes. BI has not considered rate cuts since the March Monetary Policy Committee (MPC) meeting and has held the key rate steady for six consecutive months. The shift reflects deteriorating global growth prospects and heightened Middle East tensions, effectively shelving the easing prospects that had looked promising earlier in the year.

Malaysia: Prime Minister Anwar Ibrahim announced the postponement of several large development projects due to rising costs from the West Asia conflict, and instructed ministers to refrain from overseas travel. He ruled out an immediate stimulus package, instead prioritising price controls on essential goods. The government is already paying over MYR 4trn per month on fuel subsidies alone, severely constraining fiscal space for counter-cyclical measures. Anwar indicated that potential stimulus, including tax or tariff relief, would only be considered once essential goods prices had stabilised.

Pakistan: Pakistan and Afghanistan held China-mediated talks in Urumqi from 1–7 April, with both sides agreeing to de-escalate and resolve differences through dialogue. China stepped in as mediator after Middle East tensions diverted the attention of Türkiye and Gulf states that had previously brokered ceasefires between the two countries.

Separately, Prime Minister Shehbaz Sharif invited US and Iran delegations to Islamabad on 10 April for peace talks following President Trump’s announcement of a ceasefire. Trump credited discussions with Sharif and Chief of Army Staff Asim Munir in brokering the truce, and Iran confirmed its participation. Pakistan’s mediation role drew widespread international praise.

Philippines: S&P revised the Philippines’ outlook to stable from positive while affirming ‘BBB+’, citing heightened risks from the Middle East conflict for the country’s external and fiscal metrics. GDP growth is projected at 5.8% in 2026, rising to 6.2% over 2027-2029, with inflation expected at 3.4% in 2026. The central bank (BSP) is seen maintaining a broadly neutral monetary policy stance for the remainder of 2026.

South Korea: Ruling and opposition parties agreed to pass the government’s KRW 26.2trn supplementary budget without changing its overall size. The package includes oil price relief payments of KRW 100,000 to KRW 600,000 per person for the bottom 70% of the income distribution, plus KRW 100bn for public transport fare discounts and KRW 200bn for naphtha supply stabilisation. Authorities are also mobilising KRW 26.8trn in new liquidity support for firms hit by the Middle East crisis, with four policy institutions expanding funding programmes to KRW 24.3trn.

Bank of Korea Governor nominee Shin Hyun-song said the risk of stagflation is currently low, describing the inflation pickup as a temporary supply shock that would not warrant aggressive monetary tightening. He defended FX reserve adequacy at USD 423.6bn and highlighted household debt at 88.6% of GDP as a key domestic vulnerability. The Iran ceasefire immediately freed seven stranded tankers carrying 14m barrels of crude oil, roughly a week’s national consumption, though refiners remain cautious given the time-limited truce and are accelerating Hormuz bypass strategies via Fujairah.

Exports rose 36.7% yoy to USD 25.2bn in the first 10 days of April, the highest early-month total on record. Semiconductor exports surged 152% yoy to USD 8.6bn, accounting for 34% of total shipments, up 15.6pp from a year earlier, reflecting sustained AI-related demand. Growth was uneven elsewhere: petroleum products rose strongly but autos (-6.7%) and auto parts (-7.3%) contracted, highlighting deepening sectoral divergence. Exports to China (+63.8%) and the US (+24%) were robust. The data reinforce South Korea’s rising dependence on the chip cycle, which provides leverage to tech demand but also increasing concentration risk.

Latin America

Chile CPI rises but remains within target range, rates held in Peru.

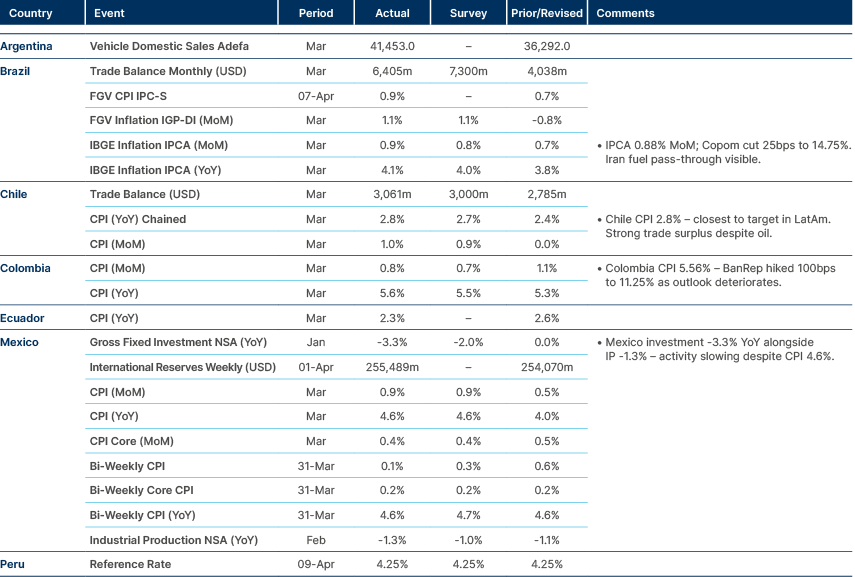

Colombia: S&P downgraded Colombia’s foreign-currency sovereign rating from ‘BB’ to ‘BB-’ with a stable outlook, citing high and persistent fiscal deficits following the three-year suspension of the fiscal rule in June 2025. S&P projects a general government deficit of 5.6% of GDP in 2026 and net debt approaching 66% by 2029. CPI inflation is seen averaging 5.9% in 2026, returning to the 3% target range only around 2029.

President Gustavo Petro responded to BanRep’s rate hike to 11.25% with fertiliser subsidies, export curbs and subsidised credit via state banks. He warned he may declare a new economic emergency. The Constitutional Court is expected to rule on the legality of the December 2025 emergency decree. BanRep warned that the 23% minimum wage hike could add up to 200bps to 2026 inflation through cost pass-through and the lighthouse effect on higher skilled wages.

El Salvador: International tourist arrivals rose 28% yoy in January-March to 1.3m visitors, with March setting a historic record at 453,000. Easter arrivals surged 50% yoy to 208,000. Tourism remains one of the strongest sectors under President Neyib Bukele, driven by improved public security. The government has targeted 4.2m visitors in 2026, up from 4.1m in 2025.

Mexico: The Bank of Mexico (Banxico) appointed Aldo Heffner Rodriguez as its new Chief Economist, filling a role that had been vacant for six months following Alejandrina Salcedo’s resignation in October to join the Bank for International Settlements. Heffner has served as director of the central bank’s economic measurement division since 2018 and takes up the post on 13 April.

Peru: Peru held the first round of its presidential and congressional elections on 12 April, with 35 candidates on the ballot and 27m voters. No candidate came close to the 50% threshold required to avoid a runoff. With partial results processed, the official count from electoral authority ONPE showed early on Monday that former the conservative congresswoman Keiko Fujimori was leading with about 17% of the vote, followed by right‑wing former Lima mayor Rafael Lopez Aliaga on roughly 15% and center‑left candidate Jorge Nieto in third place with around 15%. Just over 50% of votes had been counted. Logistical failures forced the reopening of some polling stations on Monday after around 63,000 voters were unable to cast ballots.

The market-relevant outcome is the concentration of votes among centre-right and right-wing candidates. With Fujimori and Lopez Aliaga both in contention for the runoff, the second round on 7 June is likely to feature at least one market-friendly candidate, and plausibly two. Centre-right candidates appear to be leading across the board in congressional races as well. This is a positive signal for policy continuity and fiscal discipline in a country that has had nine presidents in a decade. Peru returns to a bicameral legislature with this election, adding a 60-seat Senate to the 130-seat Chamber of Deputies.

Central and Eastern Europe

Poland and Romania held rates as expected.

Czech Republic: The registered unemployment rate reached 5.0% in March, slightly below the 5.1% consensus. Jobseekers rose 15.6% yoy, but the pace eased from February, while vacancies per jobseeker (up to six months) stood at 0.47, down 4bps yoy. Newly announced vacancies rose 13.1% yoy after two months of decline, and filled positions surged 76.5% yoy, indicating solid hiring continues albeit unevenly distributed. Job shedding remains concentrated in manufacturing, while services continue to hire at a slower pace.

Hungary: After 16 years in power, Viktor Orban conceded defeat on election night after preliminary results (97% of precincts counted) showed the opposition Tisza party winning a commanding supermajority. Led by Peter Magyar, the Tisza party won 53.7% of the popular vote and 138 seats out of 199 in parliament. The Fidesz party collapsed to 37.8% and just 55 seats, losing over half its previous 135 seats. The smaller MH party took about 7 seats. Turnout was nearly 79%, the highest in Hungary’s post-communist history.

The two-thirds supermajority is constitutionally significant. It gives Tisza the power to amend the constitution and dismantle Fidesz’s institutional control over the judiciary, state-owned enterprises and the media. Magyar announced plans for sweeping reforms under a “Hungarian New Deal” and called for the resignation of several senior officials including the president. Orban’s loyalists are deeply entrenched across Hungary’s institutions, so the transition will not be without friction, but the direction of travel is clearly towards closer alignment with the EU and NATO. Beyond Hungary's domestic outlook, the result has significant implications for EU decision-making. Orbán had used Hungary's veto to block the €90 billion EU loan package for Ukraine, delayed rounds of EU sanctions on Russia, and regularly obstructed common foreign policy positions requiring unanimity. With a pro-EU supermajority in Budapest, the most persistent structural obstacle to EU cohesion on Russia and Ukraine policy is removed. This matters for markets because EU defence and reconstruction spending, which has been repeatedly held up by Hungarian vetoes, can now proceed with greater speed and certainty. For EM investors, a more unified EU foreign policy stance also reduces the tail risk of a fragmented European response to future geopolitical shocks.

The most immediate economic implication for Hungary is the potential release of EUR35bn of EU funds that Brussels had frozen overrule-of-law concerns. The blocked funding is equivalent to roughly 10% of Hungary’s GDP, and its release could add 1-1.5 percentage points to potential GDP growth. Tisza’s programme also includes steps towards euro adoption, and EU Commission President von der Leyen welcomed the result as a move towards Europe. The inflation outlook remains dominated by global energy prices and domestic administered price adjustments, but if the forint appreciates on improved EU relations, the central bank would be expected to adopt an easier monetary policy stance with a shorter pathway to normalisation.

Poland: Prime Minister Donald Tusk confirmed that fuel price measures remain in place despite the Iran ceasefire. VAT on fuel is reduced until end-April and excise duty until 15 April, with the Energy Minister indicating excise could return to normal next week if the calm holds. The monthly cost of the fuel package is PLN 1.6bn. The government is balancing fiscal strain against political sensitivity on fuel prices ahead of autumn 2027 elections.

Romania: The National Bank of Romania (NBR) held the key rate at 6.50% as expected, unchanged since August 2024. The central bank flagged a short-term inflation pickup between March and June, driven by fuel price shocks overlapping with base effects and the electricity cap expiry. The NBR expects sharp disinflation in Q3 once these effects wash out. Fiscal correction is seen reinforcing demand-side disinflation, but material uncertainty remains around the next set of EU medium-term fiscal plan consolidation measures. Another hold is very likely in May, in our view.

Türkiye: Minister of Treasury and Finance Mehmet Şimşek framed the Iran war as the largest shock since World War II and defended Türkiye’s stability, citing USD 162bn in gross reserves with the net position excluding swaps remaining positive. The government targets inflation below 20%, dismissing market expectations near 30% as overstated. Şimşek warned that excessive Lira depreciation would cause serious balance sheet damage given the real sector’s USD 200bn FX short position. New incentive packages are being prepared for the Istanbul Financial Centre, exporting manufacturers and foreign investors.

Fitch revised Türkiye’s credit outlook from positive to stable while affirming ‘BB-’. The revision reflects a marked fall in international reserves since the start of the Iran war, with FX interventions by the central bank (CBRT) estimated to be in excess of USD 50bn. A more protracted conflict would further pressure Türkiye’s external finances and inflation, mainly due to its sizeable energy trade deficit.

Central Asia, Middle East, and Africa

Egypt CPI under pressure.

Africa (broad): The African import-export bank Afreximbank launched a USD 10bn Gulf Crisis Response Programme to provide FX liquidity for fuel, food and fertiliser imports across African and Caribbean economies exposed to Strait of Hormuz disruptions.

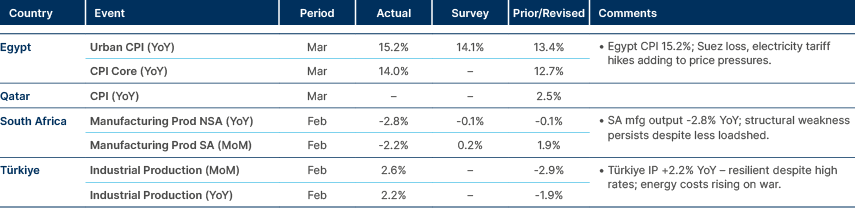

Egypt: A Reuters poll expects CPI inflation to accelerate to 14.7% yoy in March from 13.4% in February, driven by a 14% EGP depreciation and a 16% fuel price hike linked to the Iran war. Electricity prices for higher-use residential and commercial users were raised from April. The Egypti Monetary Policy Committee (MPC) paused its easing cycle last week, citing the war and high February inflation. Some analysts believe the MPC may need to reverse its stance should inflation accelerate further in April and May.

Ghana: Moody’s revised Ghana’s credit outlook from stable to positive, affirming ‘Caa1’. The revision is driven by the increasing likelihood of a durable improvement in domestic financing conditions, contributing to lasting improvements in debt affordability and government liquidity. Domestic financing costs have declined amid monetary easing and an improved fiscal position, while the resumption of domestic bond issuances should gradually reduce rollover risk if sustained. The outlook assessment will test the resilience of these trends against inflationary risks from the Middle East conflict, given Ghana’s susceptibility to terms of trade volatility.

Morocco: The International Monetary Fund (IMF) warned that Morocco’s planned infrastructure push of around 12% of GDP will lift long-run GDP by 3%, but gains depend heavily on execution and fiscal discipline. Near-term effects are dampened by import leakages and private investment crowding-out, while public debt rises during the construction phase before stabilising. Cost overruns would worsen fiscal dynamics without additional output gains.

Nigeria: The World Bank projects GDP growth averaging 4.2% over 2026-2028, slightly below January’s 4.4% estimate, supported by macroeconomic stabilisation and structural reforms. Higher oil prices improve the fiscal position, but the World Bank warns they could add up to 3.1pps to headline inflation. Imported petrol is estimated 12% cheaper than the Dangote Refinery supply. Dangote announced 17 fuel cargoes shipped to African countries and plans to raise refinery capacity from 650,000 to 1.4m bpd by 2028 in partnership with Honeywell International.

Saudi Arabia: The key East-West pipeline that bypasses the Strait of Hormuz was struck by Iran on Wednesday but is now running at full capacity again.

South Africa: Geordan Hill-Lewis, the 39-year-old Mayor of Cape Town, was elected as the new leader of the Democratic Alliance (DA) Party, replacing John Steenhuisen who stepped down after almost seven years. Hill-Lewis vowed to use the upcoming local ballot as a stepping stone to building the DA into the largest party ahead of the 2029 national elections. He has signalled continued DA participation in the coalition government, but wants greater sway over policy and decision-making, and intends to seek another term as Cape Town Mayor rather than take a cabinet post, arguing this will better differentiate the DA from the African National Congress Party.

Zambia: Chinese-owned mining companies now account for more than 50% of Zambia’s total copper production, with investment topping USD 1bn. Zambia has maintained its position as the world’s second-largest copper producer for seven consecutive years. The concentration of production among foreign-owned entities raises structural questions around domestic value addition and revenue retention as the country targets 3m tonnes of copper production by 2031.

Developed Markets

US Consumer sentiment at all time low.

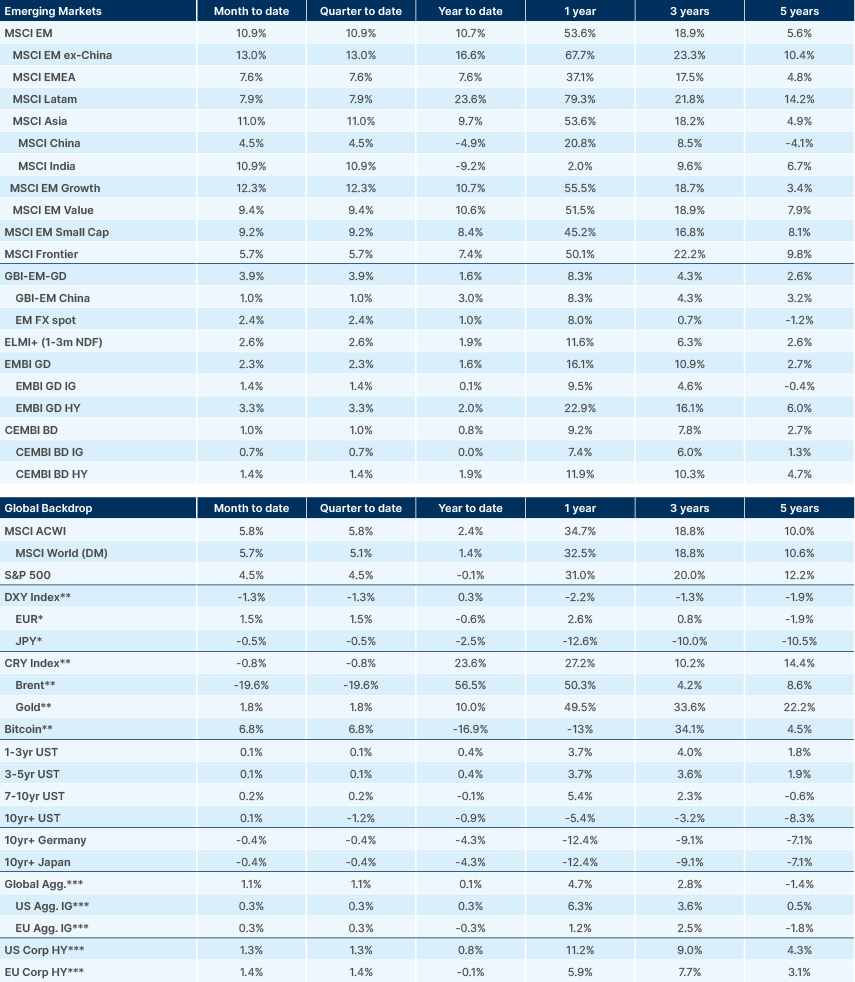

Benchmark Performance

Source and notations for all tables in this document:

Source: Bloomberg, JP Morgan, Barclays, Merrill Lynch, Chicago Board Options Exchange, Thomson Reuters, MSCI. Latest data available on publication date.

* Price only. Does not include carry. ** Global Indices from Bloomberg. Price to Earnings: 12m blended-forward

Index Definitions:

VIX Index = Chicago Board Options Exchange SPX Volatility Index. DXY Index = The Dollar Index. CRY Index = Thomson Reuters/CoreCommodity CRM Commodity Index.

Figures for more than one year are annualised other than in the case of currencies, commodities and the VIX, DXY and CRY which are shown as percentage change.